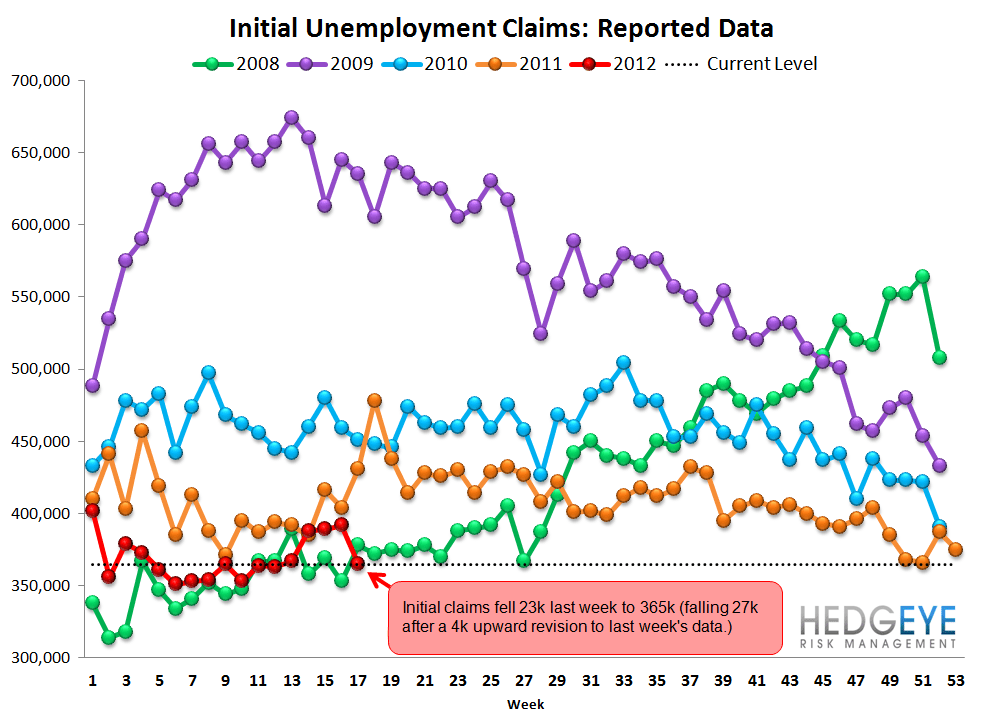

Jobless Claims Move Past 3 Weeks of Spring Break

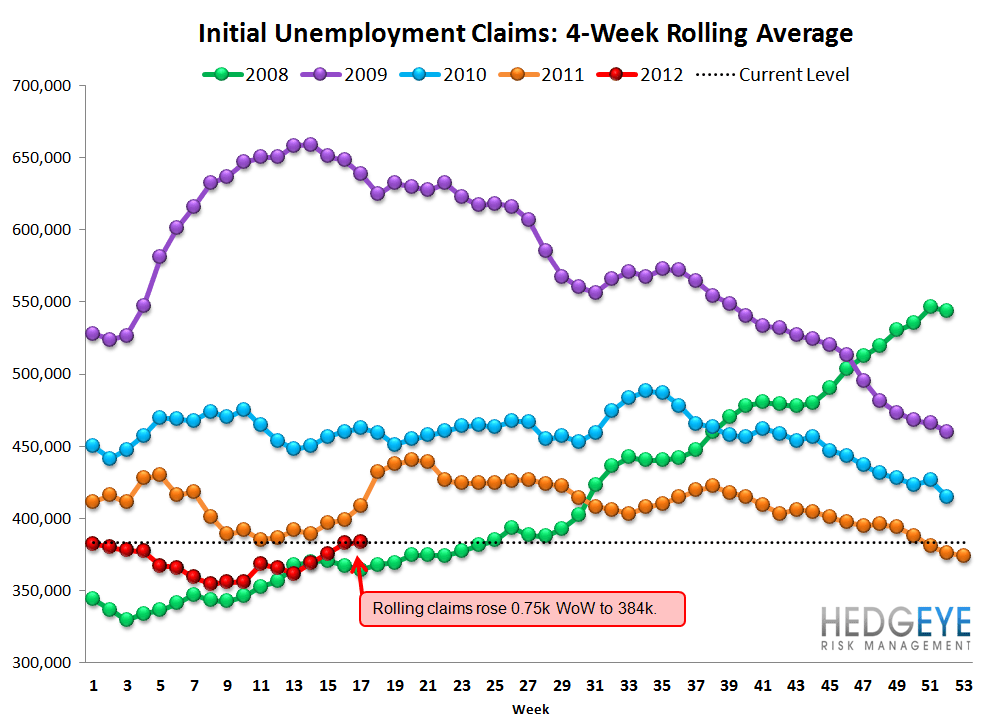

Initial claims fell 23k last week to 365k (falling 27k after a 4k upward revision to last week's data). Rolling claims rose by 0.8k WoW to 384k. On a non seasonally adjusted basis, claims fell 40k to 330k.

Over the last couple of weeks, we have noted that the claims numbers were coming in even worse than we would have expected based on our thesis regarding distortions in the seasonal adjustment factors. This week's