Employment data released this morning by the Bureau of Labor Statistics were relatively bullish for QSR versus Casual Dining. However, hiring trends within the greater Leisure & Hospitality industry, show that restaurant hiring may slow more meaningfully in April.

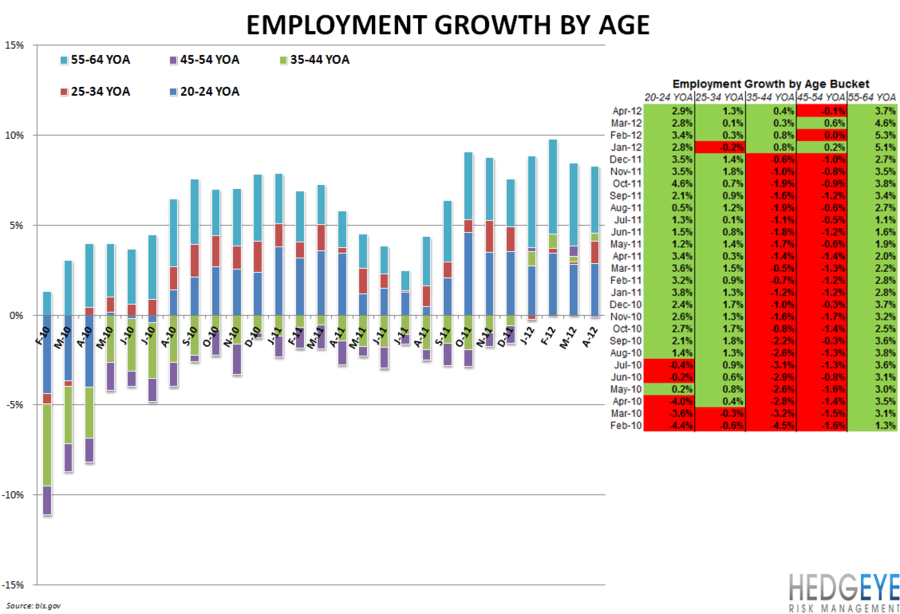

Employment by Age

As the chart below shows, all of the age cohorts we track on a monthly basis, with the exception of the 45-54YOA cohort, continued to gain jobs in April. Sequential slowdowns in the 45-54 and 55-64 YOA cohorts are not positive for casual dining. The continuing strength in youth employment trends is encouraging for QSR. Construction employment has not picked up and will not until there is a recovery in housing. Career Builder CEO Matthew Ferguson spoke on Bloomberg this morning on the jobs data and said that his company’s surveys are showing that 53% of companies say they’re going to higher more entry-level college graduates this year versus last year. That number was 40% a couple of years ago, according to Ferguson.

Hiring Trends Within the Restaurants Industry

Hiring trends within the restaurant industry remain strong as of the month of March (the full-service- and casual dining-specific data lags the broader data by one month). As the chart below illustrates, however, is that employment growth in the broader Leisure & Hospitality space has been rolling over as of the month of April. The Leisure and Hospitality data is released in line with the general employment data and gives us somewhat of an insight, at least directionally, into how hiring trends in the restaurant industry may look for April.

Consumer Confidence

The unemployment rate is obviously a statistic that has limited meaning for investors or analysts but consumer confidence is certainly impacted by headlines. As the chart below highlights, the declining Labor Force Participation Rate is helping to keep the headline Unemployment Rate print lower than it otherwise would be. Should the LFPR begin to rise, that would likely bring the headline Unemployment Rate higher absent a concurrent and substantial uptick in hiring.

Howard Penney

Managing Director

Rory Green

Analyst