Estimates still seem too high. People should focus on Demand, not Doors. In the end, consumer demand always prevails. There’s too much Hope baked into this story.

Our take on VRA following Q4 results hasn’t changed, we’re still negative on the name. People seem overly focused on doors, and not on end-demand. Demand will always win that battle. There still appears to be a substantial “trust” factor associated to 2H expectations. Hope, as we say here at Hedgeye is not a risk management process, we prefer to stick to the math. Here are some key takeaways from the quarter:

- Let’s start with the good news. The Direct segment came through better than expected. Comps up +9.3% resulted in a more modest deceleration in the 2yr trend than expected while e-commerce remained solid up +28% (but down sequentially from +50% in Q3). In addition, VRA’s sales/avg. sq. ft. productivity continues to climb up to $1,290 from $1,150, which is to be expected as stores mature on such a small base (now 56). However, our concern hasn’t been the retail business per se, which we expect to grow 32% in 2012, it’s the wholesale business that we think is at risk.

- In that regard, indirect sales were down -0.7% for the quarter on top of the easiest compare of the year. While management points to not having “those breakout patterns that we traditionally do” and how we should look at revenue growth trends on a full-year basis not quarterly, the reality is that sales across VRA’s network of 3,300 small independent retailers slowed meaningfully.

- Our sense is that VRA’s efforts to aggressively fill its uncharacteristically fragile wholesale channel with product headed into the holiday season has left little appetite for anything but modest reorders headed into the 1H.

- As expected, management discussed the 60 new doors at Dillard’s this year (~20% penetration) and also noted how they are “starting discussions” with other department store accounts. As noted in our prior note, this could certainly proved upside to sales growth in the channel, but we aren’t baking it into our model.

- This actually highlights a major piece of our call. People focus too much on door growth and not enough on product relevance and desirability. Additional retail stores and major department store accounts on top of its 3,300 existing doors does very little to impact end demand for the product. Yes, it will get more eyeballs on it. But it has an inverse impact on scarcity value. Retailers are not stupid. If they see product in a store at the other end of the mall that is identical to what is sitting in their stockroom collecting dust, they’re not reordering.

- VRA is ramping to nine new patterns in 2H compared to the historical 6-8, which helps address the issue, though the company is now extending some older successful patterns into new styles, something VRA has not typically done. Delaying the retirement of these patterns appears to undermine confidence in the current run if not indicate uncertainty/concern regarding current demand.

- In addition, Indirect segment margins were down sharply -580bps in Q4 due to higher fixed expenses (i.e. a larger sales force). It’s worth noting that the Indirect business needs to grow revenues MSD-to-HSD in order to leverage this new investment. Perhaps it should come as no surprise then that management’s full-year guidance for the business is…you guessed it, up mid-to-high-single-digit.

- This guidance for the Indirect business implies that when you strip out the contribution from another 60 Dillard’s doors accounting for roughly 3% revenue growth and incremental shop-in-shops in Japan, it assumes a modest contraction in the core channel. We don’t think that’s conservative enough. We have Indirect sales down 4% for the year reflecting cannibalization from company-owned stores and more conservative ordering to work down inventories. At this point in VRA’s growth cycle we shouldn’t be seeing the wholesale business rolling like this if there strong underlying demand in the market.

- As for margins, we expect operating margins down -275bps in Q1 and -215bps in Q2 and down -50bps for the year. We expect higher costs and the likelihood for higher promotional activity to weigh on gross margins in the 1H in addition to higher SG&A investments made in the 2H that we don’t expect to lever until Q4.

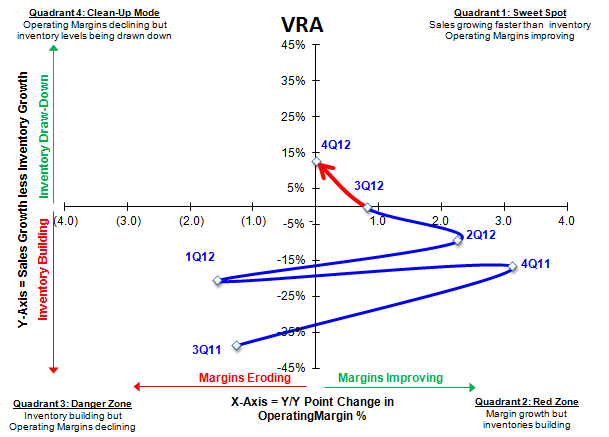

- Inventories at quarter end were one of the highlights of the quarter up +11% compared to +23% sales growth. As a result, the sales/inventory spread improved substantially after five straight negative quarters (see SIGMA below). This is bullish for gross margins on the margin, but we don’t think enough to offset the aforementioned pressures.

- Lastly, the DC expansion underway will moderate VRA’s typically strong FCF. With $36mm in CapEx budgeted for the year, we expect FCF margin to come in at 3% compared to 13% and 7% in each of the last two years. While we expect FCF margin to return to a HSD rate next year, this will limit VRA’s balance sheet flexibility near-term

All in we are shaking out at $0.27 for Q1 and $1.58 and $1.64 in EPS for F12 and F13 respectively 19% below Street expectations next year (F13). We continue to think the Street is missing the structural risk in VRA’s wholesale account base as it rolls out its owned-retail stores more aggressively. Despite a 9% hit to the stock today, we think there is more downside ahead as expectations head lower.

Casey Flavin

Director