Conclusion: CAPE valuation is at a level last seen on July 2011.

In the past, we’ve written a number of notes discussing the valuation of the broad equity markets and the implications of this metric. Anyone who watches CNBC, has often heard the refrain that the market is either cheap, or expensive, based on earnings multiples. Therefore, based on the valuation, the stock market is either a buy or a sell. Most often market pundits quote forward earnings estimates as their proxy for valuation. Unfortunately, these estimates are only as good as their inputs.

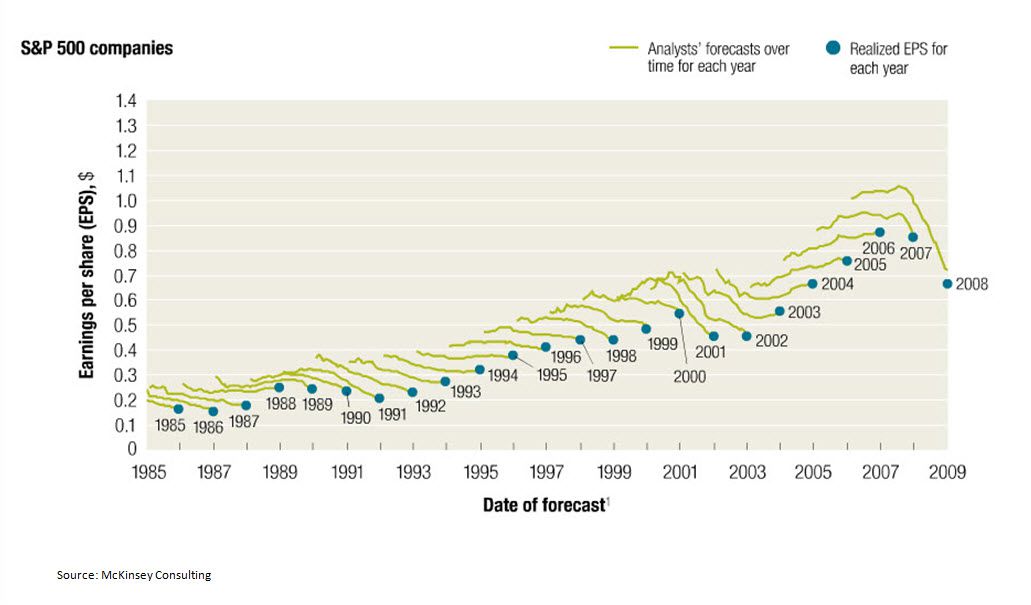

In the chart below, which is courtesy of McKinsey Consulting, we highlight the trend of S&P earnings estimates at the start of the year versus the actual realized earnings estimates going back to 1985. In 22 of the 24 years, the earnings estimates at the start of the year were higher than the actual estimates at the end of the year. To put that in context, 92% of the time over a 25-year period, analysts were too optimistic for SP500 earnings.

Now, of course, the world is replete with bad predictions, and I’ll flag a couple for some midday humor:

“Heavier-than-air flying machines are impossible."- Lord Kelvin, president, Royal Society, 1895

“I think there is a world market for maybe five computers."- Thomas Watson, chairman of IBM, 1943

The disturbing thing with many predictions or estimates is that they are made by perceived experts and are often wrong. Even more disturbing is when the perceived experts are wrong because of an obvious bias. As it relates to earnings estimates, there is clearly a positive bias among Wall Street analysts. For the time being, we will set an analysis of Wall Street 1.0 biases to the side, but just wanted to flag caution when buying a stock or equity market based on consensus forward earnings. History tells us that they are consistently too high.

We obviously have a number of factors we utilize when contemplating the direction of the markets. From a valuation perspective, we actually think that Yale Professor Robert Shiller’s methodology is a very relevant way to consider broad market valuations. By way of background, Professor Shiller uses what is called CAPE, or Cyclically Adjusted Price to Earnings. In terms of the numerator, or price, Shiller uses the monthly average of daily closes for the SP500. To derive the earnings data, in this instance the denominator, Professor Shiller uses the quarterly earnings data from the SP500’s website and utilizes an interpolation to provide earnings data by month. He then adjusts both the numerator and denominator for inflation using CPI from the Bureau of Labor Statistics. Finally, the inflation adjusted price is divided by an average of ten years of real monthly earnings to determine the CAPE.

In the chart below, we show the CAPE ratio going back to 1881, so more than 130 years. On this long range analysis, the current CAPE valuation, as the chart below shows, is clearly elevated. Currently, the ratio is at 21.94, which is the highest level since July 2011. Coincidentally, the SP500 began an almost 14% correction from early July 2011 to early August 2011.

To better quantify where the market currently is based on CAPE versus its long run averages, we split the CAPE ratios into quintiles. As the table below shows, the current valuation is in the highest quintile of the past 120 years.

Quintile Ranges of CAPE Rations 1

Certainly, a valuation case can be convenient, but if we look at the long run normalized cyclical earnings of the market, reversion to the mean suggests there is more downside than upside. Unless, of course, earnings growth accelerates dramatically, which isn’t a scenario we see in the current slow growth environment.

Daryl G. Jones

Director of Research