Hold was a little low but not much, so VIP volumes were indeed disappointing. June looks good, however.

Hold was a little low but not much, so VIP volumes were indeed disappointing. However, hold was significantly below last year's. We estimate that total direct play this month accounted for 7.0% of the market, compared with 6.0% in May 2011. The total VIP market held at 2.90% vs. 3.13% in May 2011. Accounting for direct play and theoretical hold of 2.85% in both months, May revenues would have increased 14% YoY. As we’ve discussed, the timing of Golden Week likely had a significant impact on YoY growth, probably around 5%. Going forward, we expect June YoY growth to accelerate to the high teens, assuming normal hold.

While growth decelerated across all segments, Mass continued to show robust growth. VIP volume and slot revenue slowed to 9% compared with 23% and 26%, respectively, over the prior 6 month period. Mass grew 25% YoY, compared to 40% growth over the last 6 months. Mass only grew 1% sequentially in May 2012 versus MoM growth of 15% in May of 2011. This is indicative of the timing shift of Golden Week in 2012.

For the 1st time since July 2009, half the concessionaires (MGM, WYNN, MPEL) posted YoY declines in GGR. May marked the 2nd consecutive month of GGR declines for Wynn and MPEL. Poor GGR performance was driven by RC Junket volume declines at 4 of the 6 concessionaires coupled with low hold and difficult YoY hold comparisons. Part of the deceleration in Mass is due to deceleration of the growth at Galaxy Macau which lapped its May 15, 2011 opening this month. Unless Sands Cotai Central can pick up some of the slack of the harder comps in the coming months, Mass will likely exhibit robust but slower growth in the foreseeable future.

Clearly, the opening of Sands Cotai has been a disappointment. Contrary to the build it and they will come expectation, LVS actually lost 80bps of market share in May. The decrease was largely driven by cannibalization and a low hold of 2.44% across Sands China's portfolio.

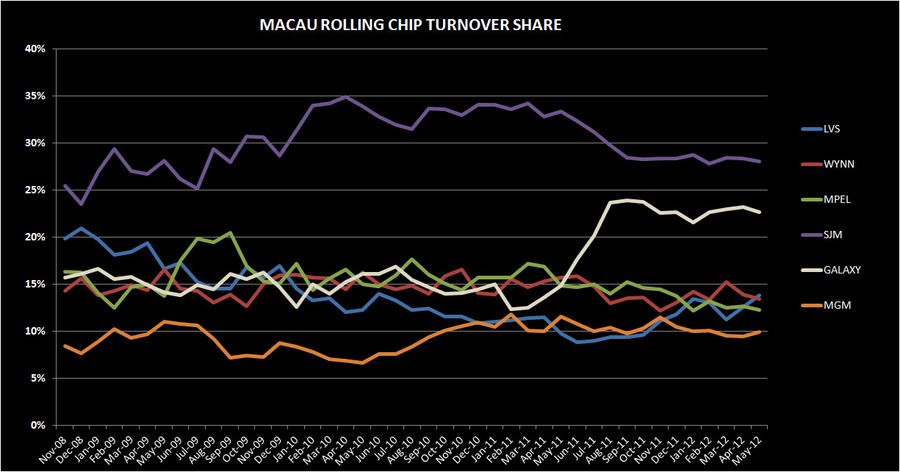

In May, Wynn was the largest market share loser, followed by MPEL, Galaxy, and LVS while MGM and SJM were the share gainers.

Y-o-Y Table Revenue Observations

Total table revenue growth slowed to 7% in May, the slowest growth since July 2009. Mass revenue growth of 25%, compared with 39% growth in the last twelve months. VIP revenues eked out 3% growth, while Junket RC growth fell below the double digit mark (at 9%) for the 1st time since July 2009.

LVS

Table revenues grew 17% YoY, outpacing the market due to the opening of Sands Cotai Central. Sands China's portfolio was negatively impacted by low hold which we estimate adjusted for direct play was only 2.44% in May 2012, compared with 3.31% in May 2011.

- Sands generated a 15% YoY decline mostly due to low hold coupled with VIP volume declines. This should be no surprise given the ‘cannibalization’/reallocation of tables to SCC. The good news is that the entire YoY decline came out of the lower yielding VIP segment.

- Mass was up 5%

- VIP tanked 27% YoY, following a 48% drop in April. We estimate that Sands held at 2.25% in May compared to 2.53% in the same period last year. We assume $234MM/month of direct play or 11% (in-line with what we saw in 1Q12)

- Junket RC was down 14%. This was the 6th consecutive month of YoY declines in VIP RC at the property.

- Venetian table revenues plunged 32% YoY, driven by low hold, a difficult hold comparison and a VIP RC decline

- Mass increased 12%

- VIP tumbled 51% while junket VIP RC decreased 10%

- Assuming 26% direct play in the quarter, hold was 1.96% compared to 3.71% in May 2011, assuming 22% direct play (in-line with 2Q11)

- Four Seasons continued to perform well, growing 74% YoY even in the face of low hold and a difficult hold comparison

- Mass revenues decreased 4%, the 2nd consecutive month of declines

- Junket VIP RC increased 2.6x YoY and VIP revenues soared 100%

- If we assume that monthly direct play volume of ~$650MM is in-line with 1Q12 absolute levels, that implies a direct play percentage of 26% and a hold rate of 2.30%. In comparison, if May 2011 direct play was around 41% then hold is approximately 3.45%.

- For its 1st full month of operations, Sands Cotai Central produced $135MM boosted by high hold. If they held at 2.85%, table revenue would have only reached $106MM or $3.4MM/day. This compares to Venetian's first full month of operations of $137MM in September of 2007, CoD's first full month of operations of $124MM in July 2009, and Galaxy Macau's $160MM in June 2011.

- Mass revenue of $32MM

- VIP revenue of $102MM

- Junket RC volume of $2,567MM

- If we assume that direct play was 15%, hold would have been 3.39%, compared with April's 2.29%.

WYNN

Wynn table revenues fell 6% in May, exhibiting the worst table decline of all 6 concessionaires. Wynn’s hold was below normal but so was last year's comparison.

- Mass only grew 4% while VIP dropped 8%

- Junket RC declined 7%

- Assuming 10% of total VIP play was direct (in-line with 1Q12), we estimate that hold was 2.51% compared to 2.55% last year (assuming 8% direct play – in-line with 2Q11)

MPEL

MPEL table revenue fell 7% due to a 30% YoY drop at Altira. MPEL had moved some tables out of Altira and into CoD’s new junket rooms.

- Altira revenues fell 30%, due to a 32% decrease in VIP and a decline of 12% in Mass

- VIP RC decreased 24%, marking the 6th consecutive month of declines which have averaged 19%

- We estimate that hold was 2.61%, compared to 2.91% in the prior year

- CoD table revenue was up 6%, driven by 22% growth in Mass

- VIP revenue and RC both eked out a 1% gain

- Assuming a 16% direct play level, hold was 2.88% in May compared to 2.98% last year (assuming 13% direct play levels in-line with 2Q11)

SJM

Table revenue fell 3%

- Mass was up 7% offset by a 7% drop in VIP

- Junket RC was down 8%

- Hold was 3.24%, compared with 3.19% last May.

GALAXY

Galaxy posted the best table revenue growth of 60%, with Mass soaring 146% and VIP growing 47%.

- StarWorld table revenues only grew 2% due to a difficult YoY comp

- Mass grew 79% but was offset by a 3% drop in VIP

- Junket RC grew 6%

- Hold was normal at 2.83%, compared with last May's 3.13%

- Galaxy Macau's total table revenues reached $356MM, surpassing the prior high of $339MM set in October 2011. Revenues were up 8% sequentially.

- Mass table revenues hit $77MM, matching the record high in March 2012

- VIP table revenue grew 8% MoM to $279MM - a new monthly record

- Hold was 3.16%

- RC volume of $8.8BN, up 18% MoM and a new record

MGM

Table revenues declined 3.3%

- Mass revenue grew 15%

- VIP revenue fell 7%, while VIP RC dropped 6%

- If direct play was 7%, then May hold was 3.19% compared to 3.16% in May 2011

Sequential Market Share

LVS

LVS share in May was 16.9%, -0.8% MoM. This compares to a 6 month trailing market share of 17.3% and 2011 average share of 15.7%.

- Sands' share was unchanged MoM at 3.2%. For comparison purposes, May share was below 2011's share of 4.6% and 6M trailing average share of 4.2%.

- Mass share was 5.9%

- VIP rev share remained at an all-time low of 2.2%

- RC share decreased 20bps to 2.6%, slightly above the all-time low of 2.4% set in Feb 2012

- Venetian’s share dropped to 6.0%, the properties' lowest share since its first full month of operations. 2011 share was 8.4% and 6 month trailing share was 8.2%.

- VIP share decreased 80bps to 3.8% and mass dropped 290 bps to 12.3% - both new lows

- Junket RC rebounded 50bps from an all-time low to 4.4%

- FS dropped 2.1% points to 3.0%. This compares to 2011 share of 2.2% and 6M trailing average share of 4.2%.

- VIP share declined to 3.4%.

- Mass share was steady MoM at 1.6%

- Junket RC fell 80bps to 3.4%. May marked the 6th month where volumes exceeded those at Sands Macau.

- Sands Cotai Central achieved table market share of 4.3% in May

- Mass share of 4.1%

- VIP share of 4.4%

- Junket RC share of 3.5%

WYNN

Wynn’s share decreased to an all time low of 11.3%, far below its 6-month trailing average of 12.9% and 2011 average of 14.1%. We expect Wynn’s share to continue to struggle in the face of a ramping Sands Cotai Central.

- Mass market share was 8.9%, 10 bps above its all-time low

- VIP market share dropped 2.2% points to 11.9%, only 50 bps away from its all-time low

- Junket RC share fell to 13.4%, a 50bps decline

MPEL

MPEL lost 140bps of share in May to 12.3% which is below their 6 month trailing share of 13.7% and 2011 share of 14.8%.

- Altira share fell 0.3% points to 3.2%, which was below the property’s 2011 share of 5.3% and 6M trailing share of 4.1%

- Mass share fell 30bps to 1.4%

- VIP declined 30bps to 3.9%, the properties’ lowest level since June 2007

- CoD’s share fell 100bps to 8.9%; below its 2011 and 6M trailing share of 9.3% and 9.4%, respectively

- Mass market share tumbled 160bps to 9.9% after hitting an all-time property high in April

- VIP share decreased 90bps to 8.5%

- Junket RC fell 10bps to 7.8%

SJM

SJM was the biggest share gainer in May, up 4% MoM to 29.3% share; in-line with its 2011 average of 29.2% and above its 6M trailing average of 26.8%

- Mass market share rose 90bps to 32.7%

- VIP share jumped 5.1% to 29.1%, its highest level since last May's 32.0%

- Junket RC share fell to 28.0%, lowest level since Sept 2009

GALAXY

Galaxy’s share dropped back below 20.0% to 19.6%, which was still above its 6-month trailing average of 19.2%

- Galaxy Macau share increased 40bps to 11.4% - a new high

- Mass share matched its all-time high of 9.6%

- VIP share increased 20bps to 12.0%, marking an all-time property high

- RC share increased 90bps to 11.9%, a new high

- Starworld share fell 120bps to 7.4%

- Mass share gained 40bps to 3.1%

- VIP share fell 190bps to 8.8%

- RC share fell 130bps to 9.7%, its lowest level since May 2009

MGM

MGM share rose 0.6% to 10.5%, in-line with its 2011 share and above its 6M average of 10.1%

- Mass share rose 1% to 8.0%

- VIP share ticked up 50bps to 10.9%

- Junket RC ticked up 50bps to 9.9%

Slot Revenue

Slot revenue totaled $145MM in May, matching the all-time high set in January 2012.

- As expected, GALAXY grew the most at 73% YoY to $14MM

- MGM had the second best growth at 34% YoY to $25MM

- SJM gained 29% YoY to $19MM

- LVS grew 17% YoY to $39MM

- MPEL fell 7% YoY to $24M

- WYNN lost 27% YoY to $23MM