The most important meal of the day.

THE HEDGEYE BREAKFAST MONITOR

HEDGEYE VIRTUAL PORTFOLIO POSITIONS

LONGS: JACK, SBUX

SHORTS: DNKN, MCD

Comments: Keith booked a gain in BWLD on Friday in the Hedgeye Virtual Portfolio. His quantitative model was indicating that the stock was oversold on an immediate-term TRADE duration. Our bearish fundamental view remains unchanged.

MACRO NOTES

Commentary from CEO Keith McCullough

Bulls were looking for a Monday morning bounce – not happening; inflows are dead:

- EUROPE – the DAX is testing an intermediate-term TREND line breakdown of the 6614, so I’ll be watching that line closely as a barometer for what the correction in US stocks could look like (Germany’s jobs and fiscal situation is stronger than in the US); Spain and Italy look awful; we re-shorted France on Thursday as we think mean reversion there is to the downside

- COMMODITIES – getting blasted ever since the US Dollar stopped going down (2wks ago); got interconnectedness? We call this Deflating The Inflation, or unwinding Bernanke’s Bubbles (commodity bubble – see our slide deck). Gold and Copper down hard this morning after failing at $1675 and $3.73 levels of support last wk – both are in Bearish Formations (bearish on all 3 of our risk mgt durations)

- BOND YIELDS – 10yr UST yields snapping my intermediate-terrm TREND line of 2.03% last wk is very bullish for Treasuries until it isn’t. This happened in conjunction with a spike in weekly jobless claims (380,000) = Growth Slowing.

SP500’s immediate-term risk mgt range = 1.

KM

SUBSECTOR PERFORMANCE

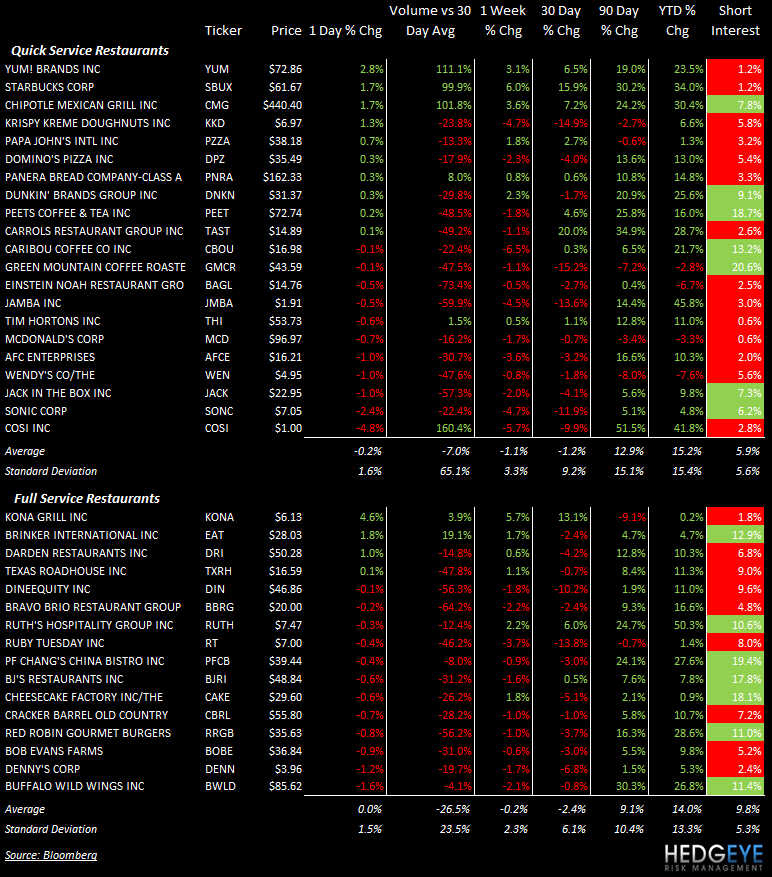

QUICK SERVICE

CMG: Chipotle was awarded the 2012 GRANDY Award by Creative Artists Agency for its animated short film “Back to the Start”. “‘Back to the Start’ was never intended to be an ad; it was meant to be a short film to invite people on a journey with us to a more sustainable future,” said Mark Crumpacker, CMO at Chipotle.

DPZ: Domino’s was raised to “Buy” from “Hold” at Miller Tabak & Co. The 12-month price target is $41 per share, or 15.5% higher than Friday’s close.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

YUM: Yum gained on accelerating volume on Friday. Bulls are buying on the expectation that the US business has improved in 2012.

SBUX: Starbucks also gained on accelerating volume to close the week.

COSI: Cosi declined -4.8% on accelerating volume.

CASUAL DINING

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

EAT: Brinker traded higher on strong volume. The company is our second-favorite casual dining name but we have advised taking a cautious stance on the name given its outsized returns during the last six months and its vulnerability in the context of a slowdown in industry sales. BWLD is our favorite name on the short side in casual dining, along with CBRL, TXRH, and CAKE on strength.

Howard Penney

Managing Director

Rory Green

Analyst