February is only one month but MCD needs global sales trends to remain strong to maintain its current valuation. February, if this morning’s release is any indication, could be the first sign that MCD is not immune to the global economic reality.

Our stance on the stock at this point is to wait and see. We are not buyers of the stock on this selloff. In short, if austerity is having an impact it will not be a one month phenomenon.

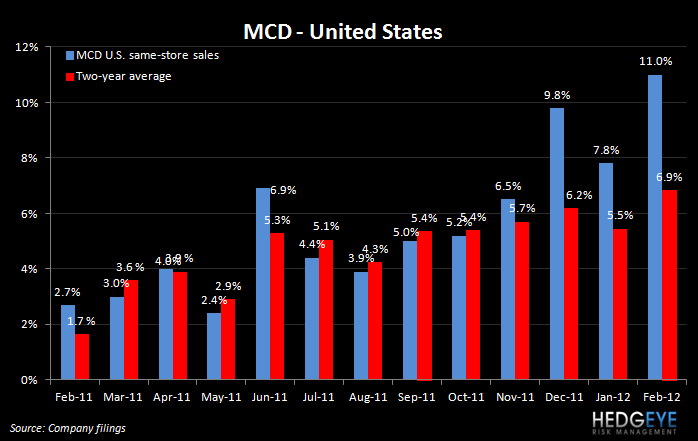

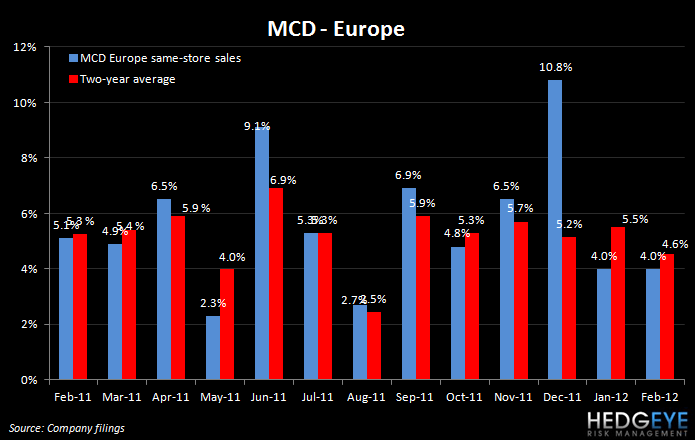

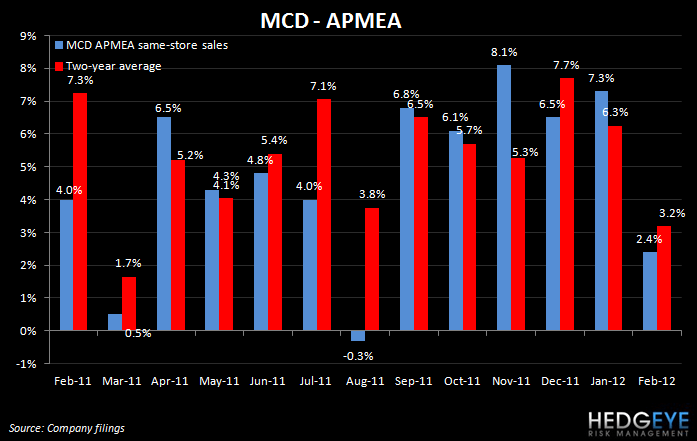

FEBRUARY SALES

Adjusting for all the noise (weather and the trading days), in the month of February there was a sequential slow down in traffic trends in McDonald’s global business. In Japan the “Great American Burger” promotion, in its third year, lost steam and the Chinese New Year also negatively impacted the headline APMEA number. In Europe, France and Italy are a drag on same-store sales, while Spain – albeit modeslty – and Germany are having a positive impact.

Adjusting for calendar-shifts, all three divisions saw declines in two-year average comparable restaurant sales trends. Japan reporting -1.2% was also a disappointment for the company.

The February top line results in the USA adjusting for the leap year suggest a decline in two year trends as well as in the rest of the world. Japan reporting down 1.2% was a big disappointment to the Asia region.

McDonald’s reported sales of 11.1%, 4.0%, and 2.4% for the U.S., Europe, and APMEA, respectively. Consensus was looking for 8.7%, 6.8%, and 8.6%, respectively. Due to calendar shifts, the numbers include an adjustment ranging from approximately 3.1% to 3.4%.

THOUGHTS ON INVESTOR EXPECTATIONS VS MGMT COMMENTARY

We were struck by the words “as previously communicated” in this morning’s press release because, while management did highlight the uncertain economy, austerity in Europe, and inflation as issues that posed business risk to the company, these factors have been withstood for some time by the McDonald’s business. The oft-repeated explanation for MCD being the Teflon Don of the restaurant space last year was that the economic malaise actually benefitted the company. Management’s commentary on conference calls never explicitly said this, but it was certainly inferred by many in the investment community; management recently said, “…at the same time, Europe stayed committed to delivering compelling fourth-tier options and promoting everyday affordable pricing for consumers feeling the pressure in their local economies”… “despite this backdrop, our European business remains strong” (1/24 transcript). The question is, from here, has the game changed for McDonald’s? Was the investment community far too optimistic in its reading of management’s commentary and the apparent immunity of McDonald’s business to economic uncertainty? Why is the soft economy now impacting results when it has little effect previously?

From a bottom line perspective, the impact of any top line slow down will be compounded by the fact that both D&A (from the all the remodels last year) and G&A, which will be up 6% in 2012 (due to technology, the Olympics, and world-wide franchise convention), are putting pressure on reported operating profit.

A quick scan of all of MCD recent filings terms “austerity” is mentioned two times in the most recent 10-K and nine times in the most earnings call. “Labor cost pressures” was mentioned once in the most recent 10-K and zero times in the most recent earnings call. “Economic uncertainty” was mentioned three times in the most recent 10-K and zero times in the most recent earrings call transcript. Again, management did communicate these issues, but we need to read between the lines to get to the conclusion about the impact on 1Q12.

The economic uncertainty and austerity measures in Europe are not new. Commodity inflation is not a new trend either; beef prices have been moving higher but that is neither a new trend nor should it be a surprise. Management highlighted mid-teen inflation in beef costs as being the most significant impact on COGS in 2011 and guided to a similar level in 2012 during the 4Q EPS call on 1/24.

From the 10-K filed on 2/24/12: “In 2012, our European business will continue to face headwinds due to economic uncertainty and additional government-initiated austerity measures implemented in many countries. While we will closely monitor consumer reactions to these measures, we remain confident that our business model will continue to drive profitable growth.” Again, no sign that there was going to be any real margin pressure – in fact this suggests less pressure in Europe this year versus last year.

From the most recent earnings transcript management filed on 1/24/12: “Europe's commodity inflation is expected to moderate a bit in 2012, with a projected increase of 2.5% to 3.5%.” Additionally, the company said that the impact of “austerity” in 2012 was going to be less severe than in 2011, stating, “…some of these incremental austerity measures, so the increased social charges and some of the other taxes that are hitting the restaurants, those are going to be, while we'll have some new ones, the magnitude of those will be lower than we saw in 2011.”

Our stance on the stock at this point is to wait and see. We are not buyers of the stock on this selloff. In short, if austerity is having an impact it will not be a one month phenomenon.

Howard Penney

Managing Director

Rory Green

Analyst