We follow the ICSC U.S. Chain Store Sales Index closely and see the trend quarter-to-date as a red flag for Cheesecake Factory’s top line.

The ICSC-Goldman Sachs weekly chain store sales index rose by 1.3% in the latest week through March 3rd. According to the ICSC, “year‐over‐year sales softened appreciably to a 1.7% pace‐‐its weakest pace since the week ending January 9, 2011 (+1.6%).” Tellingly for CAKE, the ICSC-Goldman Sachs consumer tracking survey found a “modest pickup in discount store business over the past week, but weaker business at department stores.” We see Cheesecake Factory’s business as being more closely tied to department store traffic than traffic at discount stores.

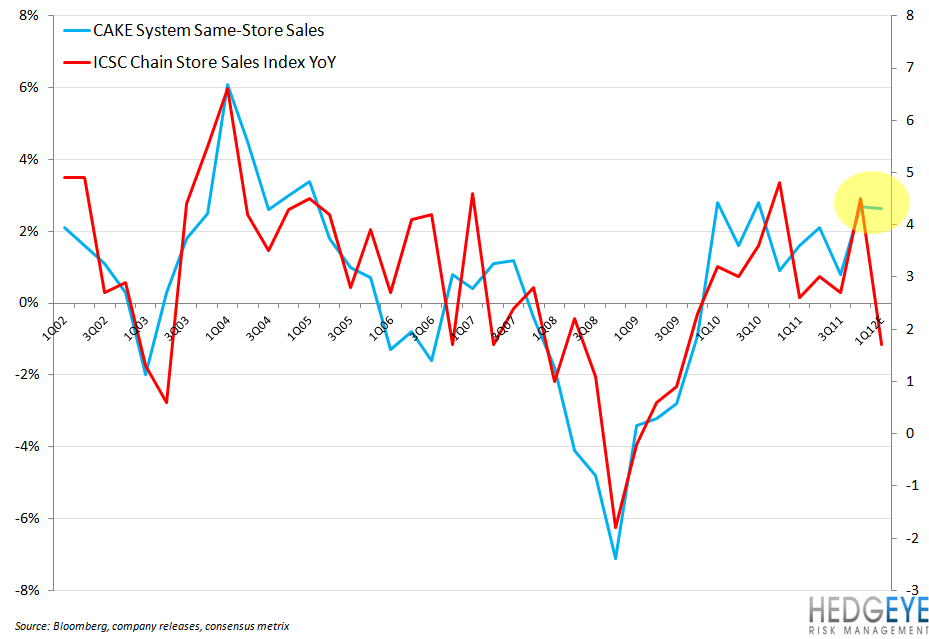

The two lines in the chart below represent Cheesecake Factory comps and the ICSC Chain Store Sales Index year-over-year change. The aforementioned ICSC dataset details the weekly change but, clearly, for comparability purposes it is necessary to monitor Cheesecake Factory comps versus the year-over-year move in the ICSC data. The 1Q12 data point for Cheesecake Factory represents current consensus expectation of +2.63% while the ICSC Chain Store Sales Index year-over-year number is the quarter-to-date figure including all weeks through March 3rd. The correlation for the data represented in this chart for 1Q02 through 4Q11 is 0.8.

Howard Penney

Managing Director

Rory Green

Analyst