Chinese New Year becoming less of a factor?

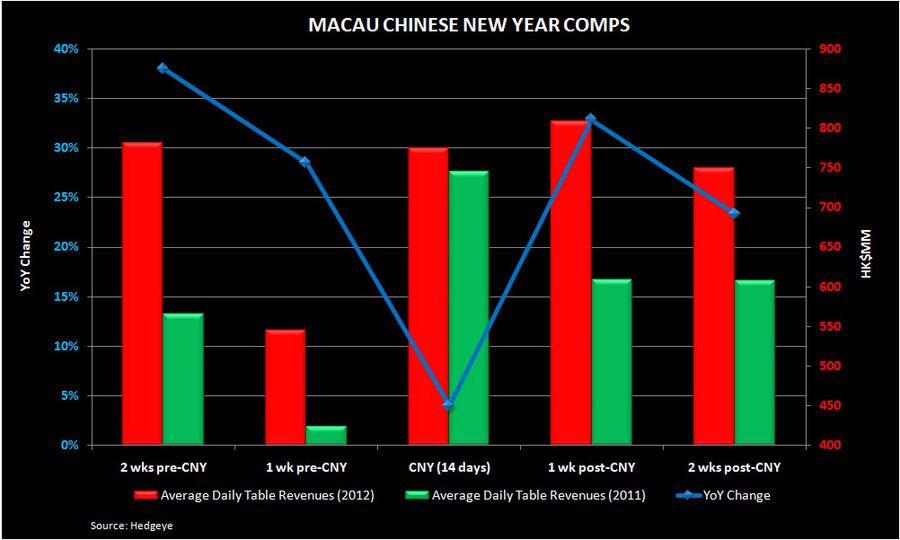

As the following chart shows, there certainly was a traditional pattern of a pre-CNY slowdown followed by a jump in Gross Gaming Revenