This note was originally published at 8am on May 01, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We are in bed too much.”

-Franklin D. Roosevelt

That classic FDR quote comes from a dramatic excerpt in Ian Toll’s latest book about WWII, The Pacific Crucible. If you are a history buff, I highly recommend it. The book is very well researched and provides a unique Japanese perspective on how they forced Americans to think differently about globally interconnected risks.

The context of the quote is important. FDR said it in the immediate aftermath of Pearl Harbor when being grilled by Senator Tom Connolly of Texas, “How did it happen that our warships were caught like tame ducks… How did they catch us with our pants down? Where were the patrols.” Roosevelt replied, “I don’t know, Tom. I don’t know.” (page 31)

Unlike most modern day Republican and Democrat “leaders”, Roosevelt didn’t point fingers. He went on to explain that it wasn’t enough not to know. It was time to take the time to re-think US strategy and understand. “They are doing things and saying things during the daytime out there, while we are all in bed.” (page 31)

Back to the Global Macro Grind…

If you want to pretend it’s the 1990s or 2003-2007 bull markets, that’s cool. All you have to do is know where the 50-day moving average is and you won’t miss a thing. Just look at the US Equity futures every morning and go back to bed.

With the US Dollar being debauched (down now for 7 of the last 8 weeks), Risk Managers are starting to pick up on the idea that more QE would only inspire a weaker World Reserve Currency and higher oil prices. That, in turn, will slow growth further.

QE1 may have worked. But QE2 didn’t, and QE3 definitely won’t. Why? Because as the USA gets a short-term “pop” in stock prices, the rest of the world gets asset price inflation (i.e. in their cost of living and/or cost of goods sold) right when they need that the least. Policies To Inflate (from these prices) slows growth and compresses margins.

Global Equity markets have obviously figured this out. With the exception of Venezuela and Egypt, Global Equity prices have been making lower- highs since February-March. The slowdown in US Equities (which somehow were last to figure this out) was much more pronounced in April than it was in that February-March performance period.

Performance period? Qu’est-ce que c’est le performance chasing period? It’s been glaringly obvious that seasonal Institutional performance chasing has called the top in US Equities in Q1 of 4 of the last 5 years. Notwithstanding the no-volume rally in 4 of the last 5 days of the month, here’s how US Equities finished in April:

- SP500 -0.8%

- Nasdaq -1.5%

- Russell2000 -1.6%

From a S&P Sector performance perspective, the complexion of the SP500’s -0.8% loss is interesting:

- Top 3 Sectors = Utilities +1.8%, Consumer Discretionary +1.2%, Consumer Staples +0.3%

- Bottom 3 Sectors = Financials -2.3%, Industrials -1.1%, Tech -1.1%

With our only Global Equity asset allocations being US Utilities and Chinese Equities (up +1.8% and +5.9% for the month, respectively), we were quite pleased with being positioned for US Growth Slowing. The question now is what will please the monthly performance chasers for May?

Can the SP500 make higher-highs for the YTD if Financials and Tech continue to pull back? What happens to the Industrials if Growth Slowing continues? The Sector Studies tell me that the most bullish outcome for May could be Deflating The Inflation. That would be good for American Consumers (good for US Consumer and Healthcare longs).

Deflating The Inflation is already in motion, but you’ll only be able to take it out of market expectations if we stop waking up late every morning begging for Ben Bernanke to bail us out with another QE experiment.

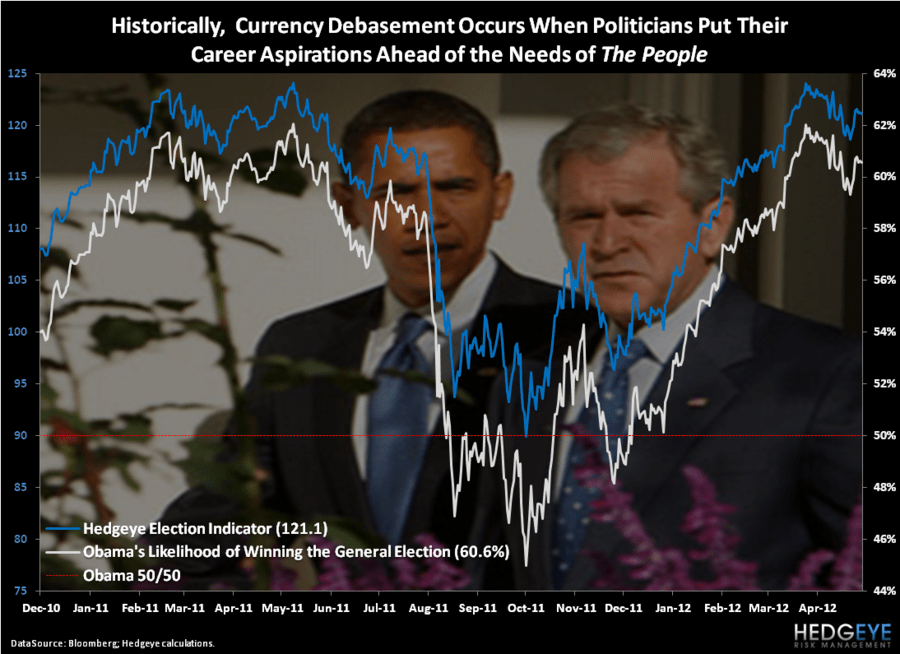

Politicians hate the idea of Deflating The Inflation via a Strong Dollar because that would be bad (in the very short-term) for the stock market. Our Hedgeye Election Indicator has already picked this up (see Chart of The Day). President Obama just had his 1st bullish week in the last 5 (up +130bps week-over-week), primarily because the stock market was up +1.8% last week.

It’s perverse, but it’s real. That’s a big reason why neither Bush or Obama have been advised to back a Strong Dollar Policy.

Causality? Policies To Inflate cause “speculators” to bet on the inflation policies they expect from conflicted and compromised politicians at the Fed and Treasury. From an immediate-term correlation risk perspective, the writing is on the wall too:

Immediate-term TRADE correlations between the US Dollar and:

- SP500 = -0.83

- WTIC Oil = -0.86

- Equity Volatility = +0.93

In other words, as Colonel Jessep would have said, “You want the truth? you can’t handle the truth!” (YouTube video from A Few Good Men http://www.youtube.com/watch?v=5j2F4VcBmeo&noredirect=1). It’s the US Dollar, Stupid.

There should be no politics associated with the Purchasing Power of America’s Currency. Every American who championed the Strong Dollar Periods of 1983-1989 (US Dollar Index Averaged $115.18) and 1993-1999 (US Dollar Index Averaged $92.93), gets this.

At $78.69 this morning, the US Dollar Index is -32% and -15% below those 1980s and 1990s averages. The price of oil is +377% and +465% higher than those 1980s and 1990s Strong Dollar, Strong American GDP Growth Peiods of 4.3% and 3.8%, respectively.

We have a Crisis of Credibility in this country because no one wants to talk about the truth. Our currency is what we buy things with. It’s not something we can borrow respect with. Fighting for it is what should be getting you out of bed.

My immediate-term support and resistance ranges for Gold, Oil (WTIC), US Dollar Index, and the SP500 are now $1647-1667, $103.96-105.23, $78.69-79.22, and 1391-1408, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer