Domino’s Pizza posted a soft quarter, missing on sales as we were expecting. From here, for now, we are neutral on the stock given the large correction on the news. DPZ missed EPS expectations of $0.49 by 2 cents. International comps also fell short while domestic comps were an unequivocal bomb versus the Street.

Our view of today’s print is that this was more a function of slowing pizza trends than any self-inflicted wounds from the company. That said, we believe that Pizza Hut’s dinner box and other promotional items from competitors may have taken share from Domino’s as the company’s promotions focused on non-pizza side items. In what seems to be a strategy to drive unit economics to a place where franchisees feel more of an incentive to help grow the unit count, management’s marketing strategy seems aimed at higher margin items likeac the Cheesy Bites (4Q) and Parmesan Bread Bites (1Q). The company said, “Our focus is on helping our franchisees generate strong store profits and to turn those profits into new stores so that our domestic store growth rate improves.”

Revenue

- Top line may have been impacted from marketing focus on side items. Pizza promotions better driver of traffic.

- Weather was not a significant factor.

- Technology continues to drive sales; 30% of orders were digital (versus a year ago) in the U.S. and 7% of total orders were made from a mobile device. The recently launched Android app accounted for 1% of orders in the quarter.

- International store growth remains strong and management offered encouraging commentary on weaker stores being “weeded out” of the system.

- 2% system comps (2.1% franchise, 1.6% company) for the domestic business was spun as being in the long term guidance range, which is it, but even bears were not anticipating such a weak comp.

Margin

- Promotion of the side item was effective in raising awareness of these items and driving margin higher.

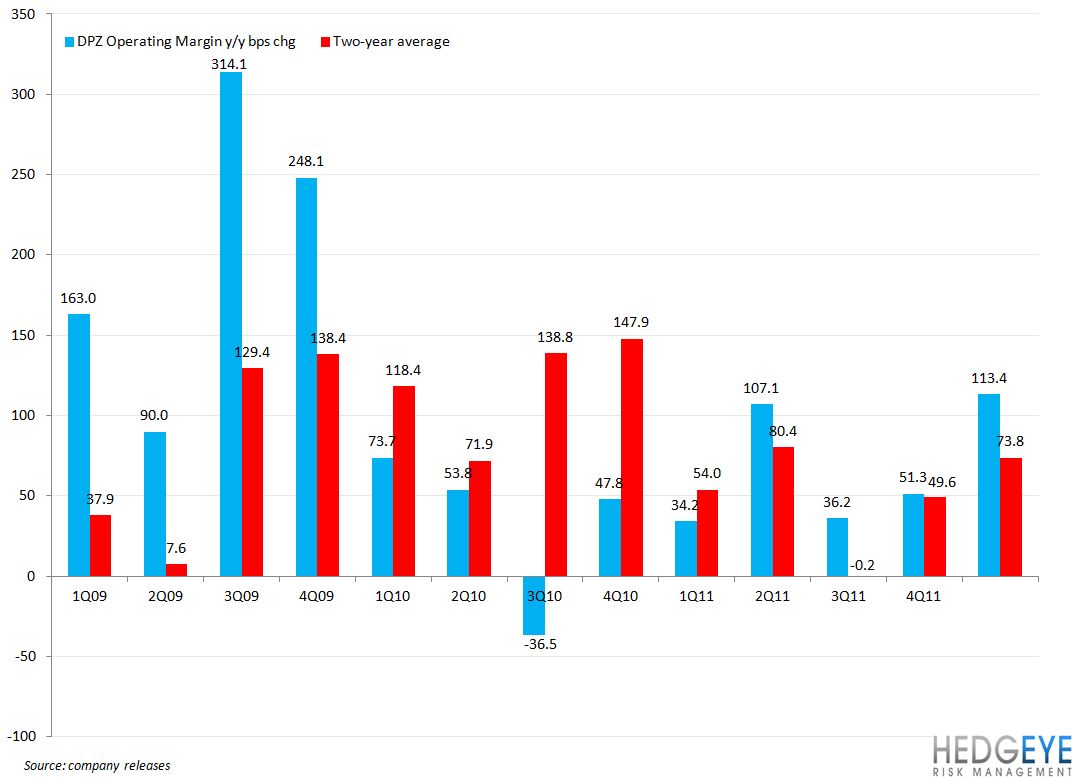

- Operating margin increased year-over-year from 28.7% to 29.8% as a result of a change in the mix of revenues attributable to fewer company-owned stores and increased franchise revenues. Franchised domestic same-store sales gained 2.1% while domestic comps were up 1.6%.

- Food costs: -140 bps as cheese block prices for 1Q were $1.52 versus $1.69 a year ago

- Labor costs: -110 bps

- Occupancy: -80 bps

- Insurance and Other: +40 bps

Outlook

- Store level unit growth is not expected to be a factor for the company in the near term. Over the medium term, raising store level profits is crucial to getting that drive back.

- Europe remains a concern with well-broadcast economic issues persisting. Management seems satisfied with how it is holding up but it is a potential worry.

- Stronger franchisees have been growing by buying stores that are not performing as well, or are even distressed, and as that trend eases there should continue to be fewer closures.

- Food basket inflation for the year is expected to be between 1-2% (unch).

- 35-40% of the company’s intended purchases for 2012 are locked in.

- The marketing message will be more evenly balanced between promoting check and traffic over the remainder of the year. Artisan pizza is a focus this quarter as well as early week carry out special and other side items.

- G&A is currently trending lower but the company expects higher G&A versus 2011 for the full year.

Other Points of Interest

- Technology has been a tremendous driver of business for Domino’s and will continue to be. However, in terms of the competitive advantage that it has offered the company versus competitors, we believe that that is waning rapidly as Papa John’s, Pizza Hut, and even smaller chains invest in their own digital ordering capabilities. Management described technology as the “biggest leveragable competitive advantage” both domestically and internationally.

- There are now more Domino’s stores outside the U.S. than within the U.S.

- Gas prices, for Domino’s, have the greatest impact on the company’s business through the effect on long term commodity prices.

- We expect sentiment around this name to turn marginally more bearish. A lot of the questions on the call seemed to lead management toward positive statements but management did not bite. According to Bloomberg there are currently no sell ratings for DPZ.

Howard Penney

Managing Director

Rory Green

Analyst