Is the Jobs Data Getting Better or Worse? It Depends Whether You're Looking at the SA or NSA data.

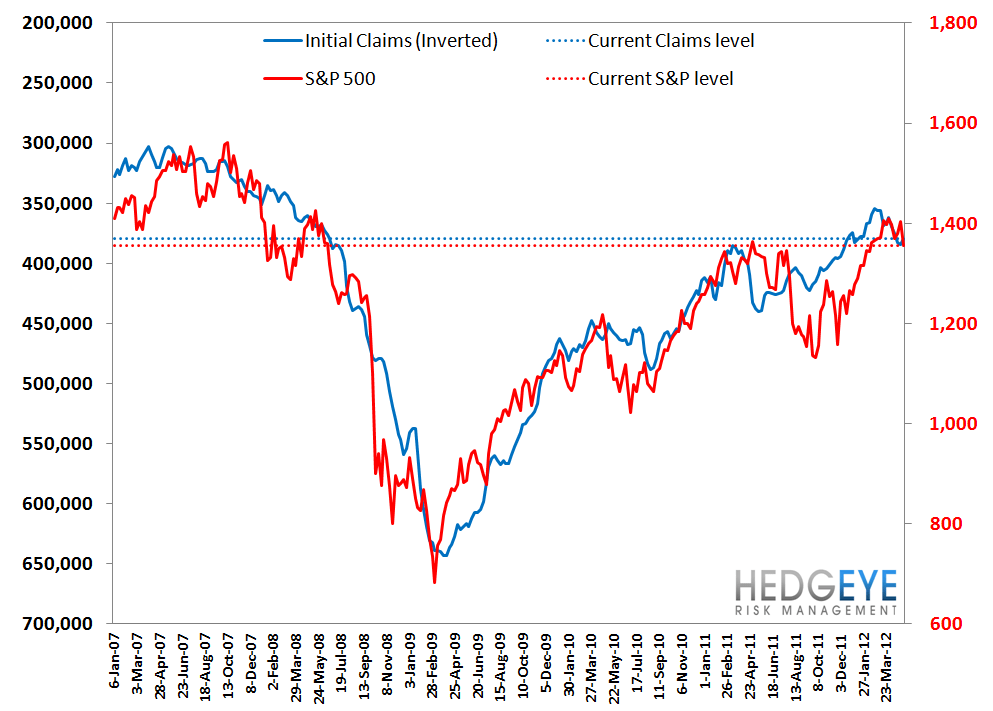

Initial claims rose 2k last week to 367k (falling 1k after a 3k upward revision to last week's data). Rolling claims fell by 5.25k WoW to 379k. On a non-seasonally adjusted basis, claims rose 5k to 338k.

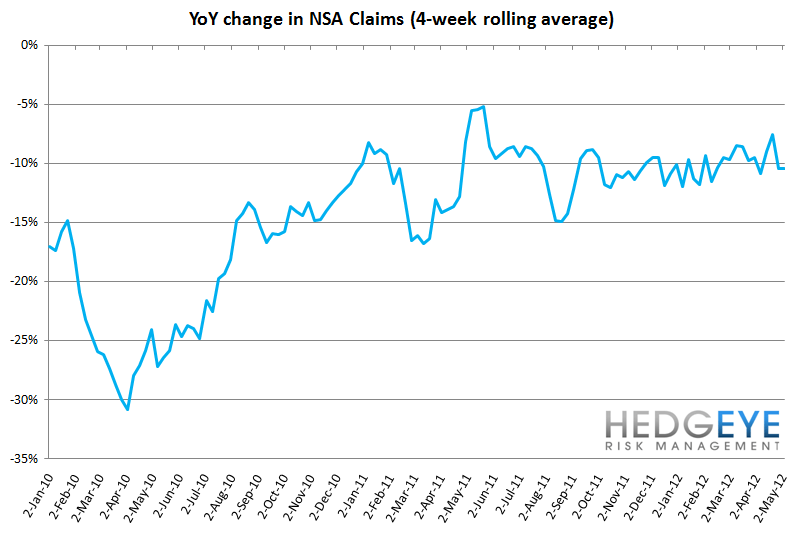

We've been vocal in highlighting the seasonality distortions taking place in the data, and how they'll continue to act as a headwind through the July/August peak effect. That said, it's also important to highlight the other side of this, which is that the real numbers are actually improving. Consider the chart below, which shows the year-over-year change in the non-seasonally adjusted data. By this measure, the data continues to steadily improve at a rate of roughly 10% per year, indicating the underlying health of the jobs market remains on track. Nevertheless, we believe that a majority of investors rely primarily on the printed, seasonally-adjusted number, and, as such, regard the environment as moving sideways to up.

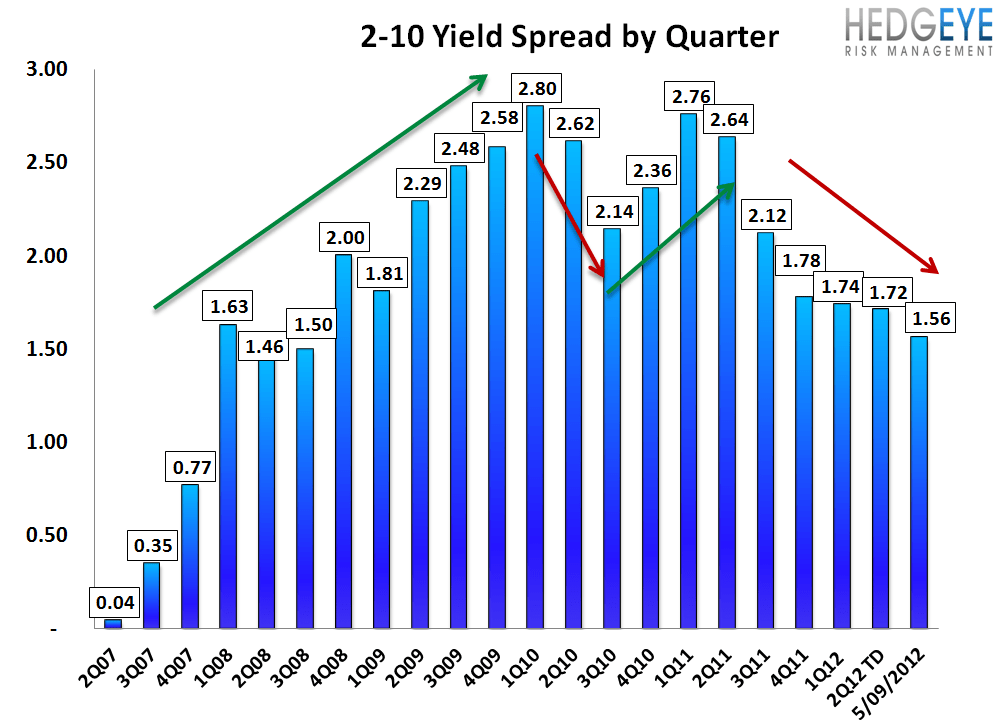

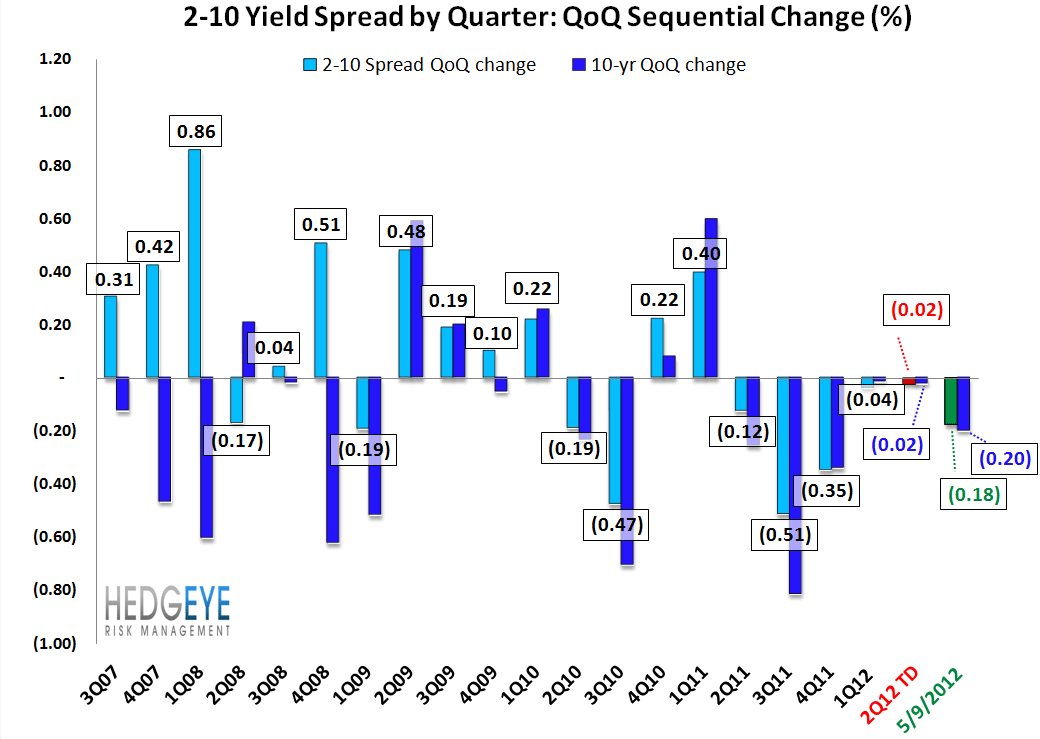

2-10 Spread

The 2-10 spread tightened 9 bps versus last week to 156 bps as of yesterday. The ten-year bond yield increased 10 bps to 182 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.