The Macau Metro Monitor, April 25, 2012

STEVE WYNN 'HOPEFUL' OF COTAI LAND GRANT NEXT WEEK Macau Business

Steve Wynn says he is “hopeful” that the company’s Cotai land grant could be in place by next week when he is in Macau. Wynn says he will be in Macau for a number of reasons, one being a meeting with the government.

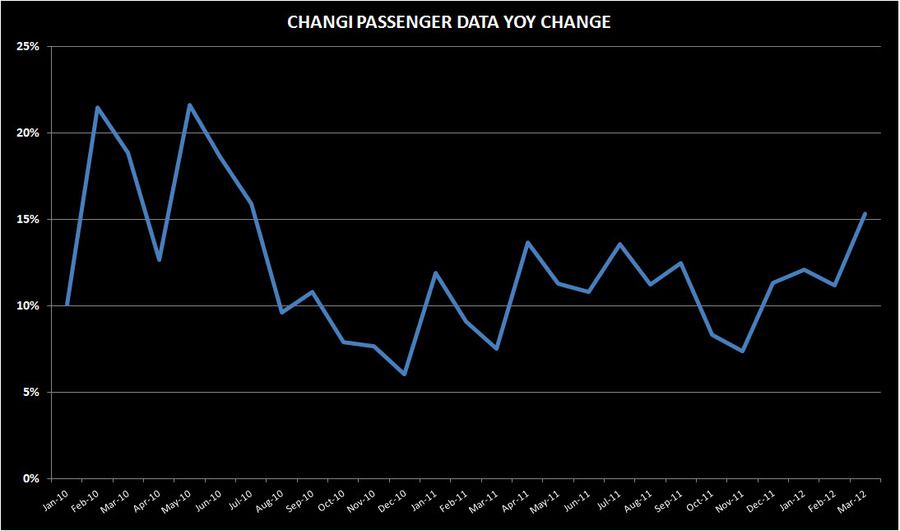

MONTHLY BREAKDOWN OF PASSENGER MOVEMENTS Changi Airport Group

Changi Airport passenger traffic grew 15.3% in March. For 1Q 2012, visitation grew 12.9% YoY.

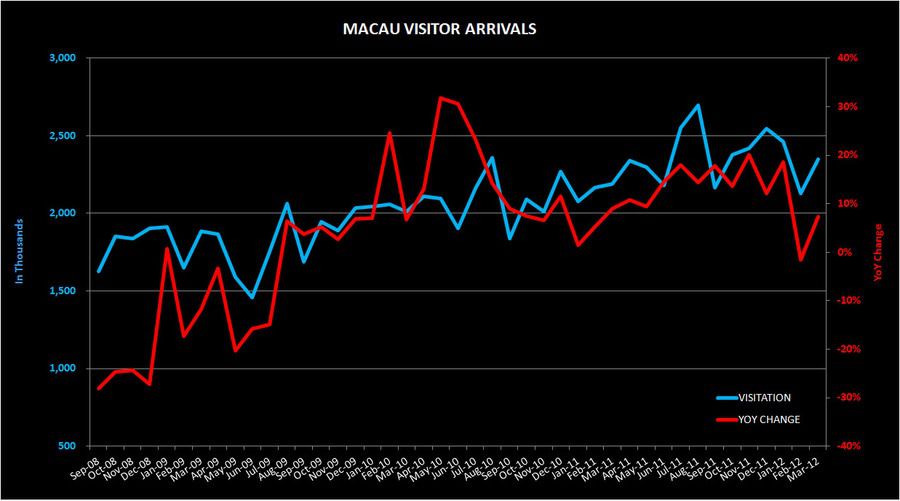

MARCH MACAU VISITOR ARRIVALS DSEC

Visitor arrivals totaled 2,349,703 in March 2012, up by 7.3% YoY. In the first quarter of 2012, visitor arrivals increased by 7.9% YoY to 6,942,320. The average length of stay of visitors decreased by 0.1 day YoY to 0.9 day. Visitors from Mainland China increased by 15.4% YoY to 1,447,564, with those traveling to Macau under the Individual Visit Scheme rising by 10.9% to 555,876.