Short term trading opportunities notwithstanding, we’d avoid MCD on the long side for now. The second quarter results and conference call will offer investors more clarity on the business’ prospects for the next year-to-eighteen months.

McDonald’s reported May sales results this morning and, as we suspected, sales disappointed as Global Growth Slowing meant that MCD comps came in below expectations in all regions. Comping the comps in the U.S., Germany slump in Europe, and negative comps in China are important issues going forward.

McDonald’s reported global comparable sales growth of 3.3% in May, which represented deceleration in the two-year average trend from April. McDonald’s continues to take share from its competitors in major markets and we are positive on the name over the longer term TAIL (three years or less). Over the near-term, however, we see a difficult compare in June as posing more headline risk for the stock. Additionally, the FX headwinds that are expected to peak in 2Q and 3Q could cause investors to shy away from McDonald’s in any search for safe plays in the consumer space over the next few months.

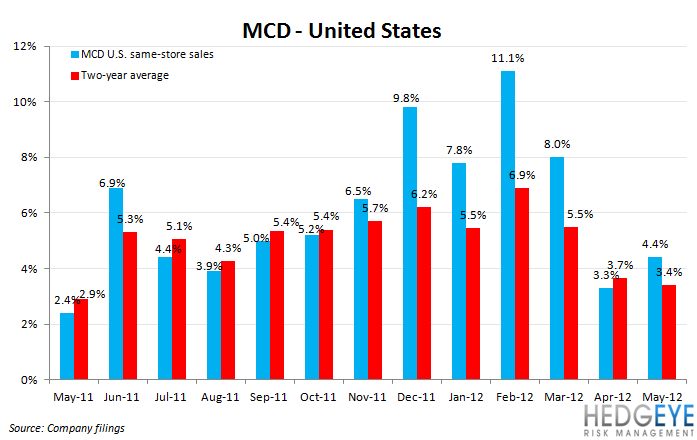

United States

McDonald’s U.S. comparable restaurant sales gained 4.4%, slightly ahead of our estimate of 4% and below consensus of 5.3%, according to Consensus Metrix. With price running at 3%, traffic/mix of 1.4% was short of what the Street was expecting. The question we would ask at this point is whether the Street is overestimating the ability of the company to drive guest counts through the summer. As we wrote on 4/23/12, “The evidence suggests that beverages are increasingly becoming a less important part of the vocabulary from McDonald’s’ management team. With that in mind, foremost in our thoughts is what the company’s strategy will be to maintain top-line momentum over the next few months.”

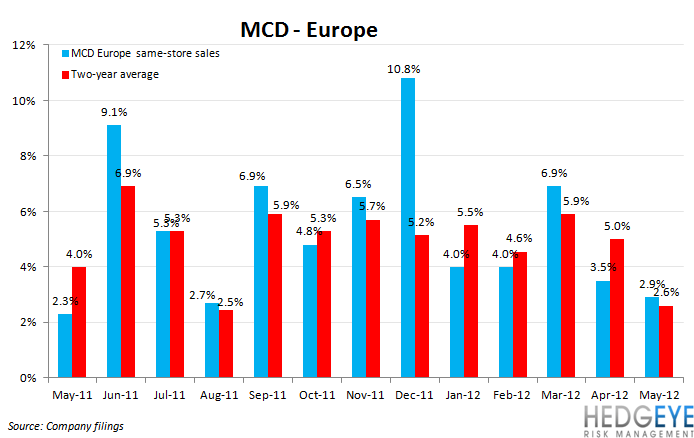

Europe

Management stated that the U.K., Russia, and France drove the 2.9% comp in May, partially offset by Germany. We expect Germany to be a key focus for investors heading into the second quarter earnings release on 7/23. Europe represents 40% of total revenues and 39% of total operating profit for McDonald’s. Overall, the print was a disappointment versus the consensus of 5.1% and the macro environment remains a concern.

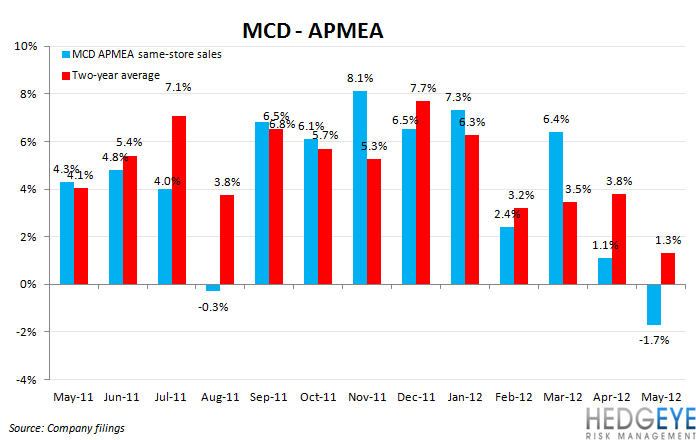

APMEA

APMEA comparable restaurant sales were perhaps the most glaring of the disappointments in the MCD press release; versus consensus expectations of 3.2%, the print came in at -1.7%. Japan (SSS -11% in May!) and, to a lesser extent, China drove the comp lower. Australia posted some positive results that partially offset the slump in China and Japan. While we view the U.S. and Europe as being far more important than APMEA (18% of operating income), a disappointment of this magnitude in an important growth region for the company is not positive news.

It has an Extra Value Menu but it is an Extra Value Stock?

The question now is, “does McDonald’s stock represent a compelling value purchase, even if its menu offerings may not?”

If you believe valuation is a catalyst, then buying the stock here is likely a good idea. The stock is nearing the bottom of its five-year valuation range and has typically been a safe haven for investors in weaker economic times. In early March, however, the first mention of austerity impacting Europe moved us to write the following: “We are not buyers of the stock on this selloff. In short, if austerity is having an impact it will not be a one month phenomenon.”

The uncertainty in McDonald’s results is somewhat new and forecasting FY12 and FY13 EBITDA is only becoming more difficult as uncertainty mounts. The volatility in the economies that McDonald’s operates in is, in some cases, so great that the staple nature of the company’s product is not sheltering sales to the extent that it has historically. Observers, including us, are often tempted to assume that the company’s value offerings will perpetuate strong sales growth. At this point, we lack confidence that the company has a sufficiently impactful pipeline of promotions to comp the strong U.S. performance during summer 2011.

If the Street is overly optimistic on management’s ability to drive traffic over the coming months, the cheap may get cheaper. Short term trading opportunities notwithstanding, we’d avoid MCD on the long side for now. The second quarter results and conference call will offer investors more clarity on the business’ prospects for the next year-to-eighteen months.

Howard Penney

Managing Director

Rory Green

Analyst