Conclusion: True to form, PVH raised its outlook intra-quarter and we expect that also true to form it will come in close to a dime above Street estimates – that’s expected. We think the 2012 outlook is headed higher as a result. With our model at nearly $1 above the Street two-years out in 2013, we also expect an acceleration in revisions and expectations ahead for one of our favorite large-cap names in 2012.

TRADE (3-Weeks or Less):

We’re at $1.15 for PVH headed into Tuesday’s print after the close, which is ahead of the Street at $1.09 and guidance of $1.08-$1.10.

- Over the last three quarters, PVH has come in above consensus by an average of +3% on revenues and +9% on EPS. We don’t think PVH results broke this cadence in Q4.

- We expect sales to come in better than expected up +9% vs. +6.5%E in Q4 driven by CK up +14% to $284mm, Tommy up +12% to $788mm and the Heritage business essentially flat up +1% to $450mm. With sales running ahead of plan through the first two months of the quarter, we have little reason to suggest that the sales trajectory changed meaningfully in the last month based on what we’ve heard and seen across the rest of retail.

- As a result of stronger top-line results, we are at GMs of 51.3% reflecting -150bps of contraction over 100bps better than Street expectations for -260bps. Moreover, with the inventory setup favorable heading into year-end, we don’t expect atypical seasonal promotional activity beyond elevated clearance in the Heritage segment.

- In addition, we expect SG&A of $642mm up 5.5% yy reflecting 140bps of leverage.

- Short interest remains very low at ~3% of the float.

- Interestingly, sentiment as measured by our index has become more bullish over the last two-months with the stock up +26% YTD vs. the MVR up +18% and the S&P up +10%.

TREND (3-Months or More):

With the Tommy acquisition no longer artificially boosting sales in 2012, we expect top-line sales to slow on the margin in 1H and to +6.5% for the full-year reflecting uncertain demand at best in Europe and a turn in Fx to a headwind from a +2-4% tailwind in 2011. In addition, we think incremental marketing spend which has proven to be a key sales driver in 2011 and continued uncertainty leading to tighter inventory commitments from European retailers will keep earnings growth at a mid-teens rate. We’re at $6.21 vs. $6.02E in 2012.

- At CK, we expect revenues to slow modestly next year up +10.5% from +14.5% in 2011 with +8% growth in licensing and +12% growth in apparel driven by continued growth in underwear as well as the new Power Stretch jeans line.

- At Tommy, with most of its growth coming out of Europe (Germany and Spain top two markets by size), we expect demand to slow over in 1H of 2012 with continued weakness in Spain a key intermediate-term variable.

- The Heritage business is unquestionably the odd man out among the three businesses over the next two quarters. It’s undergoing a transformation getting out of unprofitable/underperforming lines in 2012. Timberland accounted for ~$80mm in revs, which will account for a 4-5% reduction in sales growth while we expect the core business to stabilize. Coming in ~3pts below historical operating margins of 10% in 2011, we expect profitability to improve (+110bps) on a lower revenue base in 2012.

TAIL (3-Years or Less):

While PVH works to stabilize its cash flow business (Heritage), it’s doing what the best brands do that license out their brands in order to grow into international markets – it’s starting to take back control of its own content. Driving brand sales directly at higher margin was key to RL’s success through much of the last decade as the company bought in its licenses. We don’t expect PVH to be any different.

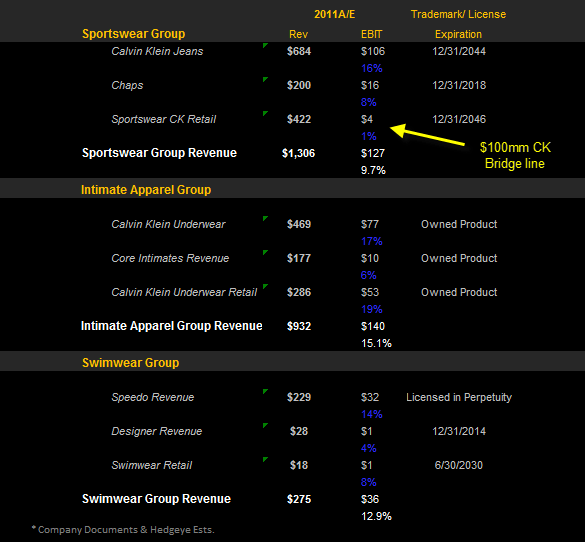

In fact, as we recently highlighted in our note “PVH/WRC: Understanding Licenses is Key,” we detailed how the recent CK bridge line it took back from WRC could add up to $0.75 in EPS 3-4 years out. Add on a few more of these and PVH’s earnings power could change materially higher.

We see continued upside at Tommy as well as CK resulting in EPS of $8 in 2013, a buck above consensus expectations. Following a strong end to the year, we expect an acceleration in revisions and expectations ahead for one of our favorite large-cap names along with RL and VFC in 2012.

Casey Flavin

Director

Management commentary from Q3 call:

Below is a table outlining WRC's product/license portfolio as highlighted in our note “PVH/WRC: Understanding Licenses is Key”: