Positions in Europe: No Active Positions

Asset Class Performance:

- Equities: European equity performance has been mixed over the last 5 days, with the balance towards the negative led by the periphery. This bucks the trend of strong performance from the PIIGS over the last month. Top performers: Russia (RTSI) 2.9%; Denmark 2.5%; Norway 1.2%; Sweden 1.0%; and Switzerland 80bps. Bottom performers: Greece -4.7%; Cyprus -4.7%; Spain -3.9%; Hungary -3.6%; Austria -3.3%.

- FX: The EUR/USD is down -0.4% week-to-date. Divergences: HUF/EUR +1.3%, CZK/EUR +0.8%, PLN/EUR +0.5%

- Fixed Income: 10YR sovereign yields were mixed week-to-date. Portugal led the move on the downside, falling -98bps to 11.99% followed by Germany (-14bps) to 1.83%. Greece increased the most, gaining +44bp to 33.35% followed by Italy (+26bps) to 5.78%.

In Review:

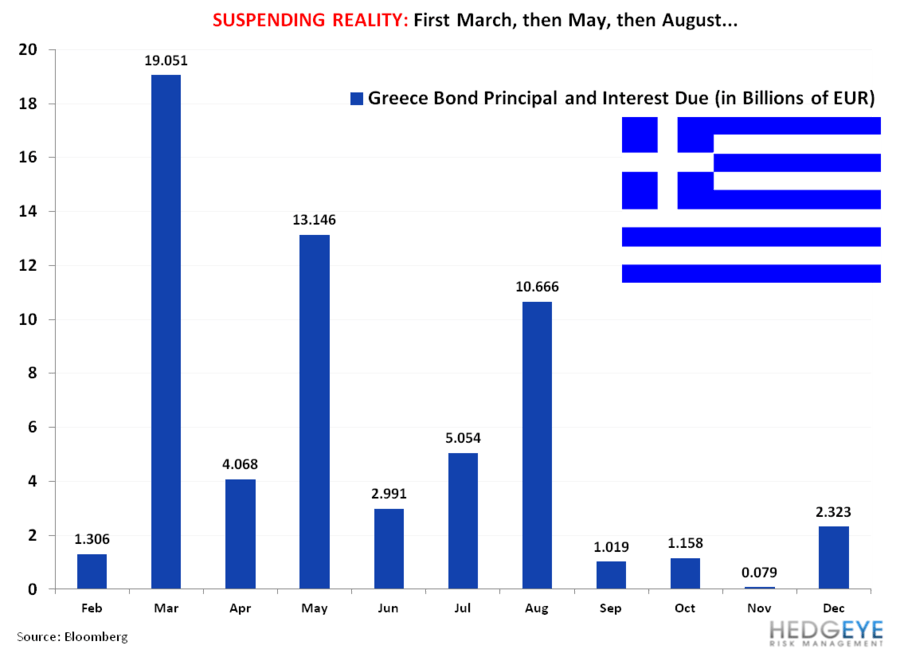

Deadlines for decision on the PSI and second Greek bailout came and went for another week as Molotov cocktails flew in the streets of Athens…. As Keith has noted in his Early Looks, Greece is but a tree in the forest, yet Greece isn’t going “away” anytime soon, which we stressed in our note “Greek PSI Is NOT Getting Done” (2/8)— we think Eurocrats will continue to suspend gravity around Greece to maintain the Eurozone project.

As we show in the extended calendar below, there are many political zig-zags ahead, including the German Bundestag’s vote on Greece’s second bailout package on February 27th. The vote could be far from a resounding “Ja”, which increases the probability that we drift towards an 11thhour decision on a Greek bailout (and PSI) ahead of the country’s €14.5 Billion bond due March 20th. Finally, this week saw elevated “rhetorical” brewing between German Finance Minister Wolfgang Schaeuble and Greek officials, yet we are not of the camp that Schaeuble speaks for Merkel.

"But it's important to say that it cannot be a bottomless pit. That's why the Greeks have to finally close that pit. And then we can put something in there. At least people are now starting to realize it won't work with a bottomless pit." -Schaeuble

Call Outs:

- Eurozone Q4 GDP (Q/Q) contracts for the first time since Q2 2009 (see chart below).

- Moody's cut its ratings on Italy, Spain (2 notches), Portugal, Slovakia, Slovenia, Malta, and placed the Aaa ratings of UK, France, and Austria on negative outlook yesterday evening.

- EU thinks Spain overstated its 2011 deficit figures to make this year’s deficit look better, and that it's also moving too slow in addressing a deterioration in public finances that is expected this year.

- Spain’s regulator announced that it is lifting its ban on short selling of financial stocks effective February 16th.

Key Regional Data This Week:

Positives (+)

Germany ZEW Current Situation 40.3 FEB (exp. 30.5) vs 28.4 JAN

Germany ZEW Economic Sentiment 5.4 FEB (exp. -11.8) vs -21.6 JAN

UK CPI 3.6% JAN Y/Y (exp. 3.6%) vs 4.2% DEC [slowed to the least in 14 months]

Negatives (-)

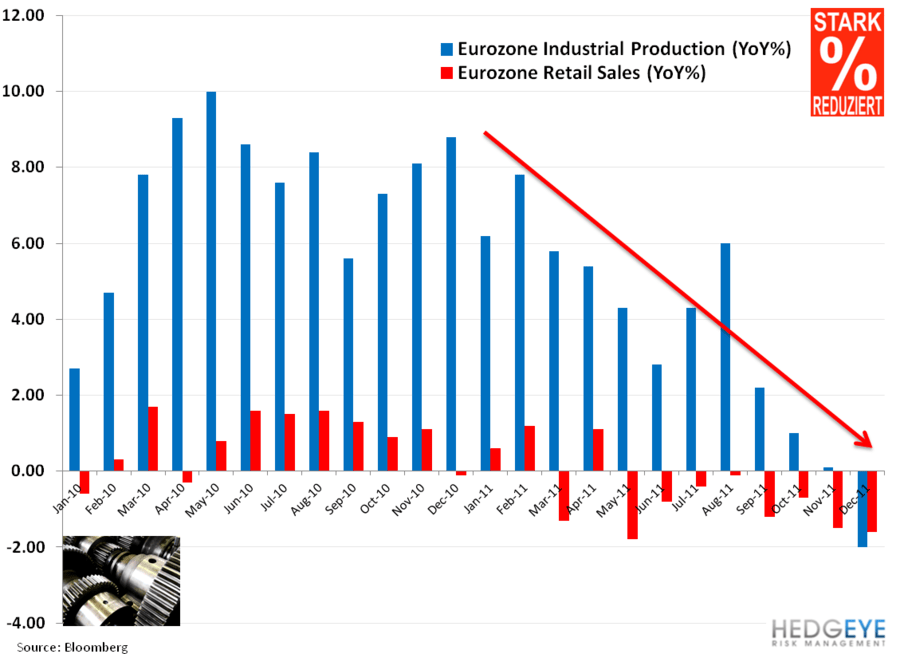

Eurozone Industrial Production -2.0% DEC Y/Y vs 0.1% NOV

Greece Q4 GDP -7.0% Y/Y vs -5.0% in Q3

EU 25 New Car Registrations -7.1% JAN Y/Y vs -6.4% DEC

Portugal Unemployment Rate 14% Q4 vs 12.4% in Q3

Rates:

(2/16) Riksbank Repo Rate CUT 25bps to 1.50% (in-line with expectations)

CDS Risk Monitor:

On a week to date basis, CDS was largely up across European sovereigns (vs up last week), with Spain leading the charge at +63bps to 416bps, followed by Italy (+56bps) to 438bps (see charts below).

Charts of the Week:

The European Week Ahead:

Monday: Eurogroup Meeting; Feb. France Production Outlook and Business Confidence Indicator; Dec. Italy Industrial Sales and Orders

Tuesday: Feb. Eurozone Consumer Confidence – Advance; Jan. UK Public Finances

Wednesday: Feb. Eurozone PMI Composite, Services, and Manufacturing – Advance; Dec. Eurozone Industrial New Orders; Feb. Germany PMI Manufacturing and Services – Advance; UK BoE Minutes; Feb. France PMI Manufacturing and Services – Preliminary; Jan. France CPI; Jan. Italy CPI – Final

Thursday: ECB Policy Meeting; Feb. Germany IFO Business Climate, Current Assessment, and Expectations; Feb. UK CBI Trends Total Orders and Selling Prices; Jan. UK BBA Loans for House Purchase; Feb. Italy Consumer Confidence

Friday: Q4 Germany GDP – Preliminary, Domestic Demand, Exports, Imports, Capital Investments, Government Spending, Construction Investment, Private Consumption; Q4 UK GDP and Total Business Investment- Preliminary, Private Consumption, Government Spending, Capital Formation, Exports, Imports, Index of Services; Feb. France Consumer Confidence Indicator; Jan. France Jobseekers; Dec. Italy Retail Sales

Extended Calendar Call-Outs:

27 February: The German Bundestag plans to vote on the issue of Greece’s second bailout, including the embedded terms of the PSI.

25-26 February: G20 Finance Ministers Meeting in Mexico City. Decision on IMF loan of €500B is expected.

29 February: 2nd 36-Month LTRO Allotment.

29 February: Eurogroup Meeting to sign the previously endorsed agreement between the 17 members on the Treaty for the European Stability Mechanism.

1-2 March: Signing of the Fiscal Compact by 17 Eurozone leaders together with the non-euro area leaders of countries willing to join. Further, the group will reassess the adequacy of resources under the EFSF and ESM rescue funds.

20 March: Greece’s €14.5 billion Bond Redemption due.

April: French Elections (Round 1) begins to conclude in May.

April: Greek Presidential Elections.

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst