POSITIONS: Long Healthcare (XLV) Long Consumer Discretionary (XLY), Short Industrials (XLI)

I came into today a lot longer than I am now. I sold by my SPY and AAPL as we push toward my Selling Zone.

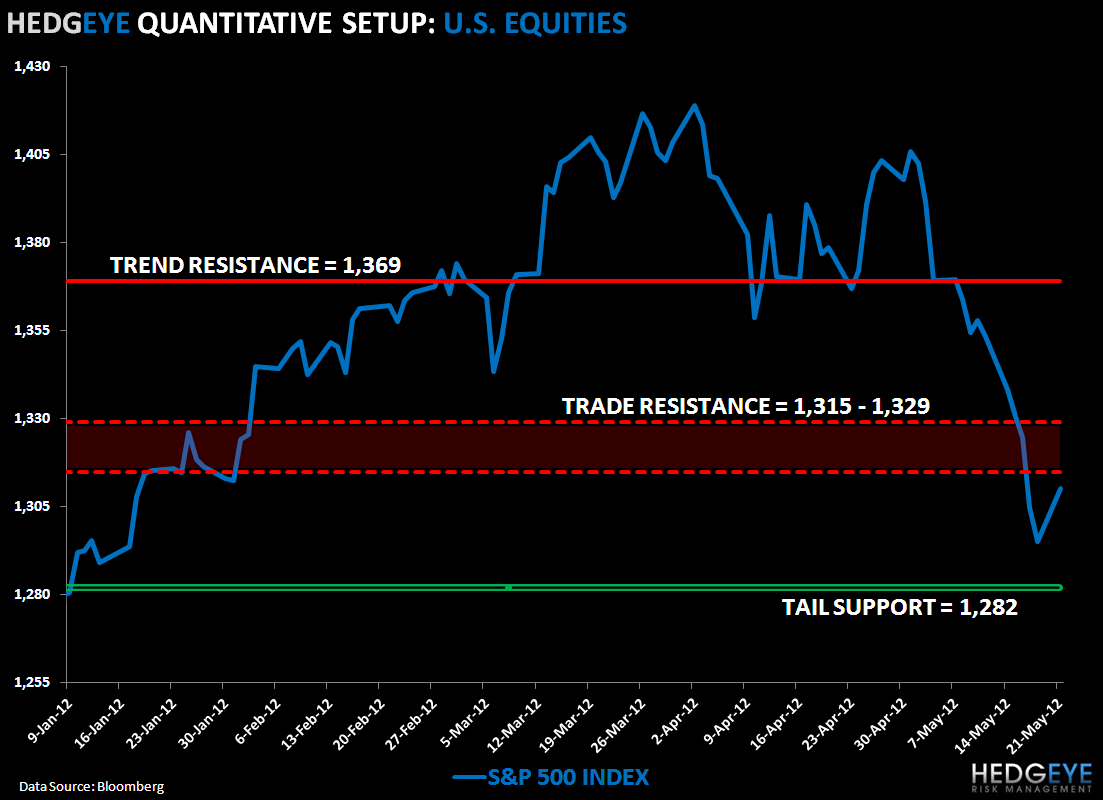

Since Equity Volatility has moved back to bullish TRADE and TREND, I can change the duration and volume assumptions in my immediate-term TRADE calculation in order to generate a range of probabilities instead of a point.

In other words, there are 2 immediate-term TRADE lines (1315 and 1329), and that generates my Selling Zone. On the way up towards that zone I want to be selling longs first, then re-shorting best ideas, selectively.

Across risk management durations that matter most, here are my lines right now:

- Intermediate-term TREND resistance = 1369

- Immediate-term TRADE zone = 1

- Long-term TAIL support = 1282

We held my long-term TAIL of 1282, and that’s the most bullish thing I can tell you. But I am also telling you to sell down gross and/or net exposure on the way up. Unless we see a close > 1369, the intermediate-term view for Q2 remains bearish.

Keep moving out there,

KM

Keith R. McCullough

Chief Executive Officer