Conclusion: Another leg down in Spanish home prices seems likely and this could potentially be the event that leads to an acceleration of stress in Spanish sovereign yields.

The focus of the sovereign debt crisis in Europe has been, rightfully so, on Greece and the potential derivative effects of a Greek default. This despite the fact that Greece’s economy, based on the CIA’s 2011 Fact Book estimates, is only $312 billion, or less than 2% of the European Union in aggregate. With an estimated 2011 GDP of $1.5 billion, Spain has the 12th largest economy in the world and an economy that is almost 5x the size of Greece’s GDP.

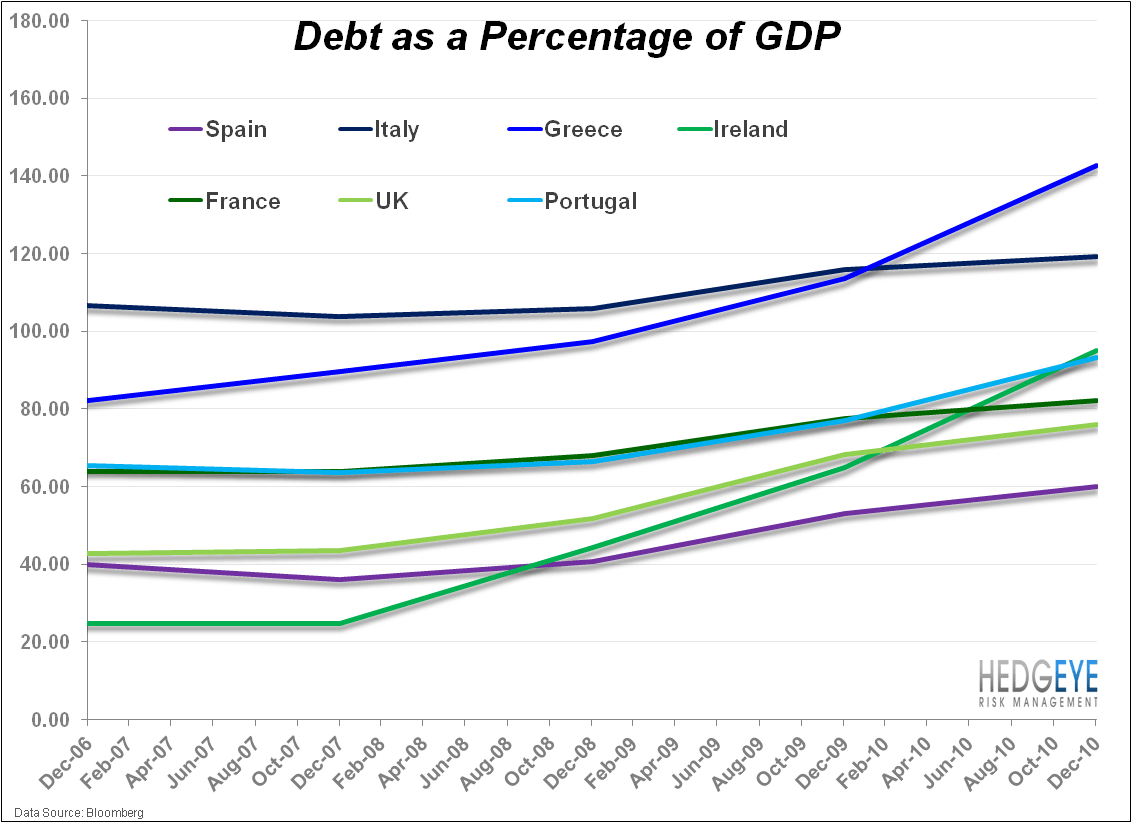

As the chart below of debt-as-percentage-of-GDP shows, Spain, so far, has been able to manage its balance sheet somewhat better than many of its neighbors with a debt-to-GDP of roughly 68.5% as of the end of 2011. (Incidentally, many believe that when incorporating regional debts, Spain is closer to 90%, currently.) Based on Spanish government estimates, this ratio will jump to 79.8% at the end of 2012. While still below the Eurozone average of 90.4%, this is the highest acceleration in the Eurozone. This last fact is at least partially reflected in the credit default swap market with Spain’s 5-year CDS accelerating in price in the year-to-date.

Spain’s most significant headwind going forward is, simply put, growth. Over the last two fiscal years of 2010 and 2011 combined, the lowest average growth rates in the European Union were the following countries in order:

- Greece at an average annual growth rate of -5.2%;

- Iceland at an average annual growth rate of -0.45%;

- Portugal at an average annual growth rate of -0.1%;

- Ireland at an average annual growth rate of +0.08%; and

- Spain at an average annual growth rate of +0.15%.

Clearly, this is not an enviable group of countries and Spain is the only one amongst them that hasn’t had a complete sovereign debt meltdown.

As any sovereign credit analyst will tell you, the easiest way to resolve a sovereign debt issue is to grow out of it. Spain’s economic growth outlook is constrained by two separate, though related, factors: employment and housing.

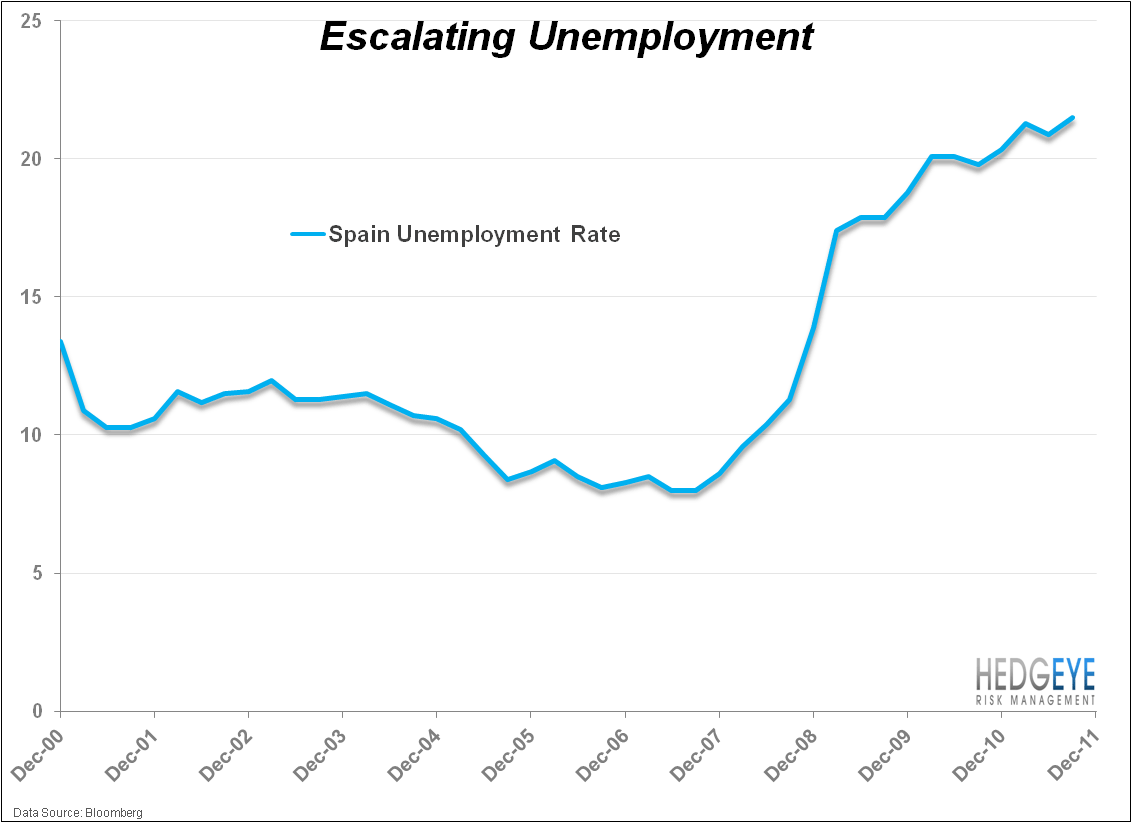

In the chart below, we’ve highlighted Spanish unemployment going back to 2000. The unemployment rate of Spain hit 23.6% in February for the 8th consecutive monthly increase, which is both the highest rate since 2000, but also literally the highest unemployment rate since World War II. As if that weren’t enough, the government expects the unemployment rate, already the highest in the industrialized world, to increase to north of 24% this year. The current number of unemployed in Spain is equivalent to 4.75 million, which is the highest number since the Spaniards began keeping the data in 1996.

The counter view to this abnormally high unemployment rate in Spain is that there is a large and thriving underground economy, which means that government reported employment figures are understated. Certainly, there is likely credence to this, but, even so, most estimates suggest accounting for the underground employment would only reduce the overall unemployment rate by 400 basis points. In the shorter term, there is also the employment head wind of a recently implemented labor reform law in February that will make it easier for employers to unilaterally lay employees off and cut salaries. Eventually, though, this is expected to make the Spanish employment market more fluid as it will likely make employers more willing to take on the risk of hiring.

The chart below highlights the structural employment issue in Spain versus the remainder of the Eurozone. Specifically, it emphasizes the year-over-year change in unemployment by country. In 2011, Greece was the only nation that saw unemployment increase at a quicker pace than Spain.

A key reason that Spanish unemployment rates have ballooned versus the rest of the Eurozone is because Spain had a vastly more inflated housing and construction sector during the boom years. In fact, according to Eurostat, Spain employed 2.9 million people in construction industries at, or near, the peak in 2007. In total, this was about 1/5th of all construction workers in the EU-27 despite the fact that Spain has less than 10% of the total population. Clearly, an improvement in Spanish employment will be predicated on a recovery in the construction sector.

Unfortunately, a recovery in Spanish housing and construction markets appears to be a long way in the coming. Unlike most industrial nations that experienced extended housing price inflation in the late 1990s and mid-2000s, Spain actually had two bubble periods with the first beginning in 1985. As the chart below highlights, from 1985 – 1991 home prices basically tripled, from 1992 – 1996 they basically remained flat, and from 1996 – 2008 prices more than doubled. So far, from the peak, Spanish home prices are in aggregate only off about 20%.

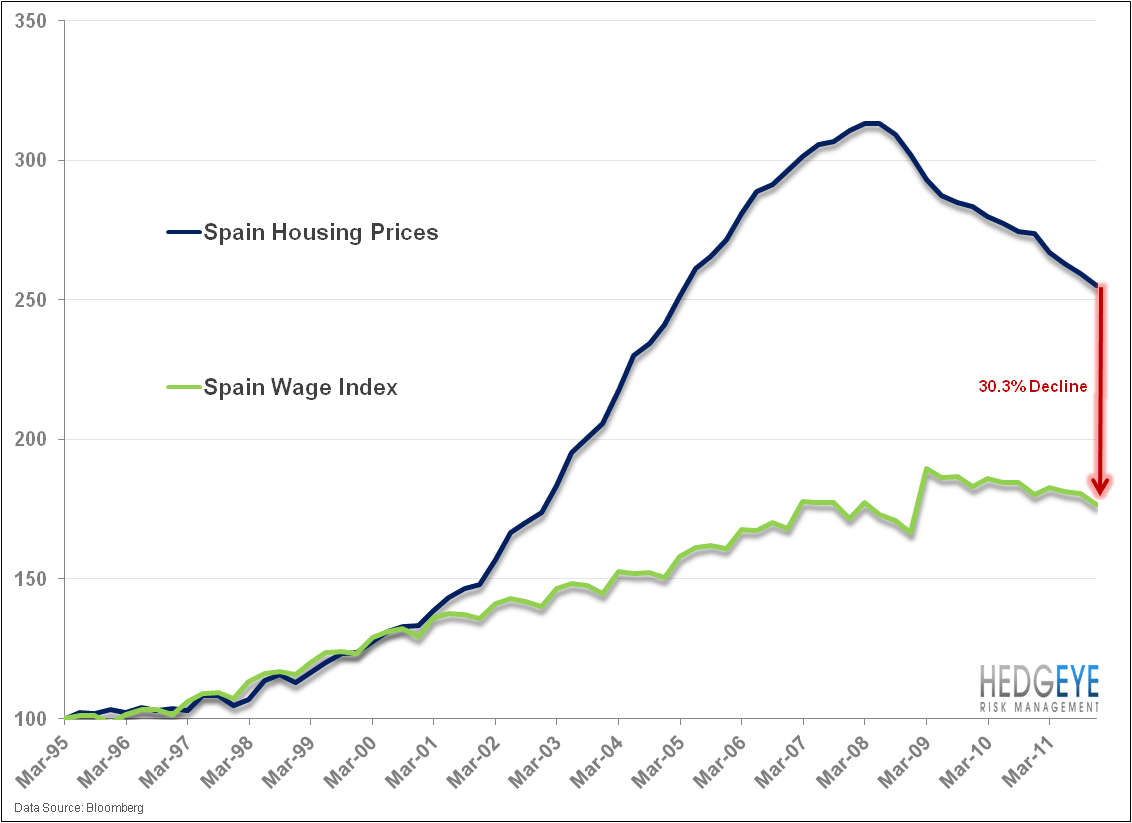

There are two potential proxies for how much further home prices in Spain may have to fall. The first is wage growth, which has historically tracked housing prices. Intuitively, this makes sense. The more consumers have in their pockets generally, the more they have to spend on housing (all else being equal). As the chart below shows, wages and home prices tracked each other steadily until 2000, at which point home prices began to accelerate beyond wage growth. Currently, home prices would need to decline just over 30% to revert back to wage growth.

The second proxy for further correction in Spanish home prices is the path of U.S. home prices. Based on the Case-Shiller 20-city seasonally adjusted series, U.S. home prices have already corrected 34% peak-to-trough. Comparing Spain to the U.S. is not quite apples-to-apples as home prices were driven much higher due to ownership rates that eclipsed 80% at the peak in Spain. So, depending on the data set we use, from the start of the second leg of the Spanish home price bubble in 2000 compared to the U.S., Spanish home prices have a potential downside of more than 35% from current levels.

The risk to the downside in Spanish home prices is being clearly reflected in real estate transactions in Spain. The chart below highlights year-over-year real estate transactions by month. In the most recent month of February 2012, transactions were down more than -30% from the prior year. Without a sustainable pick up in the real estate market, it will be impossible for employment to improve meaningfully.

The second derivatives of continued decline in real estate prices in Spain are both economic growth and the health of the banking system. On the first point, the Bank of Spain estimates that a decline in home prices of one dollar will decrease consumption by $0.03. Thus, a 15% decline in housing should reduce GDP by almost 2% over the next two years. (Hat tip to Carmel Asset Management for highlighting this analysis in the WSJ.) This would obviously have a direct impact on Spanish banks.

Currently, the Spanish banking system is estimated to have a 1.8 trillion euro loan book. It is estimated that roughly 20% of that is in real estate assets, of which almost half are considered troubled. Obviously both declining real estate prices and slowing economic growth generally put increased pressure on the portion of the loan book which is currently not troubled, and equates to almost 150% of Spanish GDP.

Certainly Greece has been the rightful focus of the sovereign debt issues in Europe, but the likelihood of another serious leg down in Spanish home price could put Spain front and center in 2012.

Daryl G. Jones

Director of Research