TODAY’S S&P 500 SET-UP – May 24, 2012

As we look at today’s set up for the S&P 500, the range is 33 points or -2.26% downside to 1289 and 0.24% upside to 1322.

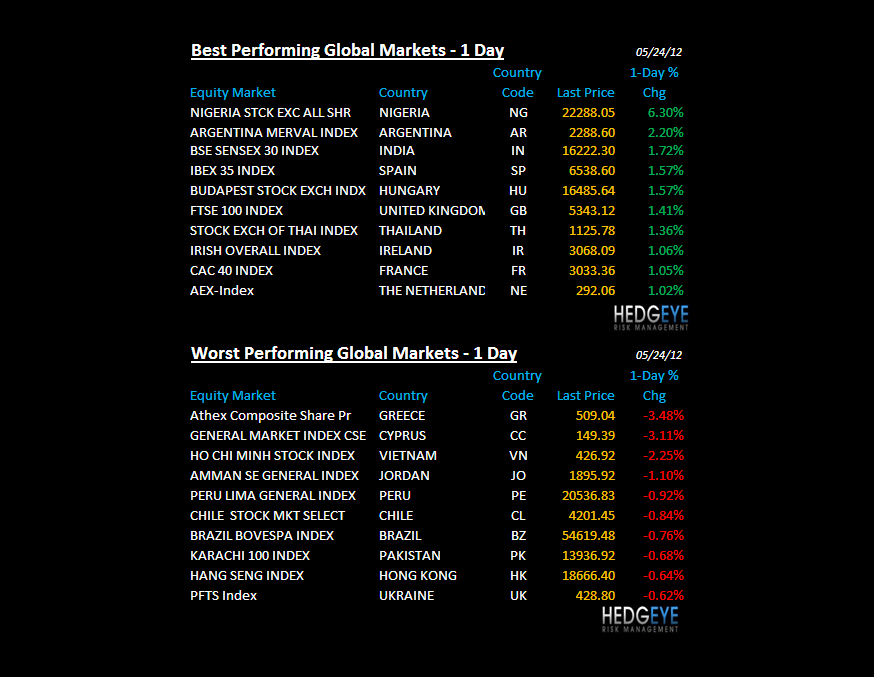

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/23 NYSE 643

- Up from the prior day’s trading of 104

- VOLUME: on 5/23 NYSE 863.01

- Increase versus prior day’s trading of 1.93%

- VIX: as of 5/23 was at 22.33

- Decrease versus most recent day’s trading of -0.67%

- Year-to-date decrease of -4.57%

- SPX PUT/CALL RATIO: as of 05/23 closed at 1.83

- Unchanged from the day prior

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.75

- Increase from prior day’s trading at 1.73

- YIELD CURVE: as of this morning 1.46

- Up from prior day’s trading at 1.44

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Durable Goods Orders, Apr., est. 0.2% (prior -3.9% revised)

- 8:30am: Cap Goods Orders Nondef Ex/Air, Apr., est. 0.8% (prior -0.8%)

- 8:30am: Initial Jobless Claims, week of May 19, est. 370k (prior 370k)

- 8:58am: Markit US PMI prelim., May

- 9:45am: Bloomberg Consumer Comfort, week of May 20

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas change

- 10:30am: Fed’s Dudley to speak on regional economy in New York at Federal Reserve building

- 11am: Kansas City Fed Manf. Activity, May, est. 5 (prior 3)

- 11am: Fed to purchase $1.5b-$2b notes in 2/15/2036 to 5/15/2042 range

- 1pm: Fed’s Dudley to speak at Council on Foreign Relations in New York

- 1pm: U.S. to sell $29b 7-yr notes

GOVERNMENT:

- EPA holds all-day meetings in D.C., Chicago on proposed rule governing greenhouse gas emissions from power generation, 8am

- Federal Deposit Insurance Corp. releases quarterly report on bank industry earnings, 10am

- NOAA issues seasonal hurricane forecast, 11am

- Senate in session, House not in session

- Senate Banking holds hearing on legislation to help homeowners refinance mortgages, 10am

- SEC holds closed meeting on enforcement matters, 2pm

WHAT TO WATCH:

- Hewlett-Packard rose after announced plans to cut 27k jobs, had 2Q profit, sales that beat ests.

- Facebook IPO debacle triggers legal debate over disclosure

- Morgan Stanley’s Gorman said to join Facebook call on price

- J&J-Bayer’s Xarelto rejected by U.S. panel for broader heart use

- Deutsche Telekom CEO says complete sale of T-Mobile USA unlikely

- European services, manufacturing contracted more than forecast in May

- China manufacturing shrank for a 7th month

- U.K. economy shrinks more than est. on building slump

- April durable goods orders may have gained 0.2% after falling 3.9% in March

- International Grains Council issues global wheat, corn, rice production est., 9am

- U.S. Climate Prediction Center issues its preseason Atlantic hurricane forecast

- Europe chiefs clash on Euro bonds as crisis summit bogs down

- German May business confidence fell more than forecast

- AIG can’t pursue some Countrywide claims in $10b lawsuit

- Goldman Sachs’s Trott tells jury Buffett deal was kept secret

- Goldman Sachs AGM

- Bank of America, MERS lose bid to dismiss Texas filing fee suit

- Jury found Google didn’t infringe Oracle’s patents in developing Android software

EARNINGS:

- Royal Bank of Canada (RY CN) 6am, C$1.18

- Flowers Foods (FLO) 6:30am, $0.28

- Toronto-Dominion Bank (TD CN) 6:30am, C$1.77

- Ship Finance International Ltd (SFL), $0.42

- Tiffany & Co (TIF) 7am, $0.69

- HJ Heinz Co (HNZ) 7am, $0.79

- Patterson (PDCO) 7am, $0.57

- Signet Jewelers Ltd (SIG) 7:30am, $0.91

- Monro Muffler Brake (MNRO) 7:30am, $0.35

- Toro Co (TTC) 8:30am, $2.13

- VeriFone Systems (PAY) 4pm, $0.61

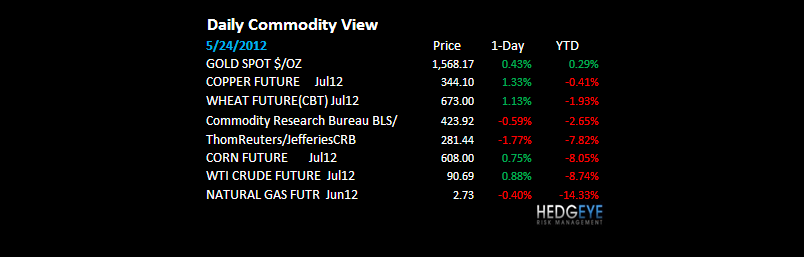

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – interesting that the ISI’s of the world still aren’t talking about things like Commodities crashing as a bearish leading indicator for demand (CRB down -13.8% from Feb top, oversold here, but remains broken).

CURRENCIES

EUROPEAN MARKETS

GERMANY – Germany’s PMI print for May was awful (45 vs 46.2 in April, which was also awful); the DAX would need to close above and hold 6383 to re-capture its 1st line of resistance; not happening despite the fresh wave of rumoring about whatever.

ASIAN MARKETS

CHINA – China’s growth data is not yet slowing at a slower rate, and we think that’s why the Shanghai Comp snapped its TREND line of 2372 again in the last week (sold our long position on that); PMIs are made up, to a degree, but 48.7 for May is what it is, lower than April.

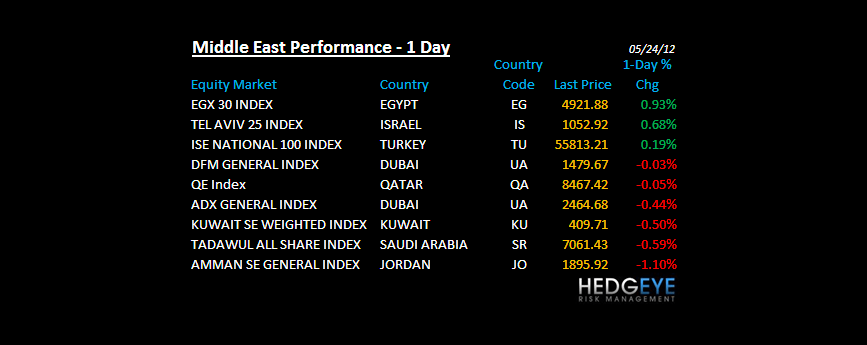

MIDDLE EAST

The Hedgeye Macro Team