“China, despite the slump of 2012-2013, has recovered its growth momentum and is economically dominant.”

-Arvind Subramanian

That’s my rumor this morning. Got one? How many more do we need from conflicted and compromised central planners of Keynesian states to keep this no-volume stock market ball in the air? This is really getting sad to watch.

Markets don’t lie; politicians do. The aforementioned quote isn’t a lie; it’s a potential long-term risk management scenario. Looking at our core Growth & Inflation macro model for China in 2013, it’s actually a very credible one.

The forecast comes from the introduction of a book I just started reading called “Eclipse – Living In The Shadow of China’s Economic Dominance.” Since it was published by the Peterson Institute, at least some of the people sleeping in Washington right now have seen it. They don’t even have to read it. The cover is red and shows Obama bowing to Premier Wen.

Back to the Global Macro Grind…

If I’ve written this 100x in the last 5 years, I’ve said it 1000x – if you lose the trust of The People, you will lose the mother’s milk of markets – inflows. The more markets depend on baseless rumors for intraday moves, the less inflows you are going to have.

Actually, never mind inflows – at this point what you should be really worried about as an asset manager are outflows. Some people are stupid with their money. Most people aren’t – at least not after you burn them 3, 4, or 5 times with the same thing.

Q: What is that thing? A: Growth.

If you don’t have growth, a government certainly can’t manufacture it. Remember Obama’s economic “advisors” (Christina Romer and Jared Bernstein) promising a government spending multiplier on $800B of 1.5x? Lol. Thank God they’re both gone.

What you need to do is what the #FairShare crowd can’t handle - let it slow. Then growth slows to a point from which it can recover. When Growth Slows at a slower rate, we start to think about getting long; really long (like we did in 2009).

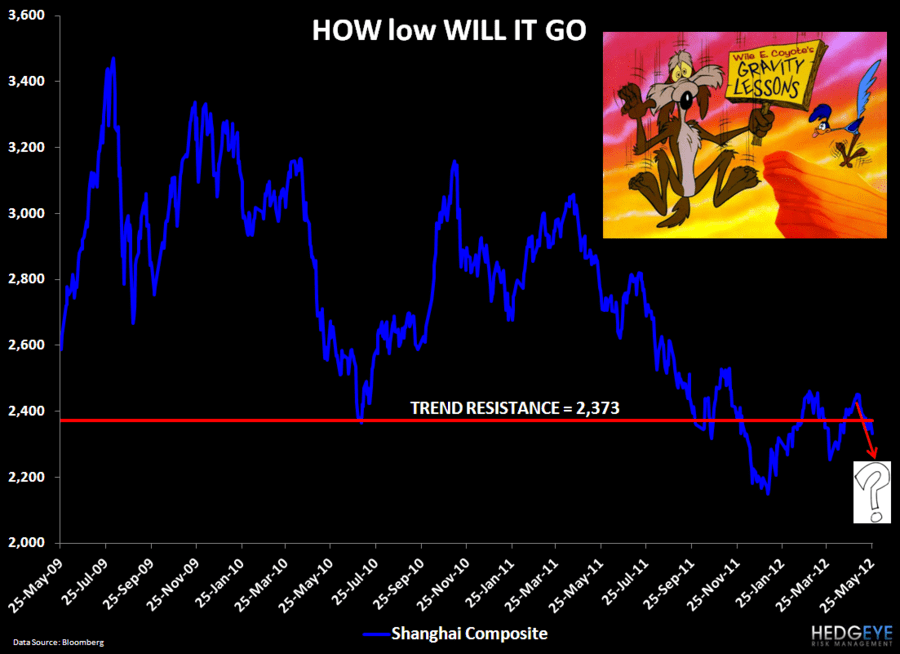

When it comes to Chinese growth, genius observers of the last 2 years of reported news will tell you that it’s slower than where it was in 2009-2010. Newsflash: that’s why the Chinese stock market was down double digits for each of the last 2 years. Markets discount future expectations.

Today, we’re trying to measure the slope of Chinese growth (we model the same for 86 countries in our model) and when it’s most likely to slow at a slower rate. When running our predictive tracking algorithms, we consider Growth & Inflation on all 3 of our risk management durations:

- TRADE (3 weeks or less) = we see Chinese growth slowing at an ACCELERATING rate

- TREND (3 months or more) = we see Chinese growth slowing at a SLOWER rate

- TAIL (3 years or less) = we see Chinese growth re-ACCELERATING at some point in 2013-2014

We use real-time market signals and high-frequency economic data to make risk managed research statements. We don’t take a survey or tell you how Chinese growth “feels.” The only feel I can give you about Global Growth Expectations right now is that they still feel heavy. And they will until Hatzius and Hyman cut their growth estimates to where the growth data currently resides.

Q: What’s the only way out of this thing? A: Strong Dollar.

That’s the only thing that will Deflate The Inflation of commodity prices. That’s the only thing that matters, on the margin, to the 71% of US Consumption growth that drives US GDP. That’s also the biggest thing that will allow China to cut rates, aggressively.

So instead of begging for bailouts and whatever other rumor some Keynesian can concoct in the next 4 hours of trading, let’s keep pressuring the political elite to get out of the way. Out with the academic dogma, we want our Dollar back.

With the US Dollar Index up for 4 consecutive weeks, it’s working.

- American Purchasing Power (USD) is up +4%

- Oil prices are down -15%

- US Consumer Discretionary stocks (XLY) are now the best performing Sector in the S&P 500 (+11.1% YTD)

Get the Dollar right, and you’ll get America right. If we don’t, by 2013 we’ll be stranded on an island of hopeless growth like Japan and Europe are, begging for the Chinese to bail us out.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $104.48-108.43, $81.53-82.61, $1.25-1.27, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer