Keith covered our GLD short position in the Hedgeye Virtual Portfolio this morning at $157.86 on the etf for a 3.28% gain, as gold finally became immediate-term TRADE oversold.

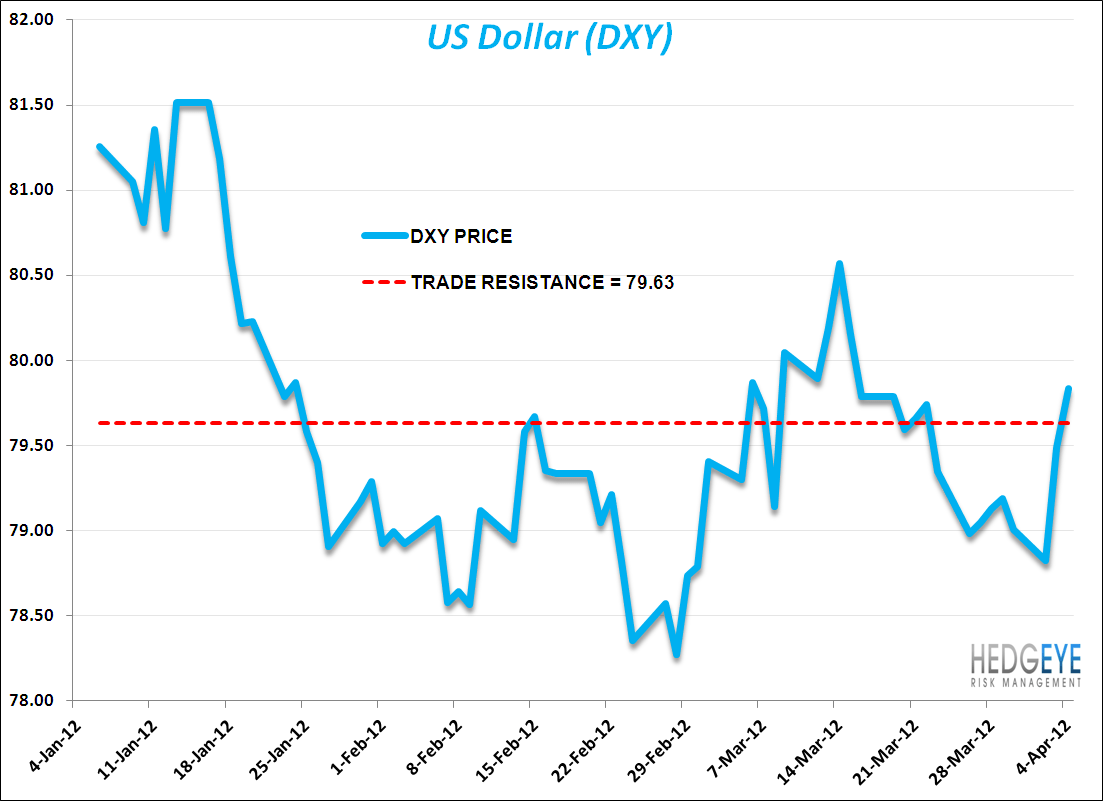

The inverse correlation between gold and the USD remains strong at -0.62 over the past 15 days and -0.75 over the past 90 days. Along with covering our short in gold, we sold our long position in the USD etf UUP at $22.12 this morning.

Fundamentally, we think that gold remains under pressure as QE3 is unlikely. The FOMC Minutes from the March 13th meeting released yesterday showed no immediate indication of further quantitative easing. The release stated that,

“Members viewed the information on U.S. economic activity received over the intermeeting period as suggesting that the economy had been expanding moderately and generally agreed that the economic outlook, while a bit stronger overall, was broadly similar to that at the time of their January meeting…In their discussion of monetary policy for the period ahead, members agreed that it would be appropriate to maintain the existing highly accommodative stance of monetary policy. In particular, they agreed to keep the target range for the federal funds rate at 0 to ¼ percent, to continue the program of extending the average maturity of the Federal Reserve’s holdings of securities as announced in September, and to retain the existing policies regarding the reinvestment of principal payments from Federal Reserve holdings of securities.”

The lack of incremental easing is a headwind for treasuries, which in turn is a headwind for gold, as gold competes with real yields.

The chart below highlights this relationship.

Kevin Kaiser

Analyst