THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer

Initial jobless claims for the week ended March 10th came in at 351k versus 357k consensus and a revised 365k for the week prior (initially 362k).

Commentary from CEO Keith McCullough

The good news is Greece is out of the Bloomberg Most Read (Today = #1 Goldman, #2 China, #3 Apple):

- ASIA – post the USA meltup in everything Apple and celebrations in Financials to a made-up test, Asia has basically been down for the last 2 days (Equities), with China and India leading the decline. Bulls were begging for India to cut rates last night and they didn’t (inflation), so the Sensex dropped -1.6% on that and snapped TRADE line support of 18,023, again. China’s FDI print was down -0.9% y/y – not good.

- SPAIN – acts like le chien de Sarkozy; the IBEX continues to flash a major negative divergence vs Global Equities as of late (Spain -1.4% YTD w/ Germany +20%!); when your stock, currency (Euro), and bond markets are all falling at the same time – not good.

- TREASURIES – here’s your hat-trick of ‘not goods’; if you are long anything in Fixed Income, that is (who would be?) – Treasury Bonds are getting blasted – 2yr yield have moved +44% to the upside in 2 weeks. It’s a good thing there is zero asymmetric risk w/ the Bernank’s zero bound policy.

People chasing performance can convince themselves this rally in Japanese, American, or Venezuelan stocks is all about Growth – or they can be realistic and just call it a chase. They chased into March end of 2008, 2010, and 2011 – that didn’t turn out so well by August.

KM

SUBSECTOR PERFORMANCE

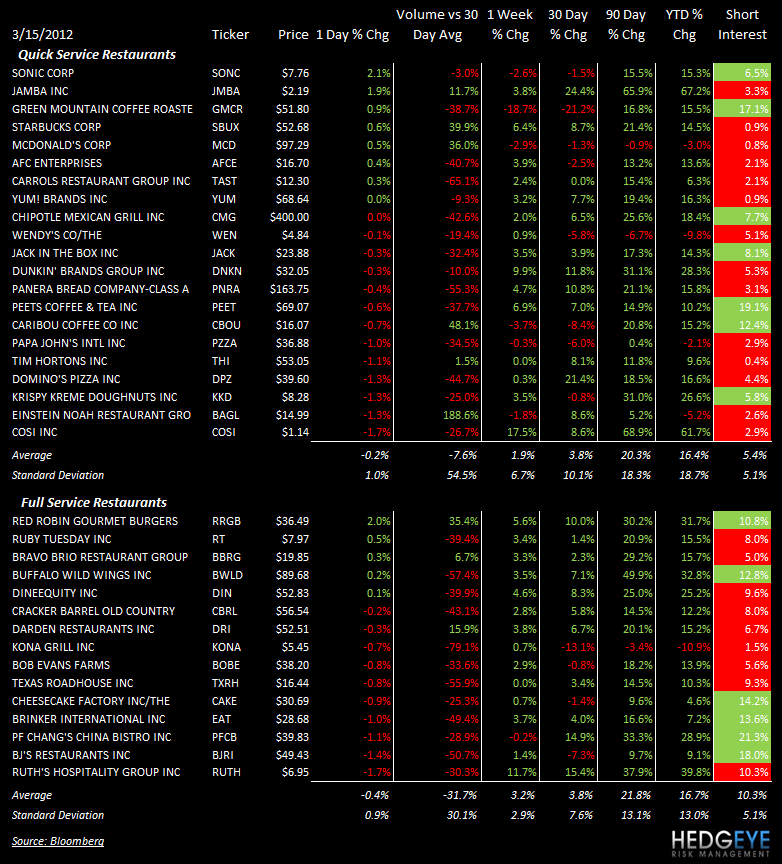

QUICK SERVICE

SBUX: Deutsche Bank increased its price target on Starbucks from $59 to $61 on possible catalyst for sales from the company’s light roast launch.

CASUAL DINING

RUTH: Ruth’s Chris has kicked off its “Sizzle, Swizzle and Swirl Happy Hour” premium bar menu at select locations, featuring food and drink items for $7, according to nrn.com.

PFCB: P.F. Chang’s was raised to Hold from Sell at Argus Research.

BWLD: Buffalo Wild Wings CEO Sally Smith appeared on CNBC’s show, Fast Money, last night and was not asked about wing prices once. March Madness is good for business, though.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

RRGB: Red Robin Gourmet Burgers gained 2% on accelerating volume.

Howard Penney

Managing Director

Rory Green

Analyst