Raising our June projection to HK$23-24.5 billion (14-22% YoY growth)

This week’s average daily table revenues (ADTR) increased 21% YoY to HK$750 million. We are raising the top end of our full month June projection to HK$23.0-24.5 billion, which would represent YoY growth of 14-22%. The June numbers continue to confirm our expectation of a June rebound from May’s disappointing 7% growth.

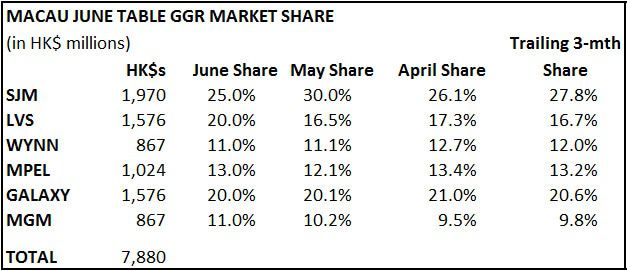

LVS finally made a move toward justifying its big investment in Sands Cotai Central (SCC). It’s only one week of data and 20% share is probably not sustainable – at least not yet – but this was a good week for LVS. We’ve been writing that not only will June be better overall for the market but also for LVS. LVS’s share thus far in June is way higher from the recent 17% share. We expect the next few months to shake out in the 18-19% range for LVS followed by another step up later in the year when the additional amenities open.

MGM is also having a good month while SJM is the big loser so far in June. Wynn’s performance continues to underwhelm. Here are the numbers: