As expected, Jack in the Box provided a comprehensive update on the business model and the direction the company is heading over the next three years.

We still believe that there is upside in JACK’s cash flow multiple (EV/EBITDA) from the current 7.4x EV/EBITDA level to a range of 8-9x which implies, at its midpoint, 28% of upside from current levels. Yesterday’s Investor Conference was the coming out party for the new Jack in the Box, Inc. As the company nears the end of its refranchising program at Jack in the Box, investments in menu, service and the store base have driven sales and traffic growth. We are confident that the company is heading in the right direction over the next three years with stabilization of cash flow and a strong growth vehicle in Qdoba.

Jack in the Box is at the tail end of a six-year restructuring that has defined Linda Lang’s stint as CEO thus far. The stock has traded sideways for much of Lang’s tenure as management has endured a long six years of transforming the company into a more franchised business model. A more franchised business model is now set to reward JACK with less exposure to volatility in commodity prices. The question is now whether or not the investment community will revalue the earnings and cash flow stream in line with valuations of other largely franchised restaurant companies.

The fact that yesterday’s Investor Conference was the company’s first since 2008 was a positive in itself. Our expectations were for management to provide investors with a clear vision for the company’s future growth prospects now that the cash flow generation is set to pick up significantly. The 1,000 foot view that the company provided for investors included:

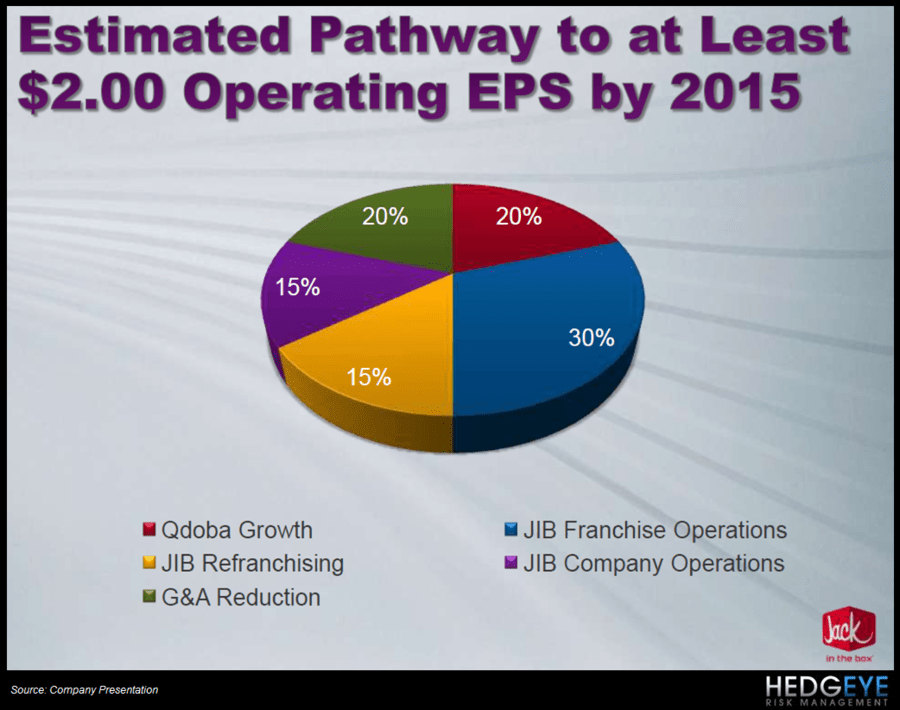

- Operating EPS of at least $2.00 by 2015, or roughly double the expected operating EPS for FY12.

- Free cash flow of ~$75 million beginning in FY15

- Shifting from maintenance to growth in capital spending focus

- 15-20% growth in Qdoba stores through FY15. Long-term target of 2,000 domestic units versus ~600 restaurants today.

This general outlook is strong, in our view, as it offers investors clarity on the source and diversity of future earnings growth and stability of cash flows. The EPS guidance is conservative, given that it assumes no stock repurchases with the free cash flow generation that the company is set to achieve over the next few years with the target being $75 million on an annual basis by FY15.

DIVERSITY OF FUTURE EARNINGS GROWTH

Doubling the company unit base of Qdoba is set to aid an increased diversification of earnings for JACK over the next three years. As management illustrated yesterday, the pathway to at least $2.00 in operating EPS by 2015 is anticipated to come from a broad range of growth vehicles. The chart, below, illustrates this 100% growth in operating EPS.

STABILITY OF THE CASH FLOWS

The company’s sources of cash flow are Jack in the Box company-owned restaurants, Jack in the Box franchise restaurants, and Qdoba. The company JIB locations have higher AUV’s and higher restaurant operating margins. The concept is not highly penetrated on a national level so we do see opportunity for expansion of the company-operated base. The JIB Franchise business was described by management as an “annuity-like” source of cash flow for the company. The company collects both royalty fees and, in 90% of cases, rental fees from franchisees. Again, given the lack of penetration of the brand on a national level, there is potential for expansion and the company bears no exposure to cost inflation. The profit flow-through on incremental sales is “near 100%”. Qdoba is a growing focus of JACK’s management team, which expects the concept to account for 25% of FY15 EBITDA versus 14% in FY11.

RETURING CASH TO SHAREHOLDERS

After a six year cash drought of cash burn, JACK is set to ring in a new era of Free Cash Flow generation. In terms of shareholder returns, this is an important point. Having negative cash flow was, in our view, a key factor in keeping investors on the sidelines over the last three years.

QDOBA GROWTH

Qdoba leverages the company to a fast-growth segment of the QSR space and, as such, will account for a larger share of capital expenditure going forward. As the table below shows, as Qdoba stores mature, they tend to perform at higher restaurant operating margins. Further, with AUV’s north of $1mm, margins approach 25%.

The strong cash-on-cash returns (21.3% versus 16.2% at JIB) generated by Qdoba are spurring management to focus its capital spending on Qdoba over the next four years. The chart below shows clearly that the company’s spending is set to shift from remodels and maintenance of Jack in the Box to growth of the Qdoba business.

CURRENT TRENDS

1QFY12 comparable restaurant sales at JIB grew 5.3%, representing the sixth consecutive quarter of positive comp growth for the concept. The increase in 1QFY12 was driven by traffic growth of 2.8% and a 2.5% increase in average check. The strength was, according to management, broad-based with each of the major markets posting increases in sales, traffic, and average check. For 2QFY12, management guided to 4-5% same-store sales at JIB versus +0.8% last year. System-wide sales are expected to increase 6% in 2QFY12 versus the same quarter a year ago.

INFLATION

Food cost inflation increased 8% for JACK in 1QFY12 and is expected to be roughly 3% for 2QFY12 and between 3% and 4% during 2HFY12.

LEVELS

The immediate-term TRADE range for JACK is $22.99 to $24.43, according to Hedgeye's quantitative models. The intermediate term TREND line is $21.02.

Howard Penney

Managing Director

Rory Green

Analyst