European Positions Update: Long German Bunds (BUNL); Covered France (EWQ) on 4/18

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.7% week-over-week vs -2.2% last week. Top performers: Switzerland +2.7%; Sweden +2.7%; Denmark +2.6%; Germany +2.5%; UK +2.1%; Russia (RTSI) +2.0%. Bottom performers: Cyprus -7.4%; Spain -2.9%; Luxembourg -1.3%; Poland -1.3%; Greece -1.3%.

- FX: The EUR/USD is up +1.03% week-over-week. W/W Divergences: GBP/EUR +0.72%, SEK/EUR +0.46%; RUB/EUR -0.46%, CZK/EUR -0.70%, TRY/EUR -0.71%.

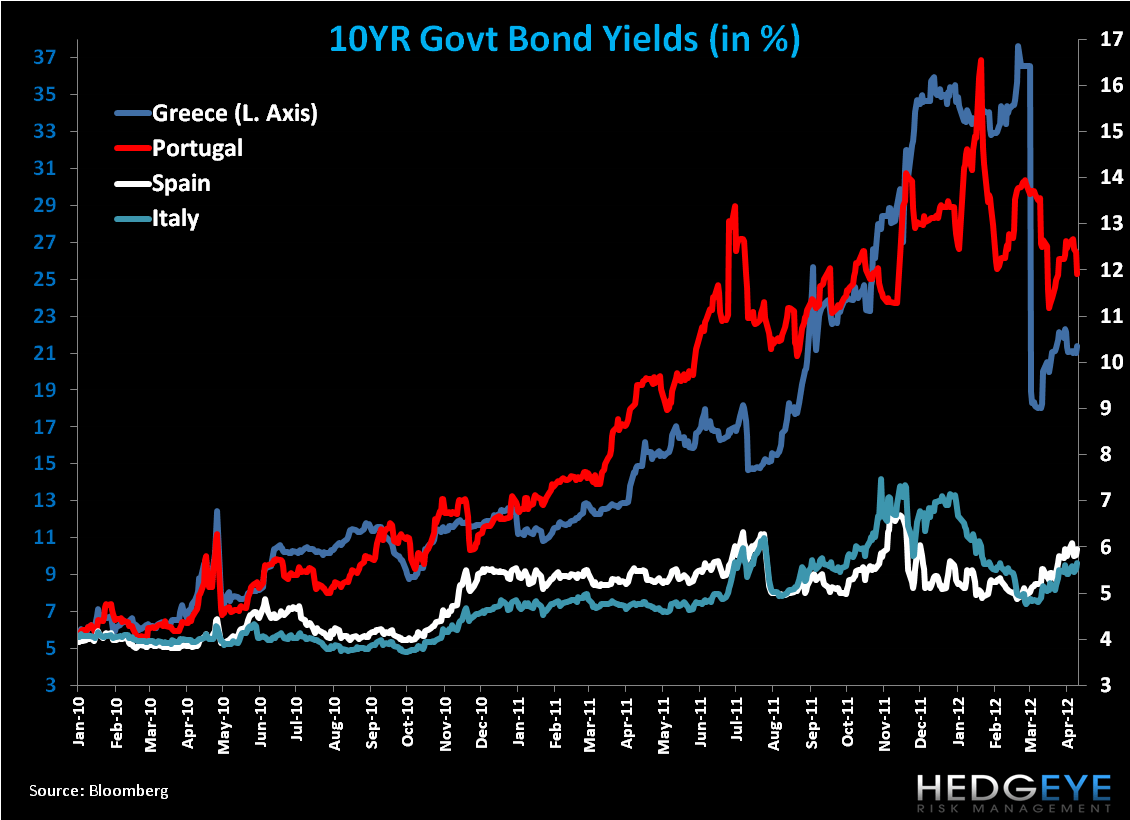

- Fixed Income: After a relatively flat week last week, Italian 10YR yields shot up +23bps to 5.65% week-over-week. This just trailed Greece's gain of 31bps to 21.37%. French yields also bounced ahead of the presidential election and talks of Fitch making a decision on its AAA credit status in May, via a +20bps rise to 3.10%. Portugal saw the only notable inflection to the downside, with yields falling -64bps to 11.91%.

In Review:

The title of this note could have also been “Europe: The Best of Times, The Worst of Times.” For yet another week, we saw substantial European capital market swings. As our Director of Research Daryl Jones succinctly said this week: One day bad news matters, the next day good news matters more.

In particular, this week saw significant equity swings around two Spanish bond auctions, short term paper on Tuesday and 2YR and 10YR maturities on Thursday, both of which met demand but saw higher average yields versus previous auctions. Both were digested favorably by the market, yet once again the PIIGS were laggards w/w on the score of equity performance and high sovereign yields. We continue to warn of the larger risks associated with Spain’s banking leverage to housing and property prices, in particular because we think Spanish house prices could fall another 30% from here. (For more, see our web portal at www.hedgeye.com for recent notes on the subject).

Further, we continue to signal that despite all the positives from such programs as the EFSF, ESM, LTRO, SMP, and increased funding to the IMF (see Call Outs below), programs designed to help firewall and provide liquidity to Europe’s fiscal and banking risks, they do little to bind Europe under a growth strategy. A positive growth profile is critical for investor confidence to buy equities, countries to pay down their debt and deficits through tax receipts, and more broadly for the market to clearly diagnose that Europe is out from under its dark cloud. In short, we think there’s more downside not priced in.

Switching gears, this Sunday marks the first of two French presidential election votes. While the leading two candidates, the incumbent Nicolas Sarkozy and Socialist Francois Hollande, will advance to the second round vote on May 6th, recent polls suggest Hollande will beat Sarkozy 29% to 24% in Round 1 and 58% to 42% in Round 2, according to CSA. Interestingly, Hollande may gain a significant share not on his merits alone, but due to Sarkophobia, or a repulsion of Sarkozy’s right-wing policy and social stance (which may sound nonsensical to an American audience) in a historically (post WWII) very left-leaning state.

That said, sociology professor Michel Maffesoli at Sorbonne University makes the case that despite the French media being very much against Sarkozy (nit-picking every social gaff and his lack of intelligence), Sarkozy has far more of a “rapport than is ever acknowledged”. He argues, "Post-modernity, which is the condition our societies are moving into, is far more anchored around the emotional than the rational or intellectual…and he is far more in phase with ordinary people than are the intellectuals who govern public life.” He adds, “in the voting-booth it is different. The booth is like a womb where people reconnect with the purely emotional. It means going with their gut rather than their brains…that's why I think Sarkozy can still do it."

Time will tell who captures the vote but what’s broadly clear is that both candidates plan to increase taxes and impose fees on financial transactions. Both have declared to reduce the country’s deficit to 0% (as a % of GDP), Hollande by 2017 and Sarkozy by 2016. Both guide to reduce the deficit to 3% by 2013 versus 5.3% in 2011. Taken together, we think these policy moves will disadvantage the broader economy versus its European peers.

Hollande specifically has signaled an even more socialist agenda, which we think should result in the inability of the state to meet its deficit and debt reduction targets. Hollande wants to increase spending by €20 MM over five years (by repealing €29 MM of tax breaks and generating revenue by separating retail and investment bank operations and raising the income tax on earners over €1 MM to 75%) and reduce the retirement age to 60 from 62. With the country’s debt rising to the 90% level, we expect growth to be compressed, as proven by the work of Reinhart and Rogoff. Finally, Hollande has stated that if elected he will renegotiate the EU budget compact and that he will not accept austerity as rule for countries and promised to increase France's minimum wage.

Taking a step back, the implications of a change of guard in France and recent statements by Sarkozy that the ECB should have “massively” bought Greek bonds at the outset to prevent the Eurozone debt crisis, may spell the end of Merkozy, namely Sarkozy’s strong working relationship with German Chancellor Merkel. Should France move further left and not find agreement with its German neighbor, the nation that we believe is carrying the big stick in Europe, it suggests the likelihood of further political instability, or at the very least a heightened improbability of attaining a united Eurocrat mind on the go-forward sovereign and banking policy decisions for Europe.

Call Outs:

Volkswagen: Europe’s largest carmaker, yesterday predicted a “very demanding” 2012 as the debt crisis threatens economic stability. European car sales dropped 6.6% to a 14-year low last month as deliveries in France and Italy tumbled by more than 20%.

IMF: Japan promises to provide $60B; Denmark, Norway, and Sweden added $26B; Poland lent $8B; and Switzerland pledged a "substantial amount" this week. The IMF continues to haggle over funding and influence from member counties in a Spring Meeting spilling into this weekend. China and Brazil indicated that they are not ready to set a figure on IMF contributions and Reuters suggests they want to be assured they will play a bigger role before chipping in.

John Paulson: the billionaire hedge fund manager who has said the euro may eventually unravel, told investors he is shorting European sovereign bonds, according to a person familiar with the matter.

Outgoing World Bank President Zoellick Suggests in FT Op-ed: “Instead of quarrelling over firewalls, Europeans should add just a fraction – say €10B – to the capital of the European Investment Bank. Under current conditions, the EIB may actually have to reduce lending. Instead, the EIB could use more capital to borrow and then invest to support structural reforms, showing Spaniards and Italians that their sacrifices will draw productive investments.”

France: Fitch rumored to not make decision on downgrading France’s sovereign credit rating until after French elections (May 6th).

Holland: Fitch official says may cut Dutch AAA rating if the Netherlands does not cut the deficit.

Sweden: cuts growth forecasts to +0.4% in 2012 (vs a prior estimate of +1.3%) and +3.3% in 2013 (vs +3.5%).

CDS Risk Monitor:

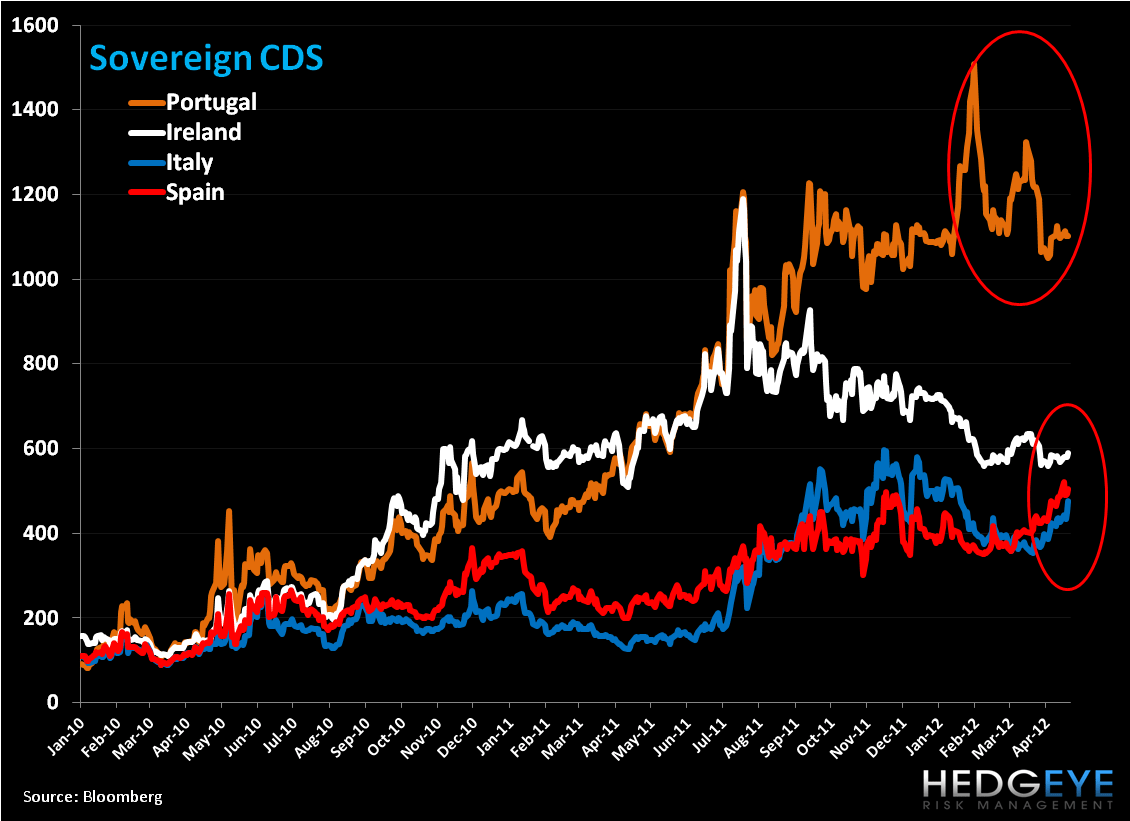

Week-over-week CDS was up across the main countries we track. Italy saw the largest gains in CDS w/w, +50bps to 476bps, followed by Ireland +21bps to 590bps; France +18bps to 199bps; Spain +17bps to 504bps; Germany +13bps to 84bps; Portugal +4bps to 1102bps; and the US +1bp to 30bps. The UK fell -1bp to 63bps.

Data Dump:

Eurozone ZEW Economic Sentiment 13.1 APR vs 11 MAR

Eurozone Current Account -5.9B EUR FEB vs -10.1B EUR JAN

Eurozone Construction Output -12.9% FEB Y/Y vs -2.7% JAN [-7.1% FEB M/M vs -0.5% JAN]

EU 25 NEW Car Registrations -7% MAR Y/Y vs -9.7% FEB

Eurozone CPI 2.7% MAR Y/Y (exp. 2.6%)

Eurozone Trade Balance 3.7B EUR FEB (exp. 5B EUR) vs 5.3B EUR

Germany ZEW Current Situation 40.7 APR (exp. 35) vs 37.6 MAR

Germany ZEW Economic Sentiment 23.4 APR (exp. 19) vs 22.3 MAR

Germany IFO Business Climate 109.9 APR (exp. 109.5) vs 109.8 MAR

Germany IFO Current Assessment 117.5 APR (exp. 117) vs 117.4 MAR

Germany IFO Expectations 102.7 APR (exp. 102.3) vs 102.7 MAR

Germany Producer Prices 3.3% MAR Y/Y (exp. 3.1%) vs 3.2% FEB [0.6% MAR M/M (exp. 0.4%) vs 0.4% FEB]

UK CPI 3.5% MAR Y/Y (exp. 3.4%) vs 3.4% FEB [0.3% MAR M/M vs 0.6% FEB]

UK RPI 3.6% MAR Y/Y (exp. 3.6%) vs 3.7% FEB [0.4% MAR M/M vs 0.8% FEB]

UK Retail Sale w/ Auto Fuel 3.3% MAR Y/Y (exp. 1.5%) vs 1% FEB [1.8% MAR M/M (exp. 0.5%) vs -0.8% ]

UK ILO Unemployment Rate 8.3% FEB vs 8.4% JAN

UK Jobless Claims Chg 3.6K MAR vs 4.5K FEB

Spain House Price Index -7.2% in Q1 Y/Y vs -6.8% in Q4 [-3.0% in Q1 Q/Q vs -1.8% in Q4]

Italy Industrial Orders -13.2% FEB Y/Y (exp. -6.2%) vs -5.6% JAN [-2.5% FEB M/M (exp. -1.1%) vs -7.7% JAN]

Italy Industrial Sales -1.5% FEB Y/Y vs -4.4% JAN [2.3% FEB M/M vs -4.9% JAN]

Switzerland Credit Suisse ZEW economic expectations 2.1 APR vs 0.0 MAR

Switzerland Producer and Import Prices -2% MAR Y/Y (exp. -1.8%) vs -1.9% FEB [0.3% MAR M/M (exp. 0.5%) vs 0.8% FEB]

Netherlands Unemployment Rate 5.9% MAR vs 5.9% FEB

Portugal Producer Prices 3.5% MAR Y/Y vs 4.2% FEB

Bulgaria Unemployment Rate 11.5% MAR vs 11.5% FEB

Slovakia Unemployment Rate 13.7% MAR vs 13.8% FEB

Hungary Avg Gross Wages 6.9% FEB Y/Y vs 4.3% JAN

Slovenia Unemployment Rate 12.4% FEB vs 12.5% JAN

Czech Republic Export Price Index 4.2% FEB Y/Y vs 5.4% JAN

Czech Republic Import Price Index 5.8% FEB Y/Y vs 7.0% JAN

Turkey Consumer Confidence 93.9 MAR vs 93.2 FEB

Turkey Unemployment Rate 10.2% JAN vs 9.8% DEC

Interest Rate Decisions:

(4/18) Sweden Riksbank Interest Rate UNCH at 1.50% (as expected).

(4/18) Bank of England Minutes from 4/5 session: votes 9-0 votes for no rate hike and 8-1 for No Asset Purchase increase.

The European Week Ahead

Sunday: First round of the French Presidential Election

Monday: Apr. Eurozone PMI Composite, Manufacturing, and Services - Advance; 2011 Eurozone Eurostat Govt Debt as a % of GDP; Apr. Germany PMI Manufacturing and Services – Advance; Mar. UK Consumer Confidence Index (Apr 23-27); Apr. France PMI Manufacturing and Services – Preliminary, Production Outlook Indicator, Business Confidence Indicator, and Own-Company Production Outlook; Apr. Italy Consumer Confidence Indicator

Tuesday: Eurozone Eurostat Discontinues the Release of Industrial Orders; Mar. Germany Import Price Index (Apr 24-30); Mar. UK Public Finances and Public Sector Net Borrowing; Apr. France Consumer Confidence Indicator and Business Survey Overall Demand; Mar. Spain Budget Balance YtD; Feb. Spain Mortgages-capital Loaned and Mortgages on Houses; Mar. Italy Hourly Wages

Wednesday: 1Q UK GDP - Advance; Apr. UK CBI Trends Total Orders, Trends Selling Prices, and Business Optimism; Feb. UK Index Services; Mar. Spain Producer Prices

Thursday: Apr. Eurozone Consumer Confidence – Final, Business Climate Indicator; Economic, Industrial, and Services Confidence; Apr. Germany CPI; Apr. UK GfK Consumer Confidence Survey, Nationwide House Prices, and CBI Reported Sales; Mar. UK BBA Loans for House Purchase; Mar. France Jobseekers; Apr. Italy Business Confidence

Friday: May Germany GfK Consumer Confidence Survey; Mar. France Producer Prices and Consumer Spending; 1Q Spain Unemployment Rate; Apr. Spain Consumer Price Index - Preliminary; Mar. Spain Retail Sales; Feb. Italy Retail Sales

Extended Calendar Call-Outs:

22 April: French Elections (Round 1).

6 May: Round 2 (Final) French Presidential Elections. Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst