THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Two of the Top 3 Most Read (Bloomberg consensus) still staring at the tree (Greece) – meanwhile the rest of the world doesn’t cease to exist:

- SINGAPORE – when the Prime Minister of Singapore warned of a “rough landing” in China last wk, our research team was buzzing about it – they should have been; Singapore is a leading indicator for Global Growth – and Singapore’s Exports for JAN just dropped to negative y/y! (-2.1% vs +9.0% DEC). Chinese Growth is slowing – I sold my China Equities (CAF) long (bought it in DEC) yesterday

- OIL – never has Oil trading > $100/barrel not slowed both US and Global Consumption Growth. Maybe this time is different. Maybe it isn’t. Brent Oil busting to new highs this morning on a weak US Dollar and institutional performance chasing squarely focused on buying inflation protection.

- JAPANESE YEN – biggest currency drop not discussed by consensus media, maybe ever – and ever, as you know, is a long time. The Yen is literally straight down for the month of FEB. Down 4% is a monster move for a major currency. I think this is front-running the Sovereign Debt Maturity spike that’s pending in March. When I was saying this about the Euro breaking down hard in April 2011, that was the early signal too…

Covered SPY short at 1341, and re-shorted it into yesterday’s close. I think we keep making lower long-term highs vs 1363.

KM

SUBSECTOR PERFORMANCE

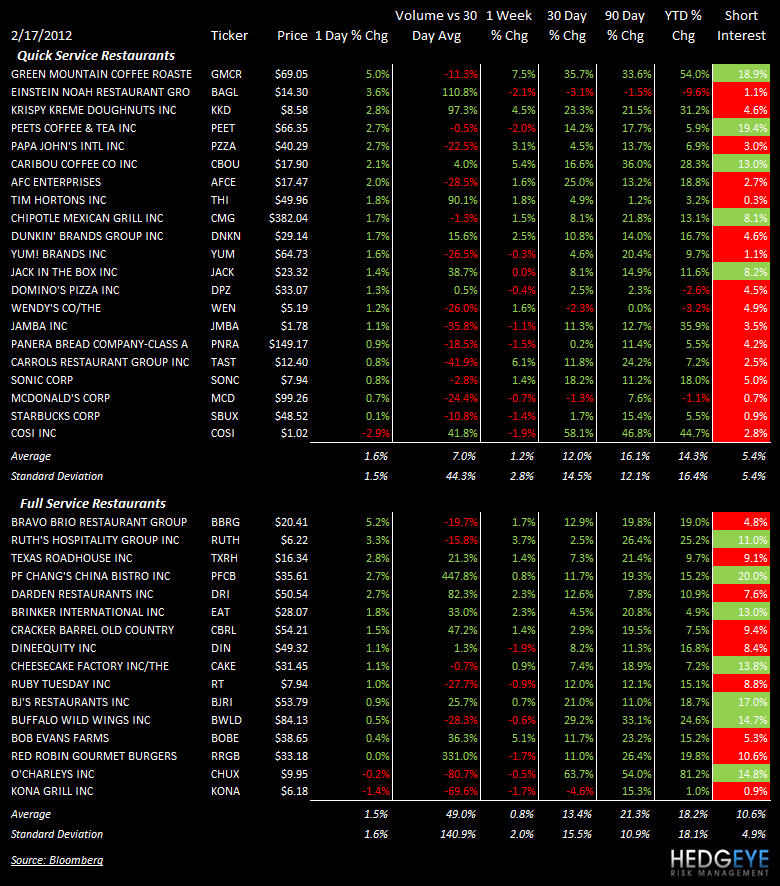

QUICK SERVICE

GMCR: Green Mountain Coffee was raised to “Buy” at Dougherty & Co. The twelve month price target is $80 per share.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

COSI: Cosi declined 2.9% on accelerating volume yesterday.

CASUAL DINING

PFCB: P.F. Chang’s was upgraded to Outperform by RBC. The price target was raised from $37 to $45.

KONA/PFCB: Kona COO Larry Ryback has resigned from the company and will leave by March 2012 to take up the post of COO of P.F. Chang’s Bistro division.

BJRI: BJ’s restaurants reported EPS of $0.34 versus consensus $0.32. Comparable sales for 4Q11 increased 5.1%.

DRI: Darden was reiterated “Buy” at UBS.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

TXRH, PFCB, DRI, EAT, CBRL, & DIN: All gained on accelerating volume yesterday. PFCB traded at 4.5x average volume following earnings. We are bullish on the stock.

Howard Penney

Managing Director

Rory Green

Analyst