Despite strong airport and taxi traffic, it’s all gonna come down to the Big B.

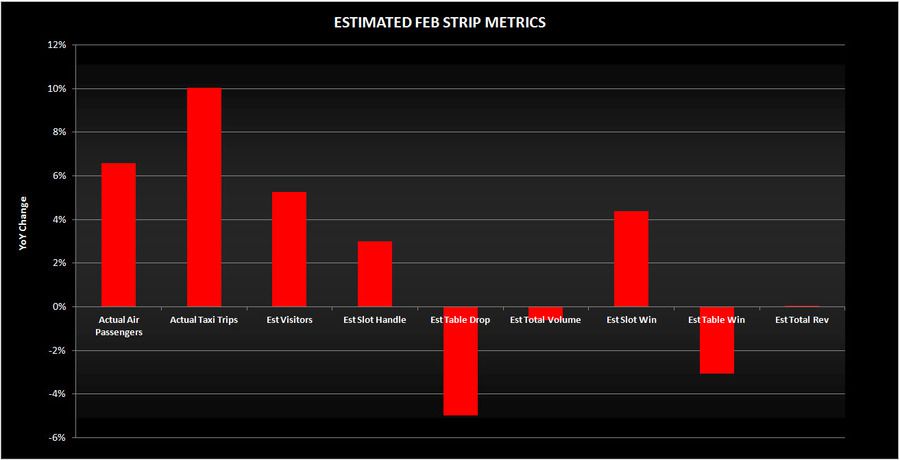

With McCarran Airport traffic increasing 6.6% and taxi trips up 10.0% YoY, one would expect blowout gaming revenues for February. Leap year probably contributed 3-4% of the surge in traffic. However, with Chinese New Year falling in January of this year and February of last year, the comparison is very difficult. Remember that with a favorable comparison, the Strip experienced a 163% YoY increase in Baccarat drop in January 2012.

Assuming normal hold – a big assumption – we think baccarat volume needs to be down 20% for gaming revenues to be flat. Anything worse would result in negative gaming revenue growth. The problem is that at down 20%, combined January and February baccarat drop would total $2.5 billion, approximately 25% higher than 2010’s record. We consider this unlikely. It looks like the Strip will need above average hold for revenues to show growth in February.

February could be a disappointment to the MGM and CZR bulls. Here are our projections: