Conclusion: While Obama has a clear edge in polls, indicators, and electoral college math, he has a less decisive edge in fundraising and is trailing his 2008 performance.

As we’ve been writing in recent political notes, the outlook for President Obama’s re-election odds currently look very positive based on a number of indicators. The first and foremost for us is likely our own proprietary indicator, the Hedgeye Election Index (HEI). The indicator currently has President Obama’s chances of re-election at just over 59.3%. The HEI is based on a number of real time economic indicators that correlate closely with Obama’s performance in conventional polls.

On InTrade, the world’s largest predictive market, the chance of Obama being re-elected is currently pegged at 60.4% and that figure has held steadily above 60% since March. This followed a relatively lengthy period of time in which, as can be seen in the chart below, President Obama’s chances of re-election were much closer to 50%. In fact, in September and October of 2011, the chances were solidly below 50%.

In traditional polls comparing Romney versus Obama, we see a similar trend. Specifically, if we look at the last ten major polls that compare Obama and Romney, Obama wins in 7 of 10, Romney wins in 2 of 10, and one poll is a tie. Based on the Real Clear Politics poll average, Obama currently has an advantage of +3.1 versus Romney.

As we drill down into the electoral vote math as driven by state-by-state polls, Obama’s situation also looks convincing. Most pundits, including us, agree that Obama would safely carry 14 states, mostly on the coasts, which would garner him 186 electoral votes. Meanwhile, it is likely that Romney safely carries 20 states in the South and West, which would garner him 156 electoral votes. Since the magic number of electoral votes needed is 270, this leaves many states still up for grabs.

In the scenario that Romney then won all of the states that Bush won in 2008, which includes Florida, Ohio, North Carolina, Virginia, Colorado, Indiana, Iowa, New Mexico, and Nevada, Romney would receive an additional 112 electoral college votes. Assuming that occurs, Romney’s total would then be 268 total Electoral College votes, which would obviously still be two short of the total needed for Romney to win the Presidency. As well, a lot would have to go right for Romney to win every single one of the aforementioned states.

So, as things stand today, an Obama re-election looks likely. There are two factors that we think may not be totally accounted for in today’s polls and indicators. The first is deterioration in the economy over the next couple of quarters, a factor that is becoming increasingly likely. The second is political fundraising, which has historically been a good leading indicator for electoral success.

In fact, political scientist Adam R. Brown published a paper titled, “Does Money Buy Votes? The Case of Self-Financed Gubernatorial Candidates, 1998 – 2008”, that looked at this the relationship between money and votes. His conclusion was:

“Because campaign spending correlates strongly with election results, observers of American politics frequently lament that money seems to buy votes. However, the apparent effect of spending on votes is severely inflated by omitted variable bias: The best candidates also happen to be the best fundraisers. Acting strategically, campaign donors direct their funds toward the “best” candidates, who would be more likely to win even in a moneyless world. These donor behaviors spuriously amplify the correlation between spending and votes. As evidence for this argument, I show that (non-strategic) self-financed spending has no statistical effect on election results, whereas (strategic) externally-financed spending does.”

If we take this a step further, it implies that in a Presidential election the money that is raised directly by the President, or his competitor, versus by his Party or a Super Pac, is strategic in nature and the most likely indicator of success. In this vein, Obama looks to be struggling.

Currently, President Obama has raised only $196 million as of the end of Q1 2012 for his re-election campaign. This is almost $40 million less than was raised by the same point in the 2008 election. Further, donations by specific industries are down dramatically from the last election. Most notably, donations from the investment industry are down -68% and donations from law firms are down -47%.

Not only are Obama’s fundraising efforts lagging, but it appears that Democrats in aggregate have been lagging Republicans. Certainly some of this has to do with the fact that the Republicans had a Presidential primary that attracted a large amount of donations, but the trends remain somewhat staggering versus 2008. The allocation of donations, so far at least, has shifted towards the Republicans in almost every major sector of the economy, even from unions. The chart below highlights these trends.

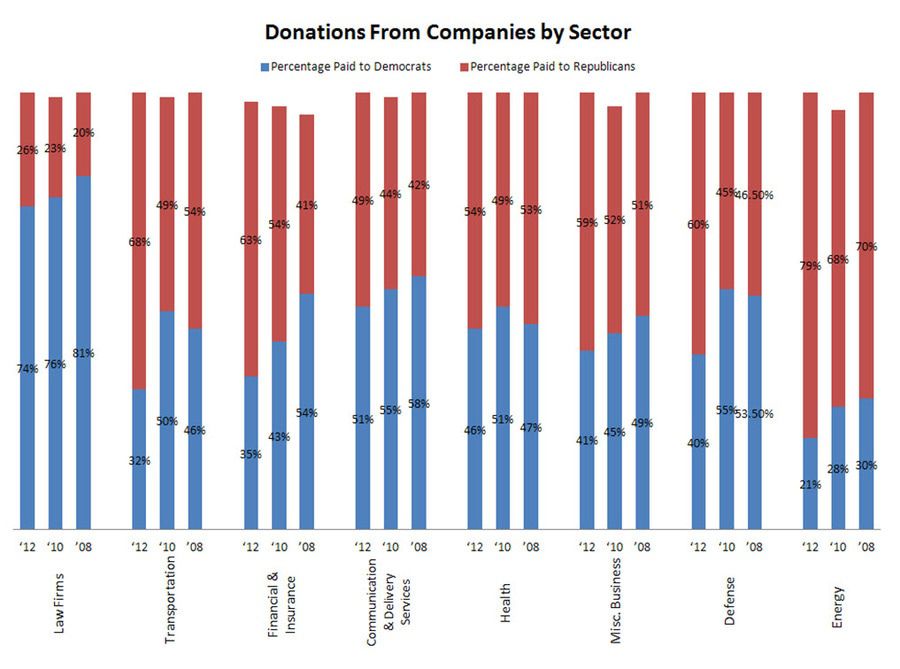

If we look at corporations exclusively, a very similar trend emerges. The chart below shows donations from major corporate sectors for 2008, 2010, and 2012. Once again, we see the trends shifting steadily towards the Republicans. (The reason some of these percentages do not add up to 100% is due to some money going to third parties and some being classified by the Center for Responsive Politics as “soft” money.)

The most staggering shift in donations is coming from, no surprise, the financial sector. As an example, in 2008, 75% of donations from Goldman Sachs went to Democrats. In 2012, only 21% of donations from Goldman Sachs went to Democrats. Now, to be fair, part of this is once again that the Republicans just had a competitive Presidential primary, but as the chart below highlights these trends also occurred in 2010.

The other key area where the Republicans are leading the Democrats in the cycle is in Super Pac funding. There are two Super PACs supporting Romney, American Crossroads and Restore Our Future, which have a combined $34 million on hand. Meanwhile, there is one Super PAC that is supporting President Obama, Priorities USA, which has $2.8 million on hand. Studies suggest Super PAC money is not as much of an indicator of electoral success as direct donations to the candidate, but, nonetheless, even here the Romney edge is meaningful.

In conclusion, while President Obama continues to look solid in many of the real time indicators we follow, the money appears to be flowing to the Republicans and Romney. In the arms race that is a Presidential campaign, money talks.

Daryl G. Jones

Director of Research