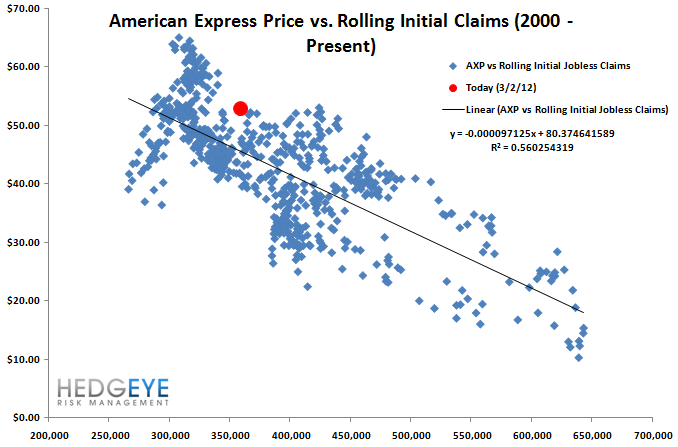

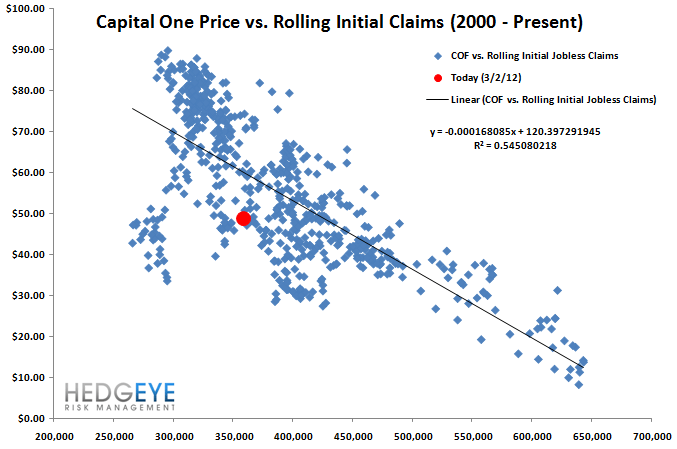

The Implications of a Rollover in Claims for the Card Stocks

The credit card stocks are among the most-correlated names to inflections in jobless claims. We anticipate the claims have troughed and will start gradually backing up towards 380k over the next three to five months, which will create a headwind for COF, AXP, and DFS.

In the charts below we show the long-term weekly relationship between the credit card stocks and rolling initial jobless claims. Note that all three of these charts are over a long time period: from 2000 to present for COF and AXP and since the IPO for DFS.

Why We Expect Claims to Rise

In our note last week, we walked through a quantification of the distortion in seasonal adjustment factors arising from the Lehman shock in 2008. Because the Labor Department uses a five-year lookback to create its seaosnal adjustment, the 2008 shock is still percolating through the data. See our note from last Thursday for more detail.

The seasonal distortion plays out as follows. Claims are understated by the largest amount in the last weeks of February. From now through May, the understatement disappears. Absent an underlying trend in the series, this effect would drive claims higher by about 20k over the course of the next three months. By July, the distortion reappears, this time as an overstatement, pushing claims slightly higher still. From July through year-end, the distortion disappears, and the underlying trend will be reflected in the weekly data.

Long-Term Ceiling

There's another set of implications for this analysis: the long-term call. Looking at the charts of AXP and COF in particular (since DFS hasn't been public through a full decade), it's striking that the stocks seem to retrace their steps almost exactly from one cycle to the next. This is the natural consequence of failing to accrete TBV over the cycle. American Express in particular is eager to spend cash on buying back stock at multiples to tangible, a process that is guaranteed to reduce TBVPS in exchange for growing EPS.

Keep in mind that claims don't go much lower than 300,000, and right now we're already at 350,000. That's not a lot of room to play for. For the stocks to go meaningfully higher, they need loan growth, multiple expansion, or a very extended stay with claims at 300k.

Bottom Line

This reversal in jobless claims should put a lid on upside in these card stocks from now through the end of the summer. Therefore, on the long side you're playing for arguably very little. However, that opens up the possibility of serious downside in the event that gas prices, Iran or any of a number of the other risk factors we're monitoring come to pass. We see the setup for these stocks over the next five months as asymmetrically negative.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.