-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Long German Bunds (BUNL); Short EUR/USD (FXE)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +2.9% week-over-week vs -3.1% last week. Top performers: Spain +8.0%; Italy +5.5%; Hungary +3.9%; Russia (RTSI) +3.8%; Finland +3.4%; France +3.4%; Turkey +3.1%. Bottom performers: Ukraine -16.2%; Cyprus -11.3%; Greece -6.2%; Romania -3.9%; Denmark -1.3%.

- FX: The EUR/USD is down -0.58% week-over-week vs -0.83% last week. W/W Divergences: HUF/EUR +3.14%, RUB/EUR +3.02%, PLN/EUR +2.62%, CZK/EUR +1.36%; SEK/EUR +1.03%, NOK/EUR +0.51%, GBP/EUR +0.07%.

- Fixed Income: Another crazy week of swings in yields. Greece fell -175bps week-over-week to 28.93% after hit near term highs last Friday. Portugal also saw large declines, falling -80bps to 11.18%, followed by Spain at -31bps to 6.22%. German bund yields bounced +11bps on the week to 1.28% after a low of 1.17% on 6/1. Italy held tight on the week, gaining only +4bps to 5.78%.

Europe’s Runway:

In today’s Early Look my colleague Daryl Jones opened the note with a quote from Seth Klarman’s Q1 2012 letter to investors:

“We are comfortable missing out on potentially major rallies if they are based purely on money flows or government action; the risks of engaging in this sort of speculative activity are simply too high.”

We keep this quote front and center as investment advisors: as close as we follow the developing European political scene and attempt to weight probable scenarios for Europe going forward, we cannot get ahead of the decisions of Eurocrats.

We are, however, highly focused on the political calendar. Our expectation is that European markets may be range bound (and in a wait-and-see mode) ahead of a stiff calendar of events in June, including: Greece elections (on the 19th), G20 Meeting (18-19.), EU Summit (28-29.), and more clarity on Spanish bank recapitalizations.

The main topics of discussion at these meetings should surround: a fiscal union, Eurobonds, a Pan-European insurance deposit facility, and scope of the ESM, all measures that could have great impact on markets. Here we’ll say that while we do not think any of these measures will be signed off on this month, sentiment around these measures will be critical to track as Europeans try to will an end to the crisis.

To this end, this week saw Germany rhetorically increase its pro-fiscal union stance, with Merkel importantly signaling that the Eurozone cannot survive as just a monetary union. She said:

“We need more Europe, we need not only a monetary union, but we also need a so-called fiscal union, in other words more joint budget policy,” Merkel said. “And we need most of all a political union, that means we need to gradually give competencies to Europe and give Europe control.”

While Merkel’s stance is still decidedly anti-Eurobonds, her emphasis on the importance of a fiscal union shows her determination to keep the Union intact, it recognizes the compromised nature of having states simply bound under monetary policy, and it portends a message that Brussels (via stronger countries like Germany) will continue to subsidize the weaker nations to keep the existing Eurozone fabric alive.

However, getting countries to relinquish their fiscal sovereignty to Brussels is a large step, one we think is challenged by the great cultural divide across countries, which may delay formal ratification across member states. Already we’ve seen fierce resistance from the UK. In any case, we believe a fiscal union will first have to be in place before Eurobonds could be issued (if they ever are).

Another big topic this week is whether Spain's troubled banks will be able to recapitalize with funds provided directly from the bailout mechanism, or whether the EFSF/ESM will have to channel the money through FROB, the country's bank resolution fund. The size of the bank recap needs are still widely unknown, with figures spanning from 40B to 100B EUR . We’re going to key off an IMF report released on Monday (6/11), and a separate report due by 21. June from two independent assessors, Oliver Wyman and Roland Berger.

