“In the contest between inflation and deflation, the rope is the dollar.”

-James Rickards

I’ve finally jumped into a book I’ve been really excited about, James Rickards’ “Currency Wars”, and the preface does not disappoint. From a risk management perspective, I couldn’t agree more with the aforementioned quote.

Rickards takes the currency debate right up the middle on the Chairman of the Federal Reserve reminding us that “by printing money on an unprecedented scale, Bernanke has become a twenty-first century Pangloss, hoping for the best and quite unprepared for the worst.”

As a reminder to The Ben Bernank and his central planning followers, hope is not a risk management process.

Back to the Global Macro Grind…

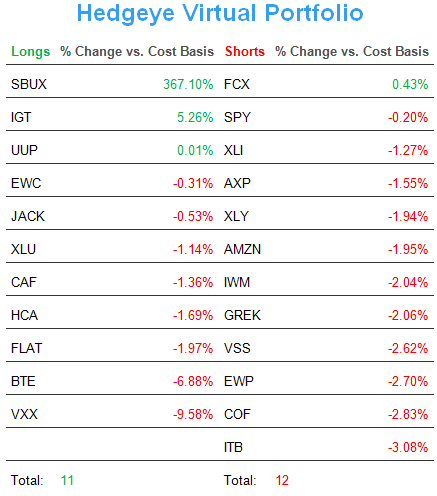

On Tuesday, I bought back my Strong Dollar position via the UUP. Yesterday, I sold my only remaining long Commodity position (Oil), taking my asset allocation to Commodities back down to ZERO percent.

Even though he’s never traded a Global Macro market with his own capital at risk in his life, Bernanke would probably smile when considering my 0% strategy move. The man likes zeroes.

The Zero Bound, or a 0% “risk-free” rate of return, concept is littered with unintended consequences. If you don’t believe that, ask the Japanese. They’ve had 20 years of anemic economic growth and will have 25% less people living in Japan come 2050.

If you do believe in the globally interconnected risk associated with the world’s reserve currency, you probably get why this entire “contest between inflation and deflation” comes down to what Bernanke/Geithner do to US Dollar policy (monetary and fiscal). When it comes to commodities inflating/deflating the CRB Index (19 commodities) has a 60-day correlation to the US Dollar of -0.64%.

Correlation? Yes Keynesians of the academic gridiron, unite! Correlation Risk in markets doesn’t always imply causality. But sometimes it does.

So why get long the US Dollar right here?

- It’s going up today, and we know performance chasers just love a good chase

- It is breaking out above our intermediate-term TREND support line of $79.33 again

- It has fortified its base, holding our longer-term TAIL support line of $76.11

- The Japanese Yen has moved into crash/crisis mode (bullish USD/YEN)

- The Euro continues to fail at $1.33 resistance as European Growth Slowing continues

Got Growth Slowing?

Apparently consensus doesn’t want to agree with us on this yet. In a note earlier this week I highlighted the Credit Suisse call to action that “economic momentum indicators suggest global and US growth is still well above consensus” – and while the people I used to work with there are good people, that call on growth is simply just wrong this morning.

1. ASIA: China and India, in particular, are showing glaring signs of Growth Slowing sequentially here in March. Whether it was India’s stock market down another -1.8% overnight (down -6.1% since the Feb YTD top) on a mounting deficit problem or both the Shanghai Composite and Hang Seng snapping their respective immediate-term TRADE lines of support in the last week as China’s PMI (HSBC) was printed overnight at a fresh 4-month low – it’s all there. #GrowthSlowing

2. EUROPE: Inflation Slows Growth; particularly when Europeans have to deal with Brent Oil prices of $122-127/barrel – never mind being bent over a barrel by that sneaky little Keynesian critter called debt (which structurally impairs long-term growth). Looking at Europe’s PMI numbers for March, here’s what the river cards look like:

Manufacturing:

A) France 47.6 MAR (exp. 50.2) vs 50 FEB

B) Germany 48.1 MAR (exp. 51) vs 50.2 FEB

C) Eurozone 47.7 MAR (exp. 49.5) vs 49 FEB

Services:

D) France 50 MAR (exp. 50.3) vs 50 FEB

E) Germany 51.8 MAR (exp. 53.1) vs 52.8 FEB

F) Eurozone 48.7 MAR (exp. 49.2) vs 48.8 FEB

Now we all know that Swiss turned American bankers can get creative in their accounting, but by our Canadian-American math, this morning’s Global Growth data is well below consensus.

How about US Growth?

- It has never NOT slowed with oil prices over $100/barrel (that’s why the FEB ISM number dropped 3% from JAN)

- Since 71% of US GDP = Consumption, real (inflation adjusted) growth slows, big time, when inflation accelerates

- Q4’s US GDP print of 3.0% carried a 0.86% Deflator; that deflator should double or triple in Q1

In other words, our Global Macro Model will not be surprised if US GDP growth gets cut in 1/2 , sequentially, from Q4 of 2011 to Q1/Q2 of 2012. If we don’t see a Strong Dollar (like we did in Q4) soon, you’ll see weakening US Consumption.

So that brings me to a comma, instead of a full stop. If you are staying one step ahead of me, you’re going to ask if Strong Dollar would get me more bullish on both US Economic Growth and US Equities. The answer to that (as it was every day in January 2012 up until Ben Shalom Bernanke decided to debauch the Dollar on January 25th), is yes.

Whether our almighty central planners like to admit it or not, we’ve all been Roped In. This “contest between inflation and deflation” has been called “risk on and risk off.” But risk is always on – especially the globally interconnected stuff. Risk never sleeps.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, and the SP500 are now $1, $122.12-124.89, $79.33-80.58, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer