TODAY’S S&P 500 SET-UP – March 28, 2012

As we look at today’s set up for the S&P 500, the range is 14 points or -0.60% downside to 1404 and 0.39% upside to 1418.

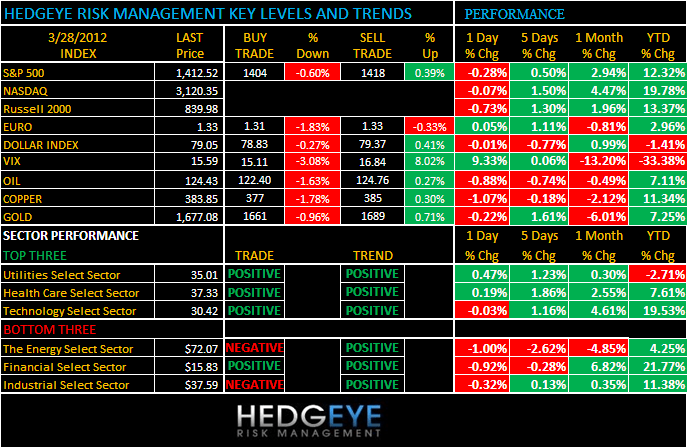

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

SENTIMENT – literally ever metric we track is bombing out the bears; hedge fund short interest hitting new lows, VIX 14, and now my Spread in the II Bull/Bear survey hits its widest to the bullish side since Q1 of last year at +2900 basis points wide! With only 22.6% admitting to be bearish (new low), we’re happy to go Lone Wolf.

- ADVANCE/DECLINE LINE: -507 (-2073)

- VOLUME: NYSE 730.24 (-3.27%)

- VIX: 15.59 9.33% YTD PERFORMANCE: -33.38%

- SPX PUT/CALL RATIO: 2.25 from 1.72 (30.81%)

CREDIT/ECONOMIC MARKET LOOK:

BOND YIELDS – the one bull case we could actually buy into is Strong Dollar + Rising Treasury Yields (at the same time); that would mean #GrowthSlowing is off the table. Not now, not at $106 oil. The US Dollar Index is down for the 3rd consecutive week thanks to daily talk show appearances from the Bernank and the 10yr failed, hard, at long-term TAIL resistance of 2.47%.

- TED SPREAD: 38.94

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.21 from 2.18

- YIELD CURVE: 1.88 from 1.86

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, week of Mar. 23

- 8:30am: Durable Goods, Feb., est. 3.0% (prior -3.7% (revised))

- 10:30am: DOE inventories

- 1:00pm, U.S. to sell $35b 5-yr notes

GOVERNMENT:

- President Obama has meetings at White House

- House, Senate in session

- House Energy Committee holds hearing on rising gasoline prices, 9:30am

- Senate Judiciary Committee holds hearing on special counsel’s report on the prosecution of Senator Ted Stevens, 10am

- House Appropriations subcommittee hears from Treasury Secretary Tim Geithner on the agency’s budget, 10am

- House Armed Services Committee holds hearing on security in the Korean peninsula, 10am

- House Ways and Means Committee marks up Small Business Tax Cut Act

- House Financial Services subcommittee holds hearing on the MF Global collapse, 2pm

- Senate Appropriations subcommittee hears from Treasury Secretary Tim Geithner on the Treasury Department’s response to the foreclosure crisis and rising student debt, 2:30pm

WHAT TO WATCH:

- U.S. Supreme Court today will consider how much of Obama’s health-care law must be thrown out if justices decide Congress can’t require Americans to buy medical insurance

- Applied Materials hosts investor day; watch for any update to 2Q forecast, market conditions

- Archer-Daniels-Midland seeking acquisitions in Europe and India and plans to increase exports from South America

- MF Global fund transfers to be scrutinized at House Financial Services subcommittee

- Orders for U.S. durable goods probably rebounded in Feb., rising 3%, as aircraft demand surged, economists est.

- Bats said to delay discussing new IPO for at least a quarter as CEO cedes chairman role

- Nokia announces availability of Lumia 800C device in China with China Telecom from April

- California said to probe planned purchase of EMI Group by Vivendi’s Universal Music and investor group led by Sony/ATV Music Publishing

- FDA advisory panel begins 2-day meeting on studying heart risks with diet pills, with voting question tomorrow

- Magic Johnson group wins Dodgers auction with $2b bid

EARNINGS:

- Jos. A Bank (JOSB) 6am, $1.58

- AuRico Gold (AUQ CN) 7am, $0.14

- Family Dollar Stores (FDO) 7am, $1.13

- Huntington Ingalls Industries (HII) 7:15am, $0.94

- AGF Management Ltd (AGF/B CN) 8am, C$0.27

- Commercial Metals Co (CMC) 8am, $0.09

- Unifirst (UNF) 8am, $0.88

- Lindsay (LNN) 8am, $0.82

- Paychex (PAYX) 4:01pm, $0.37

- Red Hat (RHT) 4:05pm, $0.27

- Verint Systems (VRNT) 4:05pm, $0.68

- Mosaic Co. (MOS) 4:15pm, $0.69

- Progress Software (PRGS) 4:29pm, $0.25

- HB Fuller Co. (FUL) 5:30pm, $0.37

- Texas Industries (TXI) Post-Mkt, $(0.82)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Rio, BHP Lose Faith in Diamonds Even as Prices Rise: Commodities

- Crude Oil Declines on Rising U.S. Supplies, Emergency Stocks

- Sugar Slides as Surplus May Be Nearer on India; Coffee Retreats

- Copper Declines on Indications Demand Is Slowing Down in China

- Soybeans Gain on U.S. Acreage Speculation, South America Drought

- Gold May Decline in London as U.S. Data Curbs Investor Demand

- Palm Oil Gains for Fourth Day on Concern Supplies May Decline

- BlackRock’s Raw Supports Glencore’s $35 Billion Xstrata Takeover

- Obama Power Plant Rule Seen Signaling Demise of ’Old King Coal’

- Goldman Reduces Three-Month Commodities Outlook to Neutral

- ADM Plans to Buy Oilseeds Capacity in Europe, India, S. America

- Transocean Biggest Winner From 28% Jump in Oil Rig Rates: Energy

- West African Cocoa Premiums Hold Steady Before Start of Harvest

- Oil Drops From One-Week High on Supplies

- Palm Oil Seen Climbing 23% on ‘Wedge’ Signal: Technical Analysis

- China Beats U.S. With Power From Coal Processing Trapping Carbon

- Glencore Sweetener Lures Xstrata-Wary Lenders: Corporate Finance

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

ASIA – oil up, growth slows – US Policy to Inflate continues to wreak havoc on the rest of the living world – while the SP500 hasn’t snapped yet, Asian stock markets are starting to (they stopped going up in Feb fyi); China down hard (-2.65%) last night and India down another -0.8%, taking its draw-down to -7.2% on the Sensex since Feb 21.

MIDDLE EAST

The Hedgeye Macro Team