What we do know is that there is no panacea to “fix” Europe’s mess with one fell swoop. The road to end this sovereign and banking crisis is a long one. Note that ECB President Draghi even suggested 10 years (see our note titled “June ECB Presser YouTubed”). We think that Eurocrats are likely to continue to attach band-aid bailout packages in lieu of more comprehensive packages, either because they cannot form a consensus with other member states, because it would spell their own political suicide at home, or because they simply are not savvy enough to craft a path of resolutions to cure the sovereign and banking ails.

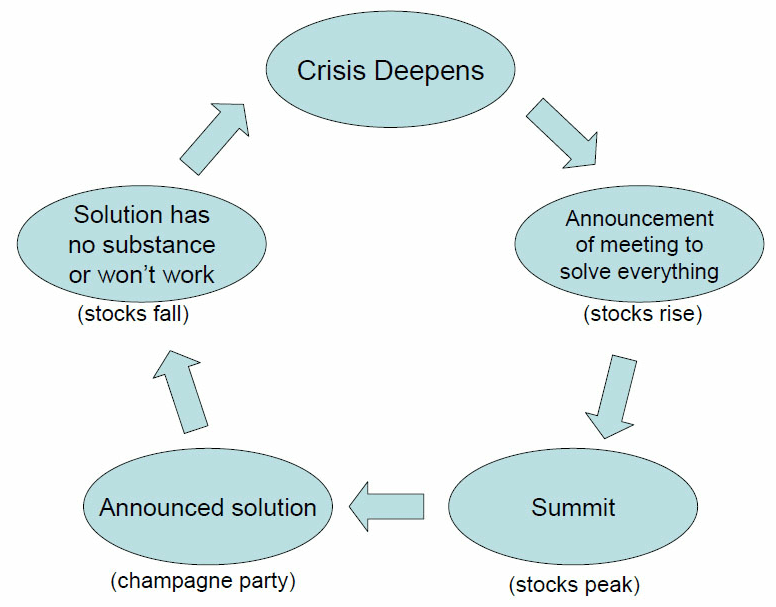

Given the likelihood of Europe to drag its feet, we unfortunately see many months ahead of David Einhorn’s chart playing out:

For yet another week we point you to the Data Dump section below. This week showed weakness in PMIs, contraction in Industrial Production across most countries, weak Eurozone Retail Sales, and some really poor numbers in Germany across the board. No European country is immune to our theme of growth slowing!

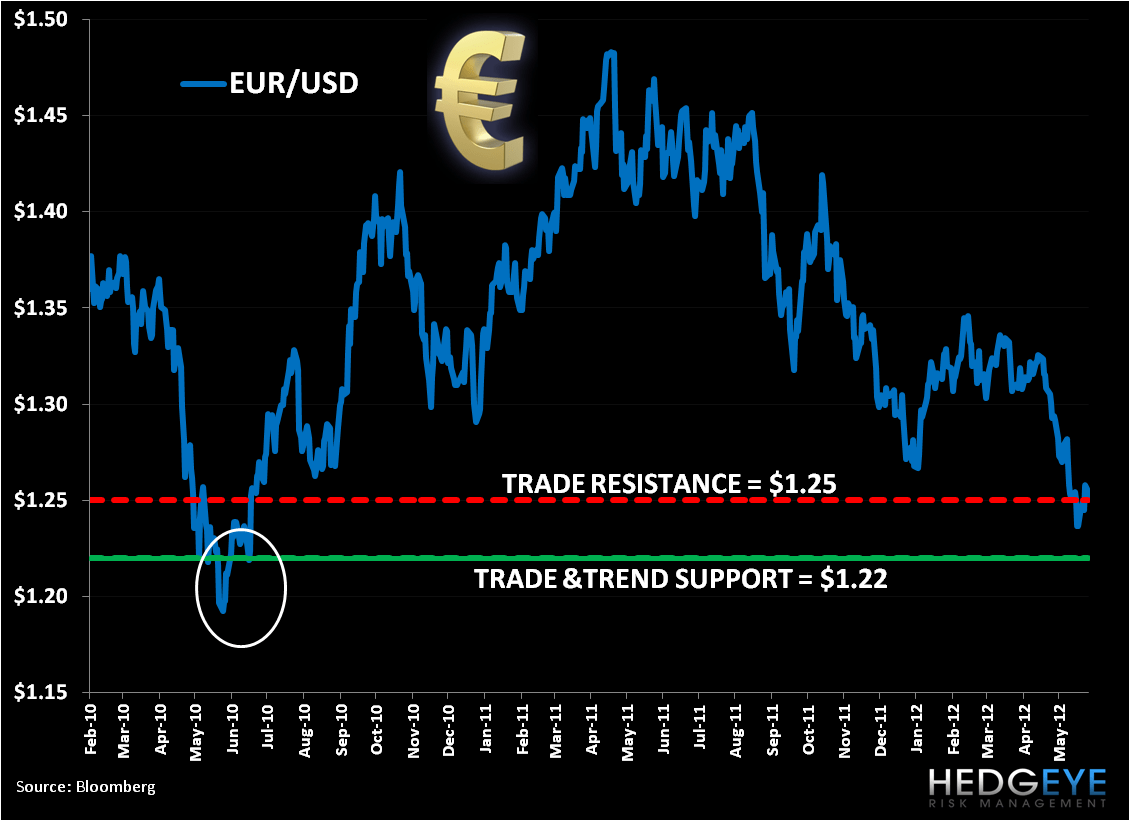

EUR-USD:

Below is an updated EUR/USD price level chart. Our immediate term TRADE and intermediate term TREND levels of support are both at $1.22. Our TRADE resistance level is $1.25. Our call remains that if $1.22 breaks, look out below! We’re not EUR parity folks because we see Eurocrats stepping in to prevent it, however the runway of uncertainty until June 17th elections puts significant downside risk in play. However, we’re well cognizant that the pair could see a bounce on any optimism around discussions concerning any number of proposals on the table, including: Eurobonds, a Pan-European Deposit Guarantee facility, another LTRO, and the ESM.

Call Outs:

Spain: Fitch downgraded Spain by three levels to BBB, within two steps of non-investment grade. (only Moodys is left; S&P already cut).

Troika and Portuguese See Eye to Eye?: The troika said Portugal's bailout remains on track. It said that its fourth review found that the program is making good progress amid continued strong external support. It added that as long as the government continues to implement the measures embedded in the program, Europe will stand ready to support Portugal until it is able to regain market access.

Germany: A poll by German broadcaster ZDF asked if Greece should stay with the EUR? 60% said NO.

PBoC chief highlights support for Eurozone: Chief Zhou Xiaochuan said in comments published on Monday with Chinese Business News that China will continue to buy Eurozone bonds, support the IMF and invest in European infrastructure and privatization programs. However, Zhou also urged Europe to step up its reforms to stem the debt crisis.

But….

China's CIC head sees heightened risk of Eurozone breakup: Lou Jiwei said that he sees mounting risks of a Eurozone breakup. He added that the sovereign wealth fund has scaled back its holdings of stocks and bonds across Europe and also noted that the CIC would be unlikely to invest in jointly-guaranteed Eurobonds if they were introduced as a crisis response measure. The paper said that the comments reflect Beijing's heightened concerns about the manner in which European leaders are dealing with the crisis.

Italy - Tax evasion weighing on recovery: Anna Tarantola, deputy director-general of the Bank of Italy, said that 27.4% of GDP in Italy evades taxation due to underground and criminal economic activities. The WSJ article noted that if the state taxed revenue of more than €400B in unrecorded activity at the 45% tax rate, Italy could eliminate its €2T public debt in less than a decade, or slash it in half to the key 60%-of-GDP level by 2017.

European Commission outlines banking union plan: Dow Jones noted that the European Commission proposed legislation on Wednesday for EU-wide bank recovery and resolution that aims to shift the cost of dealing with bank failures away from taxpayers and onto investors. Banks would be required to draw up resolution plans that set out how they could be quickly wound up if they get into trouble, while national authorities would be given additional powers to intervene when a bank is on the verge of collapse. Under the bail in process, losses could be forced on subordinated bondholders, though the only in the event they are exhausted would senior unsecured creditors be involved (the EC said that forcing creditors to share more of the burden of bank crises in the future could raise bank funding costs by 5-15 bp). The European Commission also proposed the creation of national resolution funds, which would force banks to set aside cash that would be used if they failed. It also recommended that an EU member country would have to lend some of its resolution funds to another state in the event of a broader crisis. Separately, Reuters said that the legislation is unlikely to take effect before 2015.

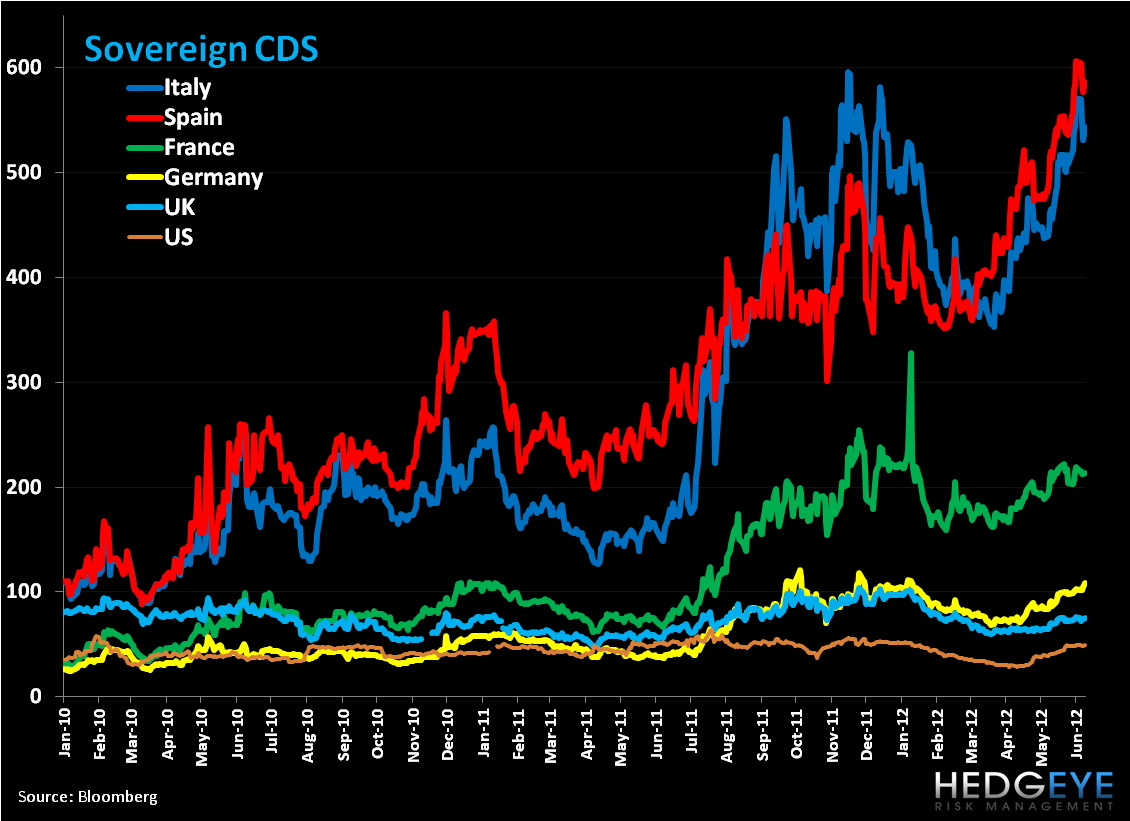

CDS Risk Monitor:

Week-over-week CDS were largely down versus a mixed bag last week. Portugal saw the largest declines in CDS w/w at -88bps to 1089bps, followed by Italy -28bps to 543bps, and Ireland -27bps to 686bps. Germany was one of the gainers that we track, rising +5ps w/w to 108bps.

Data Dump:

PMI Services –

Sweden 47.7 MAY vs 48.6 APR

Spain 41.8 MAY vs 42.1 APR

Eurozone 46.7 MAY vs 46.9 APR

Italy 42.8 MAY vs 42.3 APR

France 45.1 MAY vs 45.3 APR

Germany 51.8 MAY vs 52.2 APR

Russia 54.9 MAY vs 52.6 APR

Ireland 48.9 MAY vs 52.2 APR

Eurozone Composite 46.0 MAY vs 46.7 APR

UK Construction PMI 54.4 MAY vs 55.8 APR

Eurozone PPI 2.6% APR Y/Y (exp. 2.7%) vs 3.5% MAR [0.0% APR M/M (exp. 0.2%) vs 0.5% MAR]

Eurozone Retail Sales -1.0% APR M/M (exp. -0.1%) vs 0.3% MAR [-2.5% APR Y/Y (exp. -1.1%) vs -0.2% MAR]

Eurozone Preliminary Q1 GDP 0.0% Q/Q (UNCH vs previous est.) vs -0.3% in Q4 [-0.1% Y/Y (previous est. 0.0%) vs 0.7% in Q4]

Eurozone Household Consumption 0.0% Q/Q (exp. 0.1%) vs -0.5% in Q4

Eurozone Gross Fixed Capital Formation -1.4% Q/Q (exp. -1.2%) vs -0.4% in Q4

Eurozone Govt Expenditure 0.2% Q/Q (exp. 0.1%) vs -0.1% in Q4

Germany Factory Orders -1.9% APR M/M (exp. -1.1%) vs 3.2% MAR [-3.8% APR Y/Y (exp. -3.8%) vs -0.2% MAR]

Germany Industrial Production -2.2% APR M/M (exp. -1.0%) vs 2.2% MAR [-0.7% APR Y/Y (exp. 0.9%) vs 1.4% MAR]

Germany Exports -1.7% APR M/M (exp. -0.7%) vs -0.8% MAR (1st decline this year)

Germany Imports -4.8% APR M/M (exp. -0.1%) vs 0.9% MAR

UK PMI Services 53.3 MAY vs 53.3 APR

UK BRC Sales Like For Like 1.3% MAY Y/Y vs -3.3% APR

UK Halifax House Prices 0.5% MAY M/M vs -2.3% APR [-0.1% MAY Y/Y vs -0.5% APR]

UK New Car Registrations 7.9% MAY Y/Y vs 3.3% APR

UK PPI Input -2.5% MAY M/M (exp. -1.6%) vs -1.4% APR [0.1% MAY Y/Y (exp. 1.2%) vs 1% APR]

UK PPI Output -0.2% MAY M/M (exp. 0.1%) vs 0.6% APR [2.8% MAY Y/Y (exp. 3.2%) vs 3.2% APR]

France ILO Unemployment Rate 10% in Q1 vs 9.8% in Q4

France Bank of France Business Sentiment 93 MAY vs 94 APR

Spain Industrial Output WDA -8.3% APR Y/Y (exp. -6.5%) vs -7.5% MAR (biggest decline in more than 2 years)

Italy Industrial Production -9.2% APR Y/Y vs -5.6% MAR

Portugal Q1 GDP Final -0.1% Q/Q (UNCH vs previous) and -2.2% Y/Y (UNCH)

Portugal Industrial Sales -6.8% APR Y/Y vs -1.6% MAR

Switzerland Unemployment Rate 3.2% MAY vs 3.2% APR

Switzerland CPI -1.1% MAY Y/Y vs -1.1% APR

Holland CPI 2.5% MAY Y/Y vs 2.8% APR

Holland Industrial Production 0.1% APR Y/Y vs 1.6% MAR

Ireland CPI 1.8% MAY Y/Y vs 1.9% APR

Ireland Industrial Production 2.8% APR Y/Y vs 1.6% MAR

Greece Unemployment Rate 21.9% MAR vs 21.4% FEB (youth unemployment now 52.8%)

Greece CPI 0.9% MAY Y/Y vs 1.5% APR

Greece Industrial Production -2.2% APR Y/Y vs -8.5% MAR

Greece Q1 GDP Final -6.5% Y/Y vs March 15th estimate -6.2%

Finland Q1 GDP 0.8% Q/Q vs 0.0% in Q4 [1.7% Y/Y vs 1.3% in Q4]

Finland Industrial Production -3.2% APR Y/Y vs -4% MAR

Sweden Industrial Production -6.2% APR Y/Y vs -6.9% MAR

Norway Industrial Production 7.5% APR Y/Y vs 2.4% MAR

Norway Credit Indicator Growth 6.7% APR Y/Y vs 7% MAR

Russia CPI 3.6% MAY Y/Y vs 3.6% APR

Romania Retail Sales 3.4% APR Y/Y vs 3.1% MAR

Romania Q1 GDP -0.1% Q/Q vs -0.2% [0.3% Y/Y vs 1.9% in Q4]

Czech Republic Retail Sales -4.1% APR Y/Y vs -0.4% MAR

Hungary Industrial Production -3.1% APR Y/Y (exp. 0.5%) vs 0.6% MAR

Turkey Consumer Prices 8.28% MAY Y/Y (exp. 9%) vs 11.14% APR [-0.21% MAY M/M (exp. 0.40%) vs 1.52% APR]

Turkey Producer Prices 8.06% MAY Y/Y vs 7.65% APR [0.53% MAY M/M vs 0.08% APR]

Interest Rate Decisions:

(6/6) ECB Interest Rate UNCH at 1.00%

(6/6) Poland Base Rate UNCH at 4.75%

(6/7) BOE Interest rate UNCH at 0.50% and Asset Purchase Target on hold at 325B Pounds

The Week Ahead:

Sunday: May UK Lloyds Employment Confidence

Monday: May Germany Wholesale Price Index (June 11-12); May UK RICS House Price Balance; Apr. France Industrial Production, Manufacturing Production; Apr. Spain House Transactions; 1Q Italy GDP - Final

Tuesday: May UK NIESR GDP Estimate; Apr. UK Industrial Production, Manufacturing Production; 1Q France Non-Farm Payrolls - Final

Wednesday: Apr. Eurozone Industrial Production; Jun. Germany 3Q Manpower Employment Outlook (Jun 13-15); May Germany CPI – Final; May France CPI; Apr. France Current Account; May Spain CPI – Final; May Italy CPI – Final; Iceland Sedlabanki Interest Rate

Thursday: ECB Publishes June Monthly Report; May Eurozone CPI; 1Q Eurozone Labour Costs; 1Q Spain House Prices; Apr. Italy General Government Debt; 1Q Greece Unemployment Rate

Friday: May Eurozone 25 New Car Registration; Apr. Eurozone Trade Balance; 1Q Eurozone Employment; Apr. UK Trade Balance; 1Q Spain Labour Costs; Apr. Italy Trade Balance

Extended Calendar Call-Outs:

JUNE: Greece to Identify 5.5% of GDP in Austerity Measures

10 June: France – first round of parliamentary elections

11 June: Spain – Independent auditors contracted by the government are due to report in mid-June on the state of the banks, and a detailed IMF report on the financial system is due

14 June: Eurogroup Meeting

15 June: G20 Summit of Finance Ministers

17 June: Greece – probable date for next general election, France – second round of parliamentary election

18-19 June: G20 Summit in Los Cabos, Mexico

20-21 June: Eurogroup Meeting; Ecofin Meeting in Luxembourg

22 June: Greek T-Bill Redemption for 1.3 Billion EUR

28-29 June: EU Summit in Brussels, aim to formally sign off on growth proposals; EC meets to discuss Institutional Affairs

30 June: Deadline for EU Banks to meet €106B capital target/the 9% Tier 1 capital ratio, Iceland – Presidential election

JULY: France – extraordinary session of parliament in July is due to re-draft the 2013 budget

1 July: ESM to come into force

5 July: ECB governing council meeting

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst