This note was originally published at 8am on February 29, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Demography is destiny.”

-Auguste Comte

This Friday we are hosting a conference call for our macro subscribers on Japan titled, “Japan’s Debt, Deficit and Demographic Reckoning”. (If you aren’t a macro subscriber and want to get access to the presentation, email sales@hedgeye.com for subscription details.) During the presentation, we will spend a fair amount of time framing up the economic history of Japan starting with the American occupation post World War II. When contemplating economic history, I’m often reminded of George Santayana’s quote:

“Those who cannot learn from history are doomed to repeat it.”

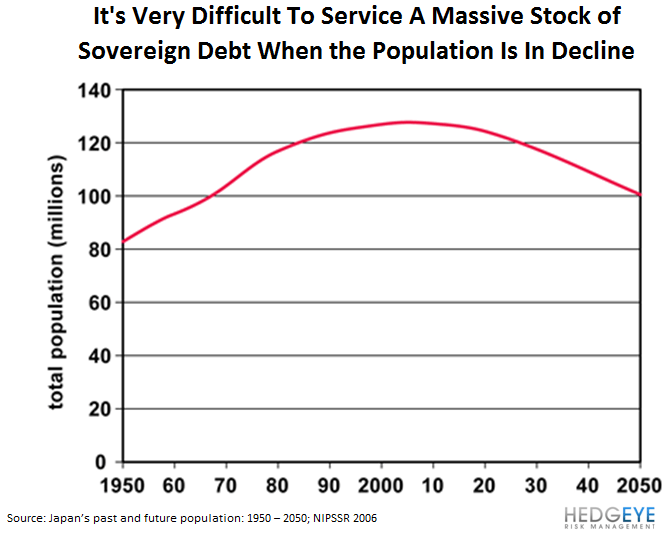

Certainly, history provides a critical frame of reference for Japan. In particular, the last twenty years of economic history in Japan, which witnessed a massive build up in Japanese sovereign debt (currently 220% debt to EBITDA) and stagnating economic growth (just +8.5% nominal growth over the last 20 years), have set the table for Japan’s future. But as my colleagues (hat tip to Darius Dale and Josefine Allain) and I have been grinding through this 80+ page presentation, the idea that Demography is Destiny truly represents the next chapter for Japan.

Currently, according to estimates from the CIA fact book, 23% of the Japanese population is over 65 years old. This compares to only 13% in the United States and approximately 8% for the rest of the world. As one of the world’s oldest countries, the burdens of supporting this aging population are seen directly in the Japanese federal budget. In the 2012 Japanese federal budget, social security spending will be just over 29% of the entire budget. This compares to 17% of the federal budget in 1990.

Due to a low fertility rate, the Japanese death rate currently exceeds the Japanese birth rate. In the absence of meaningful immigration, this implies that the Japanese population is in decline. As I outline in the Chart of the Day, based on the Japanese government’s own projections, their population will decline by more than 25% by 2050. In conjunction with said declines, the Japanese population is aging and by 2050 more than 40% of the population will be over 65. (And to think at 38 I thought I was getting old!) The demographic future of Japan will only accelerate social security entitlement spending.

The other concern with an aging population is growth. Robert Arnot and Denis Chaves recently wrote a paper for the Financial Analysts Journal called, “Demographic Changes, Financial Markets, and the Economy”, in which they attempt to quantify the relationship between demographics, growth and capital market returns based on 60 years of data. They conclude that:

“ . . . senior citizens contribute to neither GDP growth nor stock and bond market returns; they divest to buy goods that they no longer produce.”

Based on their projections, the aging population will negatively impact Japanese growth over the next decade by ~-5% in aggregate.

In theory an aging Japanese population, even if a major headwind for growth, could be overcome by the appropriate mechanisms and policy. Unfortunately, after more than twenty years of deficit spending, Japan’s proverbial hands are increasingly tied by debt. Specifically, Japan has massive non-negotiable financial burdens due to the second largest component in the proposed 2012 Japanese budget being debt service.

Servicing and interest on sovereign debt outstanding are projected to total 24% of Japan’s federal budget in 2012. This line item has almost doubled since fiscal 1980, when it was at 13%. I may not have a PHD in economics, but even I can tell you that if 1/4thof the Japanese federal budget is going towards debt service that spending is not generating an incremental return, either in the way of GDP growth or a higher standard of living, for Japanese society.

In a scenario analysis, we used a more normalized interest rate of 5.5%, which last occurred back in 1995, and applied that interest rate to the current debt servicing burden. At this interest rate level, the Japanese debt servicing burden would be 100% of the current federal budget. Clearly, increasing interest rates would squeeze out the government’s ability to more proactively invest in the nation and/or support rising social security expenditures.

To be sure, we are not projecting an imminent Japanese default, but in the short term with Japanese maturities accelerating in 2012, and specifically in March, there is increased concern as to Japan’s creditworthiness. Based on the scenario I described above, the longer term question is whether Japan will be able to fund its future. For the last twenty years, this funding has been enabled by a combination of high savings rates (both corporate and individual) and a current account surplus. Currently, we are seeing negative inflection points in both areas.

Ultimately, as Shakespeare wrote, “What is past is prologue”, and as it relates to Japan the past is indeed written. Increasingly, Japan’s future is also already largely written by her Demographic Destiny.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), USD/JPY, and the SP500 are $1752-1806, $122.01-126.19, $79.71-80.98, and 1361-1376, respectively.

Keep your head up and your aging stick on the ice,

Daryl G. Jones

Director of Research