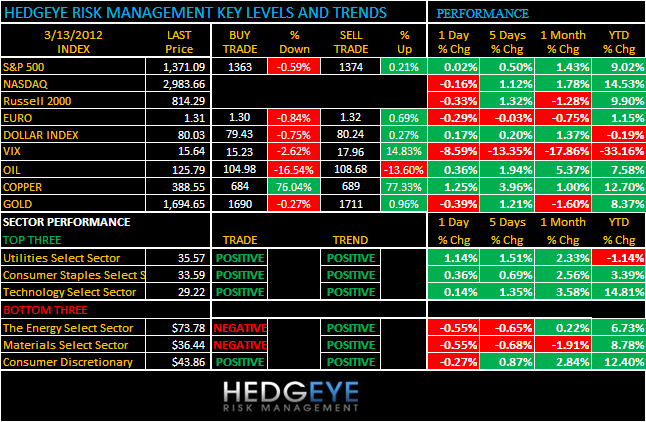

TODAY’S S&P 500 SET-UP – March 13, 2012

As we look at today’s set up for the S&P 500, the range is 11 points or -0.59% downside to 1363 and 0.21% upside to 1374.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -365 (-1567)

- VOLUME: NYSE 643.71 (-10.48%)

- VIX: 15.64 -8.59% YTD PERFORMANCE: -33.16%

- SPX PUT/CALL RATIO: 1.36 from 1.57 (-13.38%)

CREDIT/ECONOMIC MARKET LOOK:

US Deficit – we know it doesn’t matter anymore, right? Right. At -$237B for FEB that’s a new US record for monthly deficit print and should remind genius growth forecasters that tax revenues are collected on a real-basis too. Inflation at the pump finally running as headline headwind for Obama even in the NY Times poll this morning. US Tax revs are down y/y in FY 2012 vs FY 2012, despite the GDP “recovery”… spin.

TREASURIES – either 2s and 10s are testing a breakout in the US this morning because credit risk is rising on the margin (deficit) and/or Bernanke is going to be less dovish than he has been for the last 6yrs at today’s FOMC whisperings. Asymmetric risk lives on as long as this ridiculously short-sighted game of chasing yield does. Breakout lines for 2s and 10s = 0.26% and 2.03%, respectively.

- TED SPREAD: 39.72

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.05 from 2.03

- YIELD CURVE: 1.72 from 1.71

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Business, est. 94.5 (prior 93.9)

- 7:45am/8:55am: ICSC/Redbook weekly comp sales

- 8:30am: Advance Retail Sales, Feb., est. 1.1% (prior 0.4%)

- 10am: IBD/TIPP optimism, est. 50.0 (prior 49.4)

- 10am: JOLTs Job Openings, Jan., est. 3334 (prior 3376)

- 10am: Business Inventories, Jan., est. 0.5% (prior 0.4%)

- 11:30am: U.S. to sell $40b 4-week bills

- 1pm: U.S. to sell $21b 10-yr notes (reopening)

- 2:15pm: FOMC Rate Decision, est. 0.25% (prior 0.25%)

- 4:30pm: API

GOVERNMENT:

- President Obama takes British PM David Cameron to a basketball game in Ohio

- Senate Democratic Leader Harry Reid will force a vote on 17 of Obama’s judicial nominees starting today

- House in recess all week

- Supreme Court not in session

- Defense Secretary Leon Panetta traveling in Kyrgystan

WHAT TO WATCH:

- U.S. to file complaint at WTO today over Chinese limits on exports of rare earths used in high-tech products

- Retail sales probably rose 1.1% in Feb., the most in five months, spurred by strongest demand for automobiles since 2008

- FOMC meets today; Fed Chairman Bernanke said Jan. 25, after last meeting, that policy makers were considering additional asset purchases to boost growth

- Intel said to be considering creating online pay-TV service that works on TV sets, computers, mobile devices

- Alabama, Mississippi hold primaries in the Republican presidential race; Hawaii holds caucuses

- Facebook accused in lawsuit by Yahoo! of infringing patents covering functions critical to websites, including Internet advertising, information sharing and privacy

- Disney annual meeting in K.C, Missouri today; Glass Lewis opposes five nominees to board

- Chevron hosts analyst meeting, 9am

- Euro-area finance ministers signed off on second Greek bailout

- Employers in U.S. plan to boost hiring during next three months as pace of economic growth picks up: Manpower survey

- More than twice as many Americans view economy’s prospects as brightening as see them darkening, reversal from nine months ago, according to Bloomberg National Poll conducted March 8-11

EARNINGS

- Factset Research (FDS) 7 a.m., $1.12

- Empire Co (EMP/A CN) 7:20 a.m., C$1.10

- Raven Industries (RAVN) 9:10 a.m., $0.48

- Transcontinental (TCL/A CN) 9:50 a.m., C$0.34

- Power Financial (PWF CN) 11:20 a.m., C$0.59

- Alimentation Couche Tard (ATD/B CN) 11:23 a.m., $0.48

- Francesca’s Holdings (FRAN) 4:01 p.m., $0.17

- Zhongpin (HOGS) 4:10 p.m., $0.51

- Capital Power (CPX CN) 5:59 p.m., $0.35

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Milk Souring as Record Profit Spurs Herd Expansions: Commodities

- Copper Advances as Economic Rebound in U.S. May Stoke Demand

- Oil Gains From One-Week Low as Economy Lifts Fuel-Demand Outlook

- Gold Declines in London Before Fed Meeting as Dollar Strengthens

- Vekselberg Quits Deripaska’s Rusal, Citing ‘Deep Crisis’

- Soybeans Advance as China Seen Boosting Purchases; Wheat Rises

- Palm Oil Gains to Nine-Month High as Malaysian Inventory to Drop

- Kansas Wheat Faces Weather Risk as Warm Spell Aids Crop Progress

- Water Pollution Tied to Agriculture Increasing, Costing Billions

- Viterra Soaring on Bid Talk Still Offers 42% Discount: Real M&A

- Iran Oil Power Declining as Explorers Increase Spending: Energy

- Obama Takes Aim at China With WTO Case on Rare-Earth Export Caps

- Ore-Shipping Rates Seen 13% Lower as China Cuts Target: Freight

- Natural Gas Falls to 10-Year Low on Weather

- Natural Gas Falls to 10-Year Low on Mild Weather, Record Output

- Copper ETP Investments Increase to Record, ETF Securities Says

- Rubber Climbs for Fourth Day as Yen Weakens, Supply May Decline

CURRENCIES

EUROPEAN MARKETS

SPAIN – despite the concept that all is fine in no-volume rallies until it isn’t, the rest of the world’s deficit/debt problems do not cease to exist. The recent breakdown in Spanish stocks and bonds show you that in pictures – now the Euro is failing to overcome $1.32 resistance as well. Sovereign Debt risk never goes away, but its intensity focuses the mind when country currencies, stocks, and bonds do the same thing at the same time.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team