TODAY’S S&P 500 SET-UP – March 12, 2012

As we look at today’s set up for the S&P 500, the range is 19 points or -0.50% downside to 1364 and 0.88% upside to 1383.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1202 (-575)

- VOLUME: NYSE 719.04 (0.34%)

- VIX: 17.11 -4.68% YTD PERFORMANCE: -26.88%

- SPX PUT/CALL RATIO: 1.57 from 0.98 (60.20%)

CREDIT/ECONOMIC MARKET LOOK:

USD – the most important (and bullish on the margin for US Consumption Growth) recovery in the last few weeks has been the US Dollar Index recovering its intermediate-term TREND support of $79.36. With short-term Treasuries (2yr) breaking out above 0.26% TREND support and Gold struggling relative to oil, we are out of Gold for now. Considering the short side GLD and looking to buy USD back.

- TED SPREAD: 39.22

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.02 from 2.03

- YIELD CURVE: 1.71 from 1.71

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Export inspections: corn, soybeans, wheat

- 11:30am, U.S. to sell $33b 3-mo., $31b 6-mo. bills

- 1:00pm, U.S. to sell $32b 3-yr notes

- 2:00pm, Monthly Budget, Feb., est. -$229.4b (prior -$222.5b)

- 3:15 p.m. Bank of England’s Fisher speaks in London

GOVERNMENT:

- Rick Santorum, Newt Gingrich hold rival events in Biloxi, Miss. ahead of Tuesday primary

- House not in session this week, Senate in

- Supreme Court in session, rulings expected

WHAT TO WATCH:

- Glencore said to have made approach for Viterra; Cargill may have expressed interest: WSJ

- World Trade Organization may rule on appeal of decision that Boeing got at least $5.3b of illegal U.S. subsidies

- Boehringer Ingelheim will consider buying Pfizer’s animal health business, provided co. sells it in parts: Economic Times

- Fed’s extension of maturities, known as Operation Twist, may lower 10-yr yield by 85 bps: Bank of International Settlements

- Fed said to be pushing back against some banks’ proposals to pay dividends, buy back shares after concluding lenders underestimating potential losses on consumer debt

- Wells Fargo, Citigroup may join banks unleashing more than $9b in div. increases, shr buybacks if they get passing grades this week on Fed’s annual stress test

- Chevron aims to catch up on Marcellus gas drilling: WSJ

- Asahi Kasei agreed to buy Zoll Medical for up to $2.2b

- Temenos, Misys fail to reach agreement, terminate talks; Misys says talks with Vista, CVC/ValueAct continuing

- Global banking regulators will seek accord later this month on changes to draft liquidity rules criticized by some govts, lenders as threat to economic recovery

- Average price for regular gasoline at U.S. filling stations increased 12.31c to $3.8148/gallon over past 2 wks: Lundberg

- Swatch to contest counterclaim by Tiffany & Co. over end of alliance between the cos.

- Euro-area finance ministers meet to discuss Greece’s progress in fulfilling commitments under a 130b euro rescue program

- Craig Bouchard, co-founder of Esmark, said to be close to announcing deal to buy HD Supply’s pipe, valve distribution unit for ~$500m

- Disney’s “John Carter” took in $30.6m in U.S. Canada, trailing “The Lorax"; est. range: $25m-$38.9m

- No U.S. IPOs scheduled

EARNINGS

- FuelCell Energy (FCEL) Pre-Mkt, $(0.06)

- Silver Standard Resources (SSO CN) Pre-Mkt, $(0.12)

- Urban Outfitters (URBN) 4pm, $0.29

- Carmike Cinemas (CKEC) 4:02pm, $0.16

- Clean Energy Fuels (CLNE) 4:05pm, $(0.17)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds Trimmed Wagers Before Prices Rebounded: Commodities

- Oil Drops From One-Week High as China’s Exports Miss Forecasts

- Coffee Declines to 17-Month Low on Speculation of Brazil’s Sales

- Copper Falls on Signals of Slowdown in China, Largest Consumer

- Gold Declines as Commodities Slide, Hedge Funds Cut Holdings

- India Ends Cotton-Shipment Ban, to Revalidate Existing Permits

- Palm Oil Inventories in Malaysia Climb 2% as Exports Drop

- Soybeans May Gain After USDA Cut Forecast on Global Inventories

- Rubber Top May Be 358 Yen, Fibonacci Shows: Technical Analysis

- Aluminum Stockpiles in Japan Drop From Highest Since 2009

- TNK-BP Yield Drops Below Gazprom as Oil Beats Gas: Russia Credit

- Bullish Oil Bets Drop as Tension With Iran Eases: Energy Markets

- Soybean Imports by China May Rise to Record, Grain Bureau Says

- Cotton Declines as India Scraps Export Ban

- Glencore Said to Express an Interest in Grain-Handler Viterra

- Chesapeake CEO Courts Asians for $100 Billion Resource: Energy

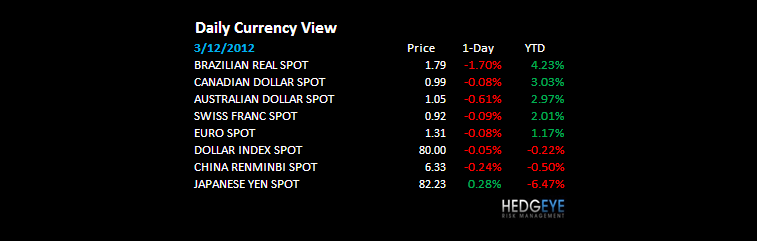

CURRENCIES

EUROPEAN MARKETS

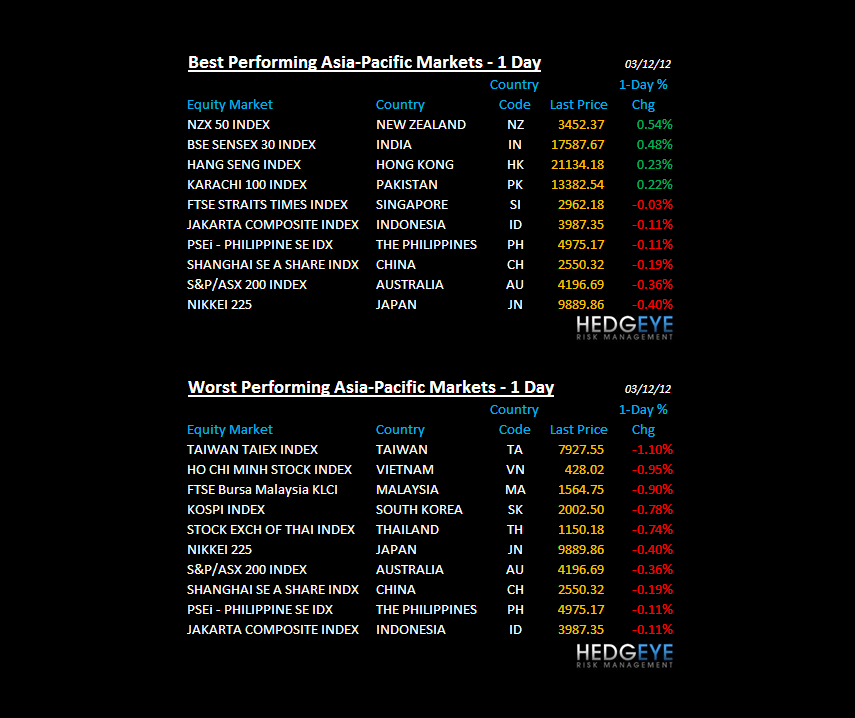

ASIAN MARKETS

CHINA – worst Trade Deficit in 22yrs (let’s call that ever – and ever is a long time) at -$31.5B after last week saw that big sequential drop in Chinese IP growth (to 11% vs 14% in JAN despite Lunar shift). Growth Slowing. Chinese stocks looking for a rate cut.

MIDDLE EAST

ISRAEL – someone knows something or someone thinks they do – what we can’t see here makes us call it out as the Tel Aviv25 Index not only moved to red for 2012 YTD last week, but is down another full 1% this morning (down -4% in since Feb 21). Iran?

The Hedgeye Macro Team