sequential improvement puts claims back on track with where we would have expected them to be based on the seasonality dynamics. For more information here, please refer to our note titled "Predicting Initial Claims: The Sine Wave Model". We continue to expect claims to have an overall upward bias for the next 2-3 months.

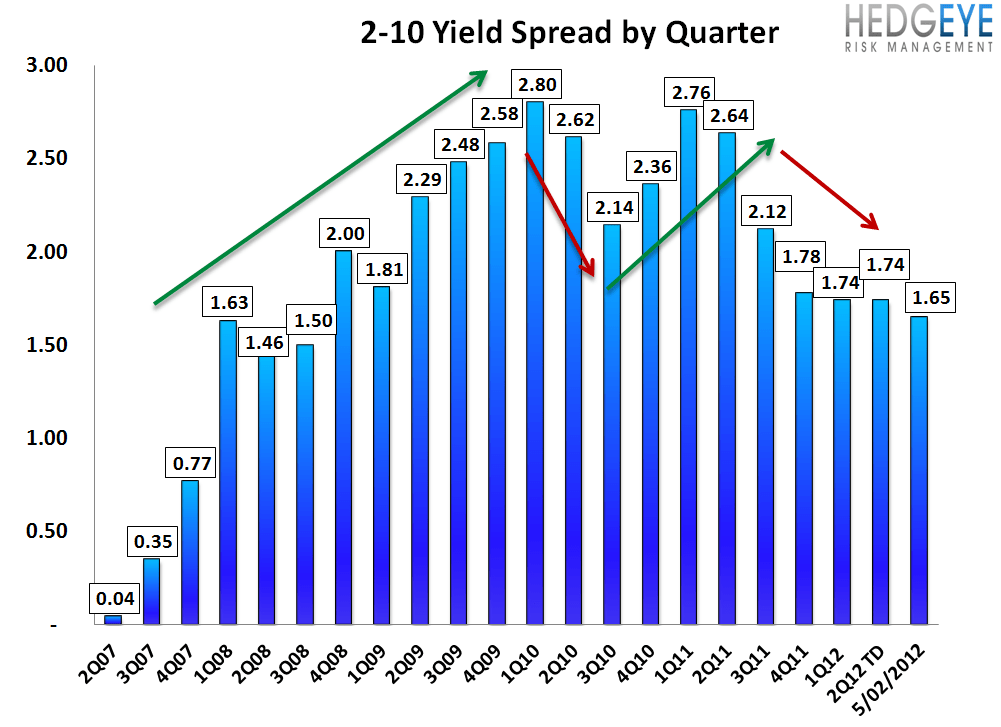

2-10 Spread

The 2-10 spread tightened 7 bps versus last week to 165 bps as of yesterday. The ten-year bond yield decreased 6 bps to 193 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky