THE HEDGEYE BREAKFAST MONITOR

HEDGEYE VIRTUAL PORTFOLIO POSITIONS

LONGS: EAT, JACK, SBUX

SHORTS: BWLD, DNKN, MCD

MACRO NOTES

Commentary from CEO Keith McCullough

Most Read (Bloomberg headline): “SP500 Caps Longest Drop Since November” – blame Europe? C’mon:

- JAPAN – what goes up on no fundamentals comes down hard – Japanese Equities down for 8 consecutive days for a -8% cumulative correction – and unless your major country index has AAPL in it, that’s pretty much the range of corrections across the world in the last 6 weeks = -7-9% (Hong Kong, Germany, Russia, Brazil, Russell2000, etc).

- VOLATILITY – so you’re saying it’s the 1990’s, eh? Right, right. Since the Russell2000 and the CRB Index topped on the same day (March 26th), the US Equity VIX is up +43% in a straight line. Buying anything equities/commodities/big beta at 14-15 VIX has not worked since 2008.

- TREASURIES – 10yr bond yield snapping my intermediate-term TREND line of 2.03% support this morning and the Yield Spread continues to compress (down 24bps in 3 wks). This is what we call Growth Slowing being priced into Equities, Commodities, and Bonds. You should have taken that Credit Suisse call to “buy stocks b/c bond yields are rising” and done the opposite.

On a net basis, I got longer on red yesterday (14 LONGS, 10 SHORTS). The SP500 should bounce today, but if it can’t close > 1391, we sell again on green and tighten that net exposure back up.

KM

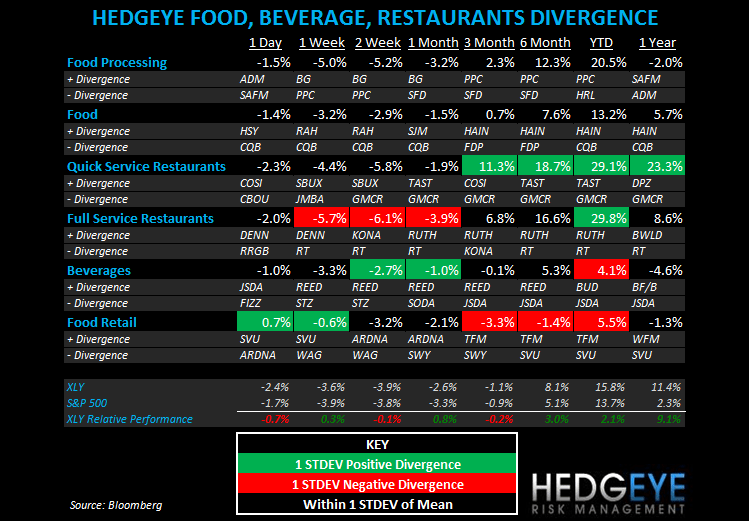

SUBSECTOR PERFORMANCE

QUICK SERVICE

PNRA: Panera Bread has appointed Thomas Patrick Kelly Interim CFO. The company said that it expects the ongoing search for a permanent CFO to take four-to-six months to complete.

MCD: McDonald’s is set to franchise in Russia for the first time under a new deal with Rosinter, the country’s largest restaurant holding company. The company still plans to open 40 to 45 company-owned restaurants per year in the country but the Rosinter deal allows the company to expand its presence to non-traditional locations like airports and train stations. There are currently ~300 MCD restaurants in Russia.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

GMCR: Green Mountain Coffee Roasters declined on accelerating volume along with CBOU and JMBA.

CASUAL DINING

RT: Ruby Tuesday closed the deal to acquire Lime Fresh Mexican Grill for $24 million.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

RT: Ruby Tuesday underperformed again yesterday.

RRGB: Red Robin Gourmet Burger declined 3.3% on accelerating volume yesterday.

Howard Penney

Managing Director

Rory Green

Analyst