McDonald’s reported a global comparable sales rise of 3.3% in April, which represented a slowdown from March on a two-year average basis. Four weeks ago, management told us that it expected global comps to come in at 4%. The 3.3% print suggests that the last ten days of the month fell below management expectations.

This was a disappointing number for McDonald’s. The Hedgeye Macro Team’s “Global Growth Slowing” theme is being confirmed by this April number as the U.S. and APMEA missed expectations. This disappointment is driving the stock lower. Given the significant calendar adjustment, the underlying trends may not be quite as significant as the headline numbers suggest but clearly these numbers are calling for a resetting of investor expectations; McDonald’s is unlikely to astound the investment community with its same-store sales numbers this summer. We still see McDonald’s as the QSR leader in the U.S. but, even in that position of power, the company is having difficulty maintaining its traffic trends.

With inflation pressuring margins, particularly in the United States, and 3% of price flowing through the P&L, sales trends are taking on a higher degree of importance for investors. We are looking for management to offer some more definite guidance on how it will comp the comps this summer.

United States

U.S. comparable sales rose 3.3% in April versus +4.8% consensus as the company had its first full month of the Extra Value Menu. With price running at 3%, traffic trends are weak in McDonald’s domestic business. The calendar impact (one less Friday and one less Saturday than April 2011) seems to have dressed down the headline numbers but we remain concerned about whether the company can comp the comps this summer. As we wrote on 4/23: “The evidence suggests that beverages are increasingly becoming a less important part of the vocabulary from McDonald’s’ management team. With that in mind, foremost in our thoughts is what the company’s strategy will be to maintain top-line momentum over the next few months.”

Europe

Europe exceeded analyst expectations in April, coming in at 3.5% versus +3.2% consensus. Macro continues to be the most important factor in Europe. Europe represents 40% of total revenues and 39% of total operating profit for McDonald’s. While the print exceeded expectations, the two-year average did decline and continuing turmoil in Europe remains a business risk for the company.

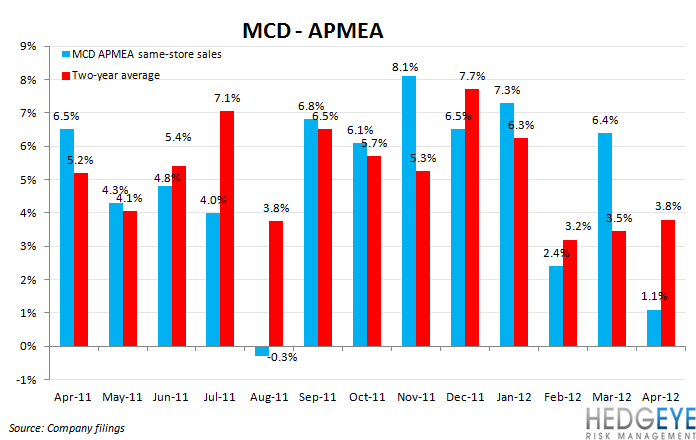

APMEA

Positive results in China were offset by negative comps in Japan as APMEA reported 1.1% same-store sales versus 1.9% consensus. Much of McDonald’s long-term growth hinges on its APMEA division but, in the near-term, we expect the company’s fortunes in U.S. and Europe to dictate the stock’s performance.

Howard Penney

Managing Director

Rory Green

Analyst