We continue to be extremely concerned about the inventory/margin setup for retail in 2H – which plays right into the countercyclical nature of TJX. No surprise that its 1Q metrics look so good. With inventories rising at SKS, JWN and M, earnings are likely to improve from here. TJX will look expensive, and it should.

Conclusion:

Inventory growth continues to be a key concern/theme out of 1Q12 results, which is good for off-price retailers like TJX. As we indicated in our earlier note "Retail: Complacency Today, Hope Tomorrow", while we’ve been seeing inventory growth outpacing sales in the mid-tier (KSS and Macy’s mid-tier business), we’re now seeing sharp negative sales/inventory moves out of the upper tier department store players as well; both JWN & SKS sales/inventory spreads deteriorated sequentially in Q1. TJX and ROST have been on a tear, but the reality is that as long as there are signs of inventory building out there, it will be a bullish set-up for them over the next 12 months. In fact, TJX is at a point in its cycle where it is clearing at high margin (revs +11.3% vs inventory -3%), and we think will revert soon enough to buying higher-priced, higher quality goods that need to find a home (ie Polo and Armani in TJ Maxx). While TJX’s revised guidance remains $0.03 below consensus at the high-end, comp expectations of 2-3% appear conservative. This will likely continue to be like Chinese water torture for the bears, as both earnings, and the stock should grind higher.

What Drove the Beat?

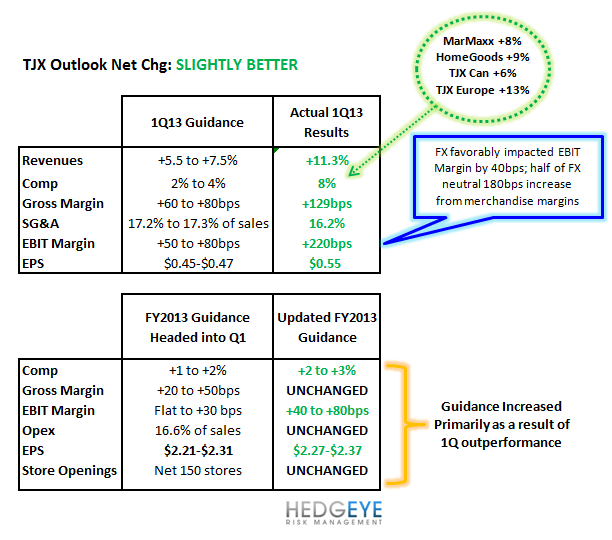

After having originally guided 1Q13 comps to +2-4%, TJX over delivered +8% (which came out on Sales day). This additional $200m+ in sales disproportionately flowed through to gross margin with little incremental SG&A resulting in 90bps expense leverage. 1Q top line resulted from significant improvements in traffic with a slight benefit from an increase in average ticket. FX contributed a favorable 40 bps to the 220bps operating margin expansion. The remaining 180bp was driven by improved merchandise margins, and the remainder was buying and occupancy leverage off an 8% comp. TJX ended the quarter with inventories (-3%) overall and (-7%) on a per store basis resulting in a meaningful 11 point sequential improvement in the sales/inventory spread (now +15%).

Deltas in Forward Looking Commentary?

In order to properly measure performance relative to original expectations, we look at management’s first quarter results relative to management guidance as well as any updates to previously provided full year 2013 outlook:

Highlights from the Call:

Comps: +8% driven by significant increases in traffic with average ticket up slightly

- Above plan sales and record flow through resulted in record profitability

- Saw significant increases in traffic across every division

- Warm weather boosted demand though sales remained strong in regions driven less by weather

- International momentum remains strong

Divisional performance

US Marmaxx comp +8%

US Home goods +9%

TJX Europe: highest first quarter segment profit in history

- Broad based strength in Europe from UK and Ireland, Germany and Poland

- See lots of room for further improvement

- Remain the only major off price retailer in Europe

TJX Canada: comps +6%

- Segment profit improved significantly

- Opened another 6 Marshalls stores in the quarter

SG&A 90bps leverage

- Driven by expense management on above plan comp

- Added very little incremental SG&A to 200mm+ revenue outperformance

EBIT Margin: +220bps

- Strong flow through of above plan sales

- 40 bps due to positive FX impact

- 8% comps would typically drive 120 bps improvement, drove 180 bps increase ex FX

- Merchandise margins drove 90 bps of the 180bps improvement ex FX

- Some buying and occupancy leverage

Inventories: down 7% per store vs. 12% increase last year

Operations:

- Customer transactions have increased mid teens over the past 3 years

- Research shows TJX attracting younger customers

- Market penetration still well below most US department stores

- E-Commerce remains an opportunity to draw customers in the future (E-commerce will not be top line accretive in 2012)

- Plan to grow square footage by 4-5% annually over the next 2 years

- More than 100 markets where there is a TJX or Marmaxx and no Homegoods creating opportunity

- Maintaining 10-13% annual EPS growth guidance

Guidance:

- May is off to a strong start

2012

EPS: $2.27-$2.37; 14% to 19% increase over $1.99 last year (Increase do primarily to 1Q outperformance)

Comps +2-3% vs. original guidance of 1-2%

Pre tax margins 11.1%-11.5% 20-30 bps above original guidance

Share Repurchase: $1.2-$1.3bn in FY13 including $250mm in Q1

2Q guidance

EPS: $0.47-$0.50 cents ($0.01 benefit from FX)

Top line: $5.7-$5.8bn range based on comps +2-4%

May: comps planned to increase 5%, June: flat to up 1%, July: +1-3 %

Gross Margins: 27.2%-27.4%; down 10bps to +10bps YoY, merchandise margins expected to be up, -10bps impact from FX

SG&A: 16.8%-17% range, down 10bps to +10bps YoY (reflects 30 bps of incremental growth investments)

EBIT Margin: 10%-10.4%, down 20bps to +20bps (includes 10bps negative FX impact)

Tax Rate: 38.5% (higher than last year)

Net interest 8m-9m range

Share count of 752 mm shares

Q&A

Marketing and Advertising Spending in 2012:

- Pretty flat though impressions are up leveraging corporate marketing initiatives

- Will be more prominent in 2H

- Have kicked it up for gift giving in Q4

Investment Spending

- Slight increase in 2Q but investments are on plan for the full year

- Corporate expense +$13mm in 1Q, planned to be up 20mm in 2Q with majority in investment spending

- 1H increases in 30-33mm but back half in +10mm range

- Able to leverage SG&A slight in 2H on flat to +1% comp to due timing of investment spending

Debt

- Long term debt ($775mm) with nothing due near term

- No plans at this point in time to increase leverage but remain open

Traffic Increases

- Are seeing new customers in that average age is decreasing a bit

- Large percent of new customers are younger (18-35 range)

- Maintaining the older customer as well

Marmaxx segment margins:

- Improvements coming across the board with new stores and old stores

- Across the country in all demographics

Sourcing:

- High percent of sourcing done in Europe- very specific by country

- Have learned what the mix needs to be by country

- Adding countries to improve assortments- currently 700 people in merchandising department

- 6 or 7 main sourcing offices around the world with additional satellite offices

- Will be growing sourcing team through new hubs and additional buying persons in main offices

- Sourcing team is constantly traveling

Europe:

- Only off-price vehicle in Europe

- Europe has a long runway of opportunity

- Merchants overall in Europe are more seasoned than a year ago which has benefitted

- High increases in traffic patterns in Europe

- More and more opportunity to increase store count- taking advantage of current real estate opportunity

- Now guiding Europe to a 5.2-5.8% segment margin on a 53 week basis, 280-300 bps improvement over last year on a 4-5 comp

- Pleased with current momentum in Europe

- Learning from Europe E-commerce in terms of working online in the off priced sector- learning about average order, basket, communication, etc.

- E-commerce business getting stronger and stronger

- TJX does not perform better in a weaker macro setting

Segment margins hitting record highs

- Planning comp conservatively, every comp is about $0.05

- Strive to beat plan

Category Drivers

- Apparel and Home have been terrific

- Tremendous color changes in fashion this year

- Mens/kids strong against the board

- Buying structure allows team to take advantage of changes in fashion, weather, etc.

Comp Drivers

- Planning for average ticket to be up slightly with most of comps driven by traffic

Rural & Urban type stores

- See more and more possibility for additional stores in rural and urban markets

- Continue to learn and can improve on real estate targeting

- Opportunity for home goods to have urban and rural stores as well- volume of stores is less than chain avg but margin is in line

Homegoods

- Results from buying team executing on the merchandising side

- Starting to see a younger customer with the store being a great vehicle for younger customers getting their first apartment