It’s about time. KSS is finally taking steps to adjust its pricing strategy a full quarter after JCP implemented its new EDLP approach in February. We’re rarely (if ever) a fan of reactive strategies and this one is no different. KSS will now be more aggressively fighting for share – that’s great, but others have already been taking it for the last 3-months now such as Macy’s, the off-pricers (TJX/ROST), etc. Increased competition in the mid-tier that will ultimately drive increased margin pressure is here and officially heating up. This isn’t good for KSS, or the companies that rely heavily on this channel for distribution such as CRI, HBI, GIL to name a few.

That said, KSS posted a very low quality SG&A driven beat for the quarter with both revenues and gross margins coming in soft. A few points of note here:

- Revenues were light. We knew that last Thursday and now KSS is going to try to drive traffic with lower pricing. This didn’t work out so well for JCP. We expect an uphill battle ahead for KSS as well. Not good.

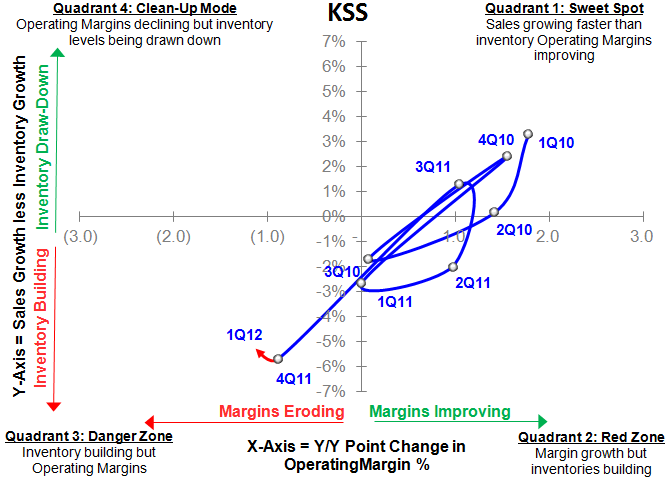

- Gross margins also came in below expectations. While some portion of this degradation was due to the new pricing initiative, KSS’ sales/inventory spread is virtually unchanged and still among the worst in the mid-tier. That’s very gross margin bearish over the intermediate-term.

- SG&A was the saving grace in the quarter coming in $66mm lower yy. We’d prefer to see KSS invest in remodeling some of its tired store base rather than pulling this lever so heavily to make EPS. It may indeed help manage earnings near-term, but that’s no good for F13 earnings growth sustainability.

All in, KSS is guiding Q2 down, but maintaining full-year expectations implying a more bullish view on 2H results. A strategy change of this magnitude is hardly a 1-qtr transformation – just ask Ron Johnson. This not only takes up the risk embedded in management’s guidance substantially, but it also increases the mid-tier competitive environment.

Here are a few more details regarding Q1 results:

Pricing: the newly implemented lower price strategy resulted in gross margins -220bps vs. guidance of -160E & the street -151E.

Opex: KSS beat this morning on a ~$70mm reduction in SG&A spend to offset comps coming in light (+0.2% vs +1E).

Core Contracting: E-commerce sales were not given in the press release, but if we assume 10% growth in 1Q12 (on 40% growth in FY2011), new store sales suggest the core business contracted -0.2%.

Guidance: 2Q guidance per the press release is $0.09-$0.17 below consensus at $0.96-$1.02 vs. $1.13E driven by sales +2%-3% vs. +3.1E and comps flat to +1% vs. +1.2E. The delta seems to be primarily attributable to lower

priced sales driving the top line. The street is looking for Q2 Gross Margins to be -94bps- they may come in closer to -150bps. For the full year, KSS reiterated EPS of $4.75 vs. $4.74E suggesting some back half improvement

relative to expectations. Guidance suggests 2H earnings of $3.10-$3.16 vs. $3.03E which seems to be driven by better positioning for back to school and the lower pricing.

Inventories: Inventories were +7% in 1Q12 vs. +5% in 4Q11. As a result of first quarter revenues +2% vs. slightly negative in 4Q11, the sales/inventory spread improved 1 pt sequentially though remains -5%.

Casey Flavin

Director

Matt Darula

Analyst