Keith shorted CSH in the virtual portfolio earlier today at $43.85. His quantitative levels show a TRADE (short-term) and TREND (intermediate term) levels of resistance at $44.61 and $45.97, respectively.

Our bearish view on CSH is growing. There are several factors at play here.

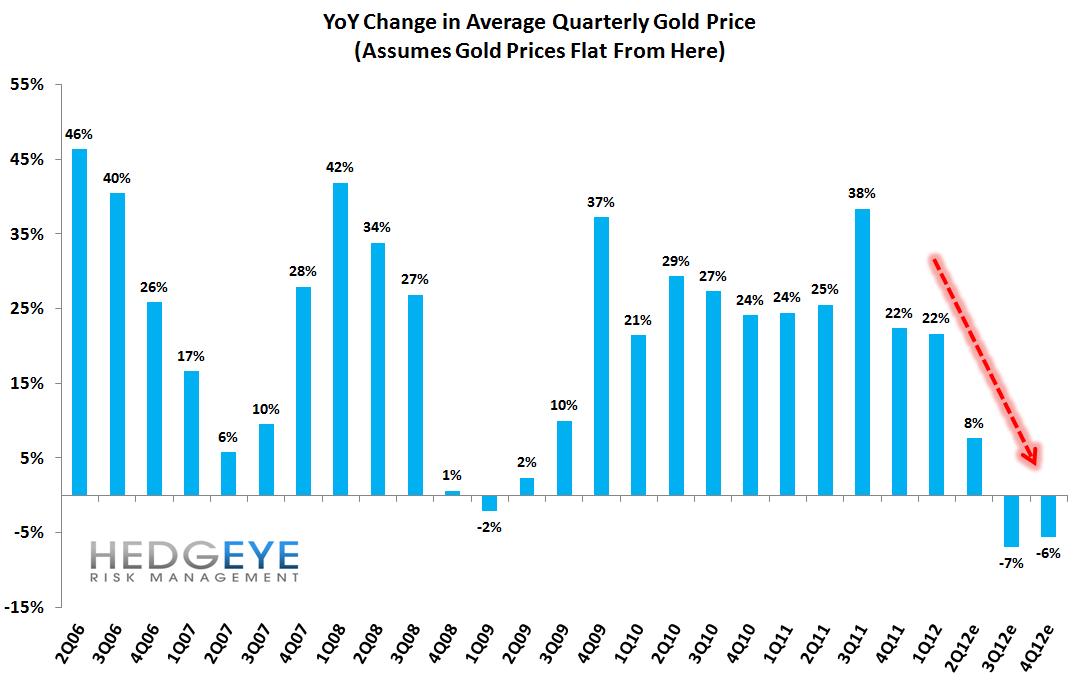

* The YoY price change in gold is poised to roll from a 22% tailwind to an 8% tailwind in 2Q12 and if gold holds at its current level it will be a 7% headwind in 3Q12. A rough heuristic for the revenue model of a pawn store operator is that gold appreciation over the past decade has contributed 9.6%, or just over half, of the overall growth in revenue. We show this in the chart below. For CSH the effect should be more acute, because they hedge out the price of gold six months in advance. This means that when they reported 1Q12 results, they were actually reflecting the 38% 3Q11 YoY tailwind, meaning that gold price tailwinds will slow meaningfully for them for the coming 9 months.

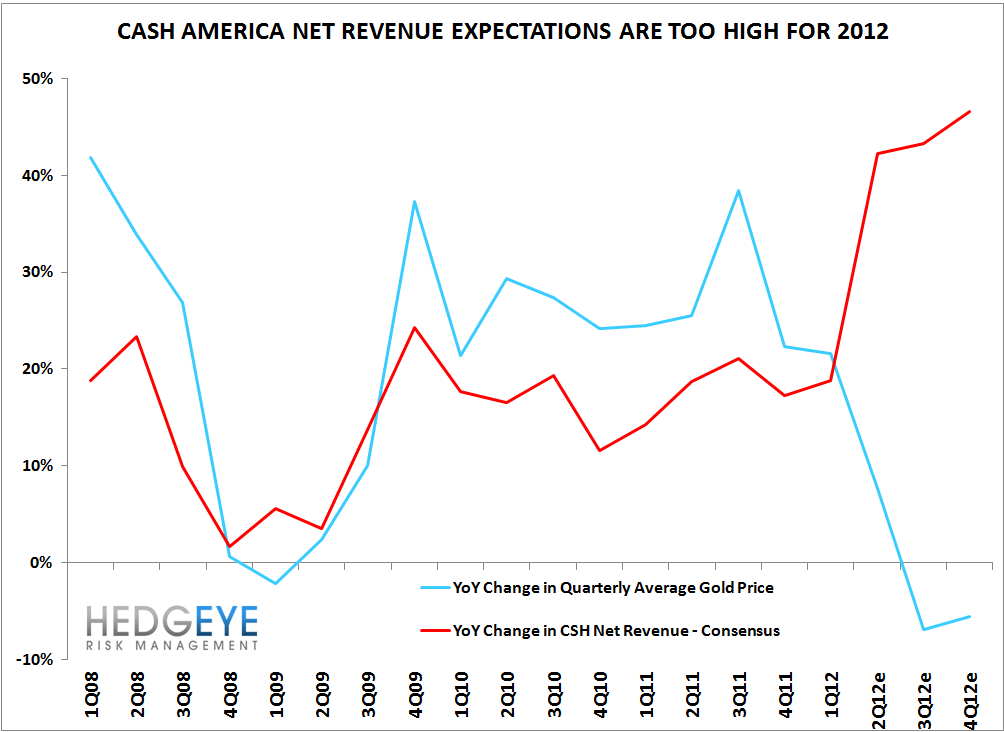

* Judging from the divergence between expectations and reality, the consensus doesn't understand the amount of headwind the company if facing. Consider the net revenue growth expectations the Street is modeling in for the next 3 quarters relative to the headwind from gold.

Source: Factset Estimates, Hedgeye Research

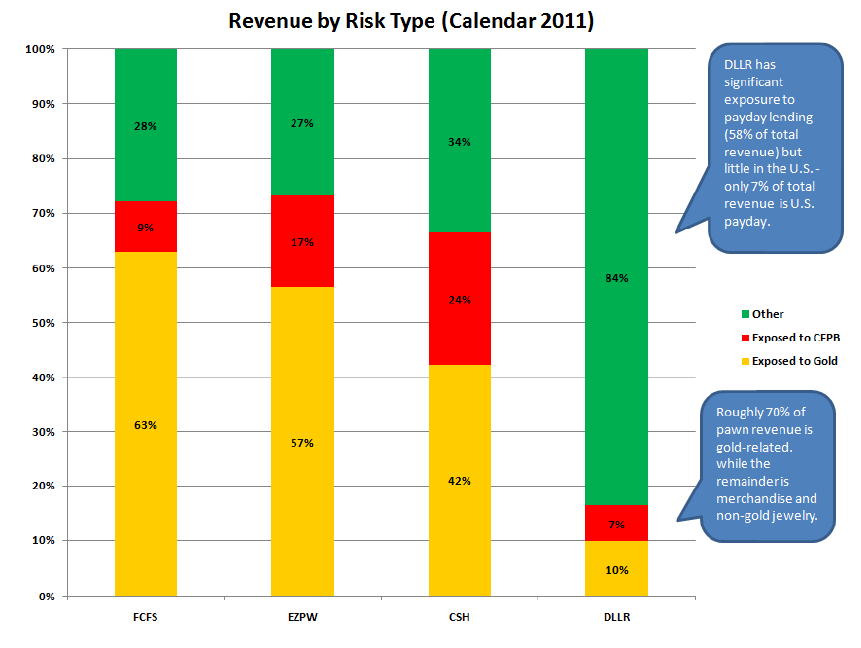

* The other issue at play here is whether gold volumes are drying up for the pawn operators. We wrote a note on this following EZPW's earnings, but to summarize: both FCFS and EZPW spoke to materially declining gold volumes, and EZPW attributed it to their borrower base running out of gold. Cash America came out and denied that they were seeing the same trends in their business, but call us skeptical. The main driver of the falling volumes is the emergence in the last few years of the pop-up gold buyer - ads for these places are now ubiquitous: billboards, radio, tv. These shops are taking share from traditional pawn business like CSH, EZPW and FCFS. A secondary factor is that the borrower base is running out of gold. The rise in the price of gold over the past decade has made for a largely one-way trade: gold leaves the population of pawn borrowers and returns, via scrap, to more affluent customers outside the pawn borrower population.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.