March GGR estimate up 23-33% YoY

It’s only 4 days so not much read through yet but we’ll tell you what we have. Average daily table revenues were HK$748MM which is down from February’s surprisingly strong HK$779MM. We would have expected better since two out of the four days were weekend days. On a full month basis, the calendar is favorable with one extra weekend days. Some people are saying two extra weekend days but the Macau government counts one day in arrears. Overall for the full March including slots, we are estimating GGR at HK$24-26 billion, up 23-33% YoY. Last year in March, VIP hold was percentage was the lowest of the year.

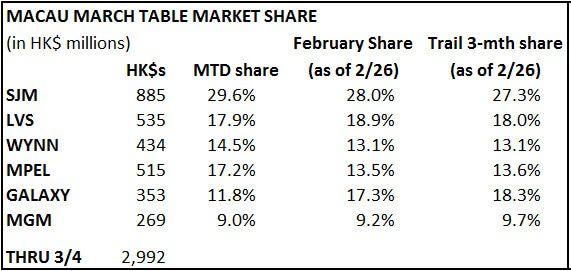

Market share is irrelevant at this stage of the month so we have little commentary other than to say Galaxy looks like it is taking one on the chin in terms of hold. Galaxy has been struggling with share recently and we expect that trend to continue, particularly with the opening of Sands Cotai Central next month. Wynn and MPEL are off to strong starts.