“The Dollar is our currency, but it’s your problem.”

-John Connolly, US Treasury Secretary (1971)

That’s the quote Jim Rickards uses to start Chapter 5 of Currency Wars. From an economic history perspective, it’s a critical quote to contextualize as President Richard Nixon was the first Republican President to go all-in Keynesian.

I’m not a Republican or Democrat. I am Canadian. So sometimes I just have to laugh when Republicans blame Obama for everything. It’s as if these partisan political pundits think we are dumb enough to believe that the likes of Nixon and Bush didn’t uphold the same monetary and fiscal policies to debauch the Dollar.

At least Nixon admitted it when he said plainly, “we’re all Keynesians now.” But are we? Inquiring minds in this country would like to know. Are we as numb to economic reality as the economically partisan media? Being Keynesian (Republican or Democrat) is partisan you know. And that probably had something to do with Republican veteran Lugar losing to the Tea Party in Indiana.

Back to the Global Macro Grind…

You can blame Greece or Canada at this point, but the market doesn’t care to hear the excuses. The global economy is as interconnected as it has been for the last 5 years. The idea of “de-coupling” is only something the Sell-Side could make up.

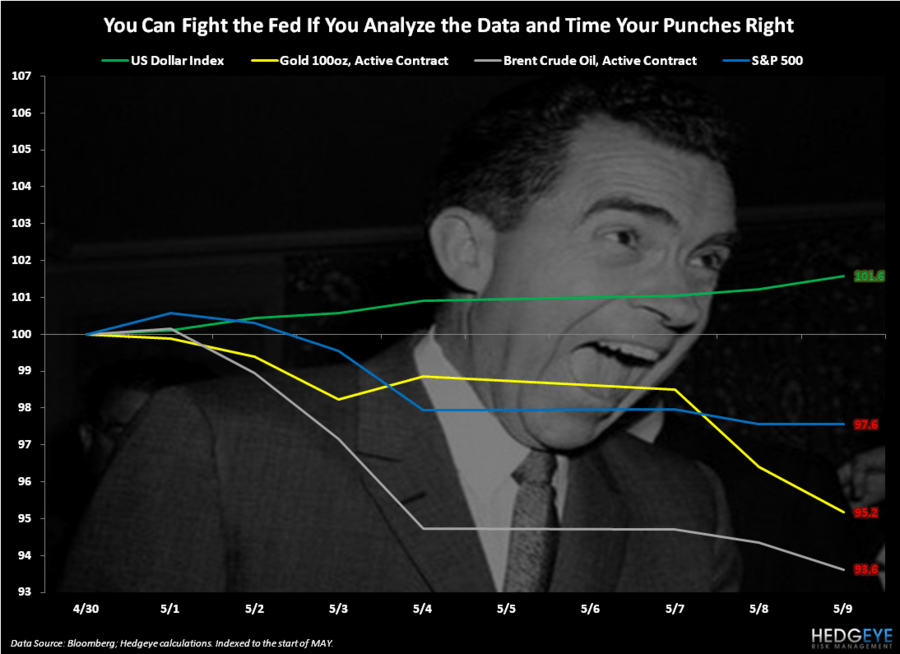

If you didn’t know that the US Dollar is still the world’s reserve currency and that its daily, weekly, and monthly moves are driving what we call The Correlation Risk, now you know.

The US Dollar Index is having its 6th consecutive up day (touching $80 this morning), and one of our major Global Macro Theme calls for Q2 2012, Bernanke’s Bubbles (as in Commodities), are popping.

Since the Old Wall begged for Bernanke to do it, market expectations became addicted to it. Now it, as in “It’s Your Problem”, is on the tape.

Deflating The Inflation of easy money Commodity bubbles in Gold, Oil, etc. are riding the following immediate-term TRADE correlations to the US Dollar:

- Gold -0.85

- Palladium -0.81

- Copper -0.67

- Oil -0.84

- Heating Oil -0.82

- Soybeans -0.79

If you want to call these mathematical ironies, you can. As a matter of fact, you can call anything in this profession whatever you want to call it until you have to report your performance results back to your clients. If you are just a pundit, not held accountable to the TimeStamps of what you say and when, I can’t help you from yourself. Twitter’s gotcha!

In our 50 slide Q2 Global Macro Themes Deck (April 2012) we walked through the Top 10 Bernanke Bubbles (email if you’d like to review it with refreshed risk management levels).

The aforementioned immediate-term TRADE correlations anchor on 6 commodities. If you want to look at The Correlation Risk from a bigger picture perspective, here’s how the USD Index is trending versus some fairly major stuff:

- CRB All-Commodities Index (19 Commodities) = -0.93

- S&P 500 = -0.85

- Euro Stoxx 600 = -0.84

“It’s Your Problem” or its your opportunity now. It’s a major performance problem if you are long anything US, European, or Japanese Equities (all Keynesian Policy Bubbles) or commodities. It has been since the middle of March.

Now plenty people who are long Gold (I have a zip lock bag of the stuff in my desk, fyi) will quickly say that’s precisely why they are long Gold – because it’s “protection against all the money printing and Keynesian central planners” of the world.

Fair e-nuff.

But what if the world is pricing in an end to the Nixonian madness? They did in the early 1980’s. What if we are on the verge of actually getting off the iQe drugs? Gold being up for 12 consecutive years naturally implies some mean reversion risk to the idea that Americans are dumb enough to vote for Dollar Debauchery for much longer.

In addition to their Keynesian economic policy making teams, Bush and Obama have one thing in common – Ben Bernanke. This is not unlike what Nixon and Carter had in common – Arthur Burns (who was also tasked, politically, with devaluing the Dollar and monetizing US Treasury debt).

Got Causality?

- Dollar Debauchery in both the 1970’s and 2000’s perpetuated commodity price inflation

- Dollar Debauchery in both the 1970s and 2000’s perpetuated fear-mongering by policy makers to back their policies

- Dollar Debauchery in both the 1970s and 2000’s perpetuated a lack of confidence/trust and employment growth

Both GDP Growth and US Employment Growth were as nasty as they have ever been (by decade) in both the Nixon/Carter and Bush/Obama periods of raging Keynesian Economic policy influence.

So, here’s a little reminder from little old me in New Haven, CT this morning to all of the Keynesians, from Larry Summers to Ben Bernanke, and all of their offspring – It’s Your Problem now. If that sounds like I am picking a fight, that’s old news. I did that in our April Themes presentation too. We are officially Fighting The Fed (and winning).

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, Euro (EUR/USD), and the SP500 are now $1, $110.92-113.87, $79.42-79.88, $1.29-1.31, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer