Positions in Europe: Short Greece (GREK), Short Spain (EWP)

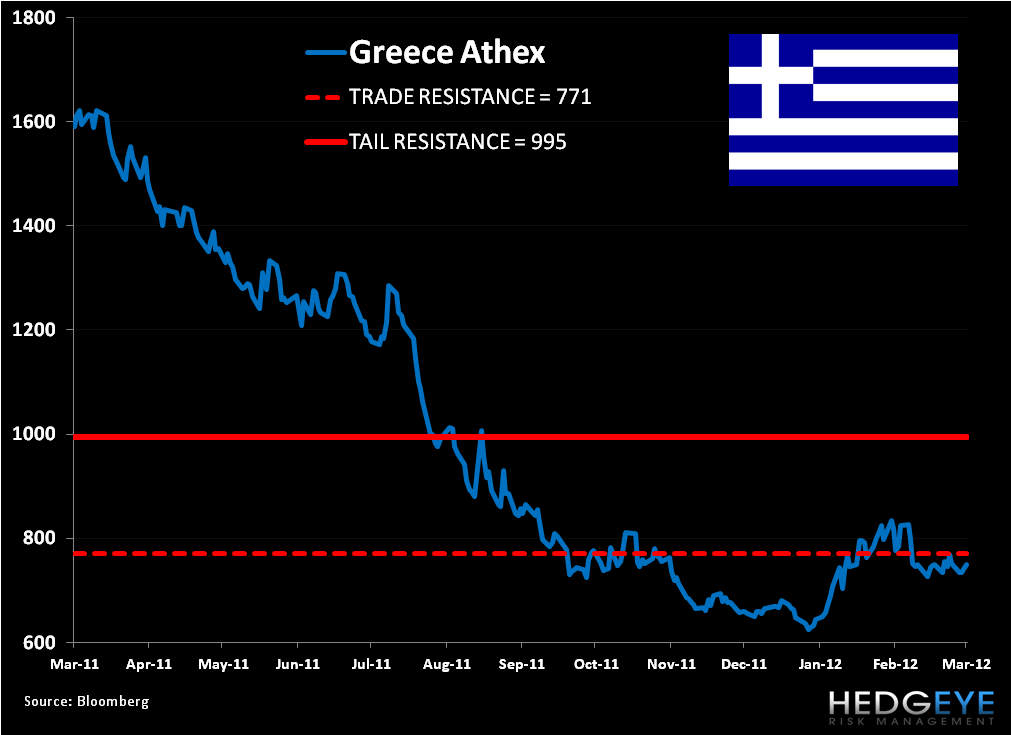

Keith shorted Greece in the Hedgeye Virtual Portfolio today with the Athex trading comfortably below its immediate term TRADE and long term TAIL levels (see chart below).

Greece remains the poster child for Europe’s sovereign debt excesses, of which its banks are highly levered. While many expect the ECB’s two 36 month LTROs liquidity injections to put Europe’s sovereign debt and banking crisis to bed, we’ll take the other side, and take advantage of price swings across the PIIGS equity indices, as growth expectations should continue to decline throughout 2012.

At a bare minimum, we think the assumptions from Troika that Greece can reduce its public debt to 120% of GDP by 2020 are overly optimistic, which implies the need for yet another bailout. But aren’t Eurocrats wishing for more bailouts ahead in artificially supporting an uneven union of countries, some of which should default and consider returning to their own currency?

In addition, we expect social unrest to erupt in Spain on the near horizon over unemployment and fiscal consolidation, which will further pack this already topped-off Eurozone powder keg.

Matthew Hedrick

Senior Analyst