“American and British pilots were forced to learn about this lethal athlete the hard way.”

-Ian Toll

Don’t blame the pilots. Blame the politicians. They were willfully blind to obvious risks and put our bravest in the sky anyway. That’s one of the key risk management and leadership lessons I learned from Ian Toll’s excellent new book about WWII, Pacific Crucible.

“The Mitsubishi A6M Zero was a dog-fighting champion, and aerial acrobat that out-turned, out-climbed, and out-maneuvered any fighter plane the Allies could send against it… The Zero had been placed in service in the summer of 1940, almost 18 months before Pearl Harbor… it was yet another example of the fatal hubris of the West in the face of plentiful evidence..” (pages 52-53)

I read about war because it educates me on winning and losing. Every decision counts. Decision processes matter. There has been “plentiful evidence” that the US Dollar has been driving The Correlation Risk in Global Macro markets since 2007-2008. There has also been an outright obfuscation of facts by Western Academics who have chosen to ignore it. It’s un-objective and un-American.

Back to the Global Macro Grind…

The US Dollar is up for the 7thconsecutive day and US Stock Futures are indicated down for the 7thconsecutive day. There is absolutely zero irony in this causal relationship. Policy expectations drive currency prices.

In the absence of immediate-term expectations for an iQe4 upgrade of Gold and Oil price inflation from Ben Bernanke, the US Dollar has arrested its decline – and stocks and commodities have arrested their ascent.

Here’s a real-time update on the surreal Correlation Risk (inverse correlations between the USD and asset prices) developing:

- SP500 = -0.90

- Euro Stoxx = -0.92

- CRB Commodities Index = -0.94

- WTIC Oil = -0.89

- Gold = -0.89

- US Equity Volatility (VIX) = +0.93

Yes, you’ll notice that in the Romper Room that has become Keynesian Economic Policy outcomes, one of these things is not like the other – one of these things just doesn’t belong. It’s called volatility.

The US Federal Reserve has a 2-stroke mandate:

- Price “stability”

- Full Employment

We have neither. We have price volatility like the world has never seen. And we have forced American Pilots of other people’s hard earned moneys to chase their own tails of performance going after short-term and short-sighted Policies To Inflate.

As US Dollar Debauchery has only proven to Slow Global Economic Growth via accelerating short-term food and energy price inflations, now world markets have to deal with the other short-term side of the trade:

- Growth Slowing (until it slows at a slower rate)

- Deflating The Inflation (Bernanke’s Bubbles in Oil, Gold, etc. are popping)

When these 2 things are happening at the same time, you just cannot ignore the capital losses. They happen real fast.

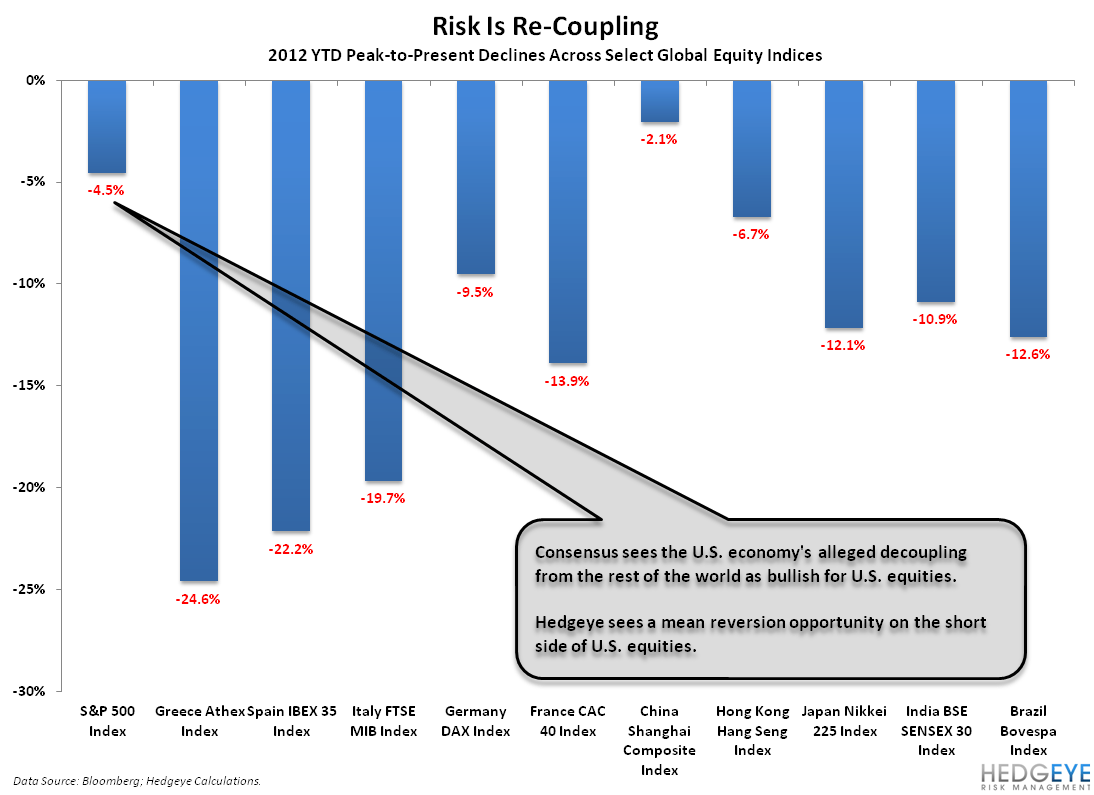

That said, what’s been fascinating about this -4.6% draw-down in the SP500 from its April 2nd, 2012 top (capital loss from the Russell2000 March 26th, 2012 top = -6.9%) isn’t the absolute performance impact, but the Storytelling.

The Most Read (Bloomberg) headline this morning epitomizes the storytelling of the Old Wall: “Dow Falls For 6th Day In Longest Losing Streak Since August On Greece.”

On Greece? C’mon. Americans in this profession are better than that.

You can look at real-time market signals (leading indicators) in 2-ways at this stage of the Fed Fight:

- What’s happened on the margin (draw-downs) from the YTD tops in February-April

- What’s happened YTD

The YTD thing is all about the Storytelling. Just don’t do it with my money. Last I checked, the SP500 is still down -13.5% from its willfully blind 2007 high and needs to be up almost +16% (from here) just to get The People and their 301ks back to break-even.

Everything that happens on the margin in markets matters most to the American and Global Macro Pilots who are trying to manage your money’s real-time risks. What happens on the margin is what drives fear and greed. It’s also what builds or destroys confidence.

If you don’t have planes or markets that the pilots can trust, you’re one step closer to losing whatever is left of the money they are willing to flow back to the politicized decision making process that’s driving markets.

Bottoms are processes, not points. We humbly suggest you fly these risky skies of Federal Reserve sponsored Price Volatility with the credible analytical sources out there who have actually landed the planes for the last 5 years.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, EUR/USD, and the SP500 are now $1, $110.23-113.89, $79.42-80.28, $1.29-1.31, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer