"We must also stand ready to do even more if needed to best achieve our statutory goals of maximum employment and price stability."

–John Williams

Who is John Williams?

That’s a question that would most definitely make Atlas shrug. Not to be confused with all-American pianist and composer John Towner Williams (Star Wars, ET, Sunday Night Football, etc.), this is the lackey Williams who runs the San Francisco Fed alongside his Vice Chair of American Economic Central Planning and Economic Cycle Smoothing, Janet Yellen.

Both of these charlatans were out in full force yesterday ramping up expectations for more of what has not worked – Policies To Inflate commodity and asset prices (Qe). So, thanks to who I am sure your Founding Fathers foresaw as being the leaders of your centrally planned market life, today’s risk management question is will he (Bernanke) or will he not deliver the drugs?

Back to the Global Macro Grind..

So far, my real-time market signals are actually telling me the answer to the question is no. That doesn’t mean the market has it right this morning. But someone always knows something – and, sadly, that’s actually the game that both Bush and Obama have signed off on in this country for the last 12 years – the game within the game.

I work on the inside of the game. But I don’t have the inside information itself. I deal with some of the most sophisticated and accomplished investors in the game. I don’t deal with Washington’s academic elite and/or those with political power. My job is to boil it down to the truth and be right. In the end, from a market pricing perspective, truth trumps storytelling.

The truth is that Janet Yellen might be even worse than Ben Bernanke from a forecasting perspective. That’s saying something. She’s been on the Fed’s Board of Governors since 1994! That makes her very special. Never mind the Housing bubble, she’s overseen a hat trick of Fed sponsored bubbles: Tech, Housing, and now Commodities.

Back to what Bernanke will or will not do today…

Bernanke, of course, is not politicized, but today’s Joint Economic Committee meeting has been completely politicized. He is supposed to be delivering an accountable explanation as to why his economic forecasts are wrong at least 2/3 of the time. Instead, Yellen is pressuring him to whisper sweet nothings about Quantitative Easing.

To review, the Fed’s Congressional mandate is twofold:

- Full Employment

- Price Stability

Instead, their perpetual Big Government Interventions in our markets are delivering:

- Shortened Economic Cycles

- Amplified Market Volatilities

Boom, bust. Boooom, bust. Then, kaboooom!

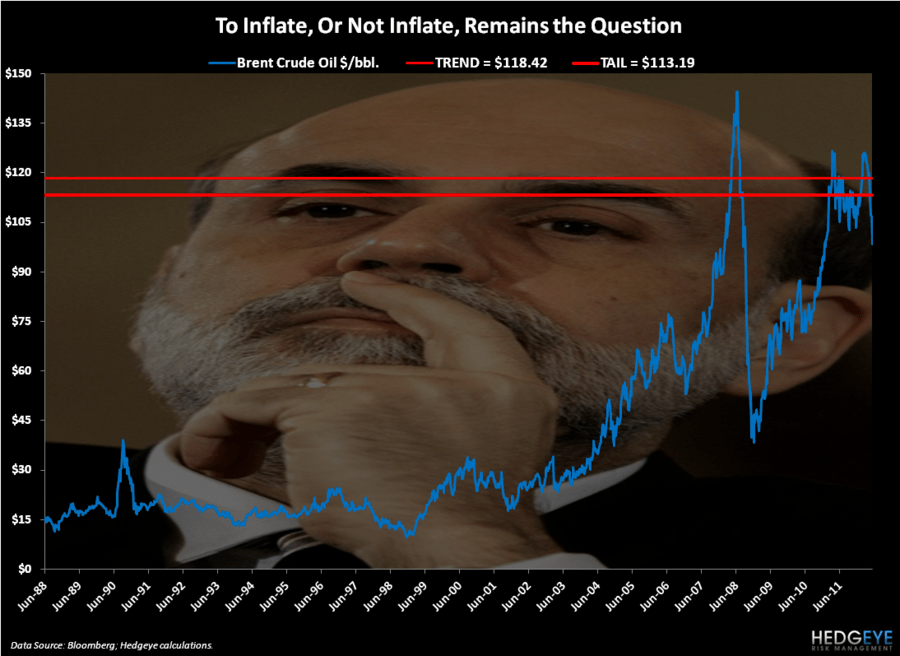

That last part is what we have been making a call on since launching our Q2 Macro Themes of Fed Fighting (The Last War) and Bernanke’s Bubbles (Commodities). Janet Yellen 3 for 3, baby – Tech, bust; Housing, bust; Commodities ka-booom!

I “stand ready” to present 35 slides today in Dallas, Texas (at The Money Show) on why Commodity Bubbles in oil and food in particular are going to continue to pop as the Fed’s broken promises continue to fail.

There is a massive movement in this country towards arresting doing more of what has not worked. And, if you all need a Canadian and his American family to stand on the front lines of this policy making war, get me a red-white-and-blue jersey (and helmet) – I’m already there.

Before I go, I’ll leave you with the real-time signals that are suggesting Bernanke may not deliver on hope today:

- Chinese Equities closed down -0.7% (ahead of their rate cut, which implies growth is really slowing)

- European Equities are up but failing at their most immediate-term TRADE lines of resistance (DAX, CAC, and IBEX)

- Oil prices are down

- Gold is down

- Copper is down

- US Dollar is barely down

The only thing that’s complicated about analyzing all of this at this point is how Bernanke is going to attempt to explain it.

Stand Ready for another Qe. This man is fighting for his political life (Romney says he will fire him). If Bernanke goes there, he’ll put his short-term political career risk ahead of the country’s long-term risk management position. Qe3 will cause Dollar Debauchery. Oil will rise again, and real (inflation adjusted) US, Chinese, and European growth will slow further.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $95.77-102.97, $82.11-82.65, $1.22-1.25, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer