“Get the US Dollar right, and you’ll get a lot of big beta in macro right”

Keith McCullough

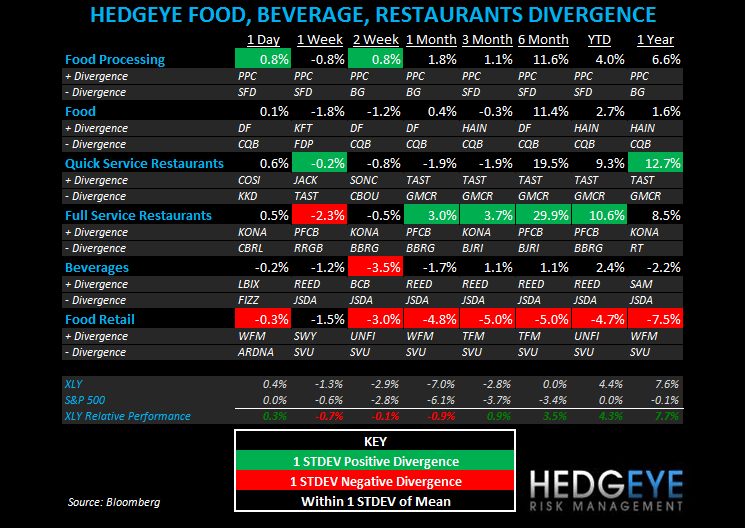

The MACO team has said many times that there has been “plentiful evidence” that the US Dollar has been driving “The Correlation Risk” in Global Macro markets since 2008 - "the US Dollar up means stocks and commodities have arrested their ascent." This has positive intermediate-term implications for Restaurant Industry margins.

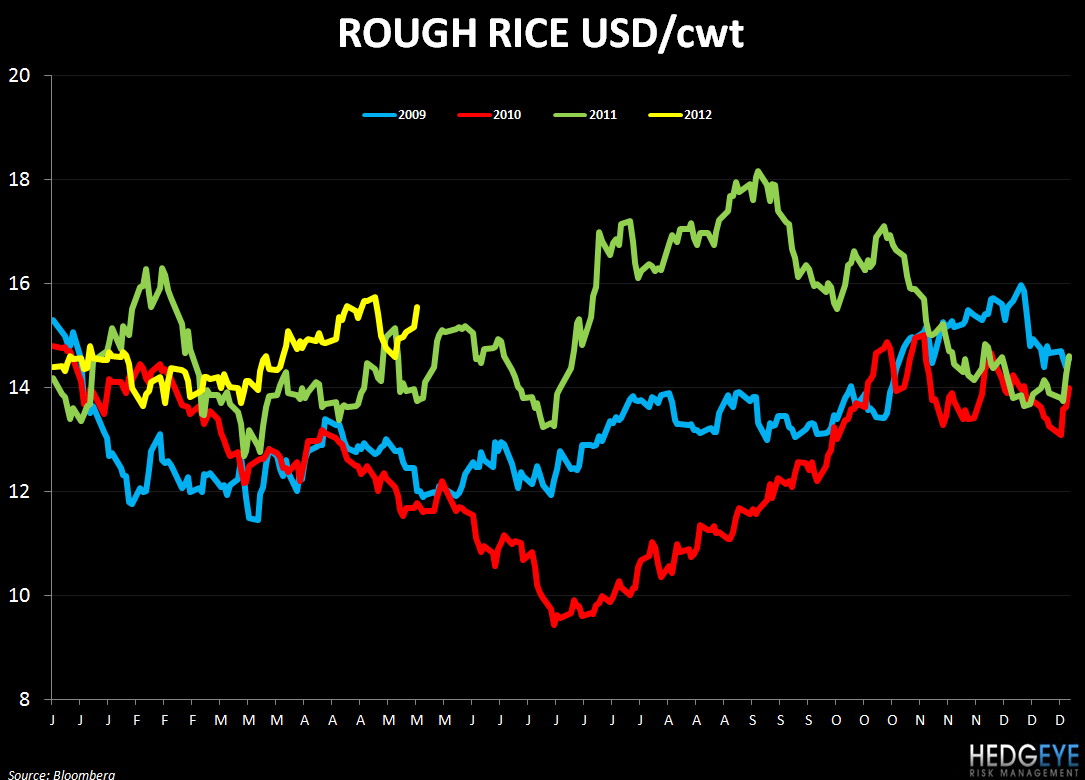

On Monday at the Alltech International Symposium it was suggested that the current world population of 7 billion is supposed to grow to 9 billion by the year 2050, which could require 70 percent more food production than currently is the case. (The amount of food needed will grow by a larger percentage than the population due to a higher standard of living around the world.) This would suggest that there is substantial long-term demand for food and in the overall Ag commodity complex.

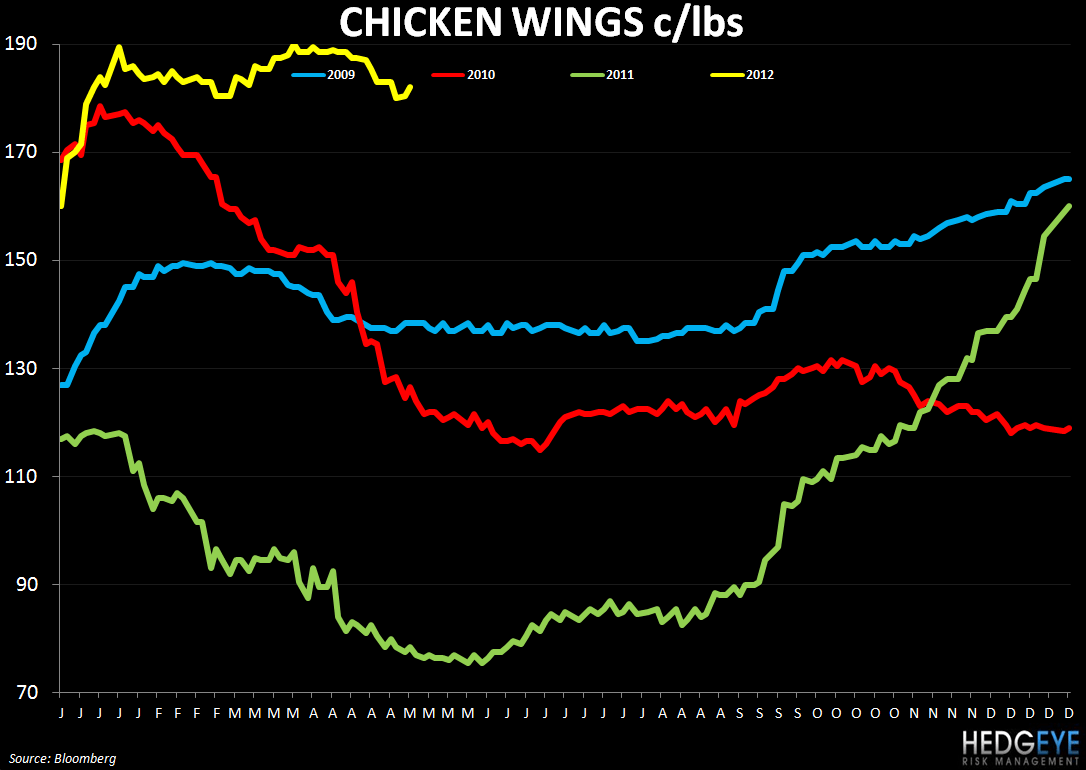

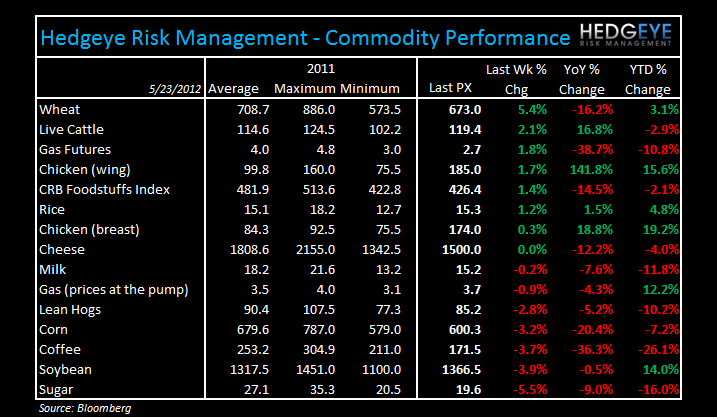

We continue to hit our chicken theme (long SAFM and short BWLD) as corn and commodity prices (corn down and chicken prices up) move in our favor. (See the charts below)

SAFM: While the tone from management has been cautious, we see declining corn prices and tight chicken supply over the next 18 months as strong positives for the stock. SAFM’s superior balance sheet, versus its peers, helps its position as the industry turns. Intermediate term risk is seasonality in the stock Jul-Sep.

BWLD: This stock is highly valued as it one of the few “growth” plays in casual dining. The year-over-year increase in wing prices has a direct impact on EPS that we believe consensus is underestimating. We expect negative FY12 EPS revisions over the next two-three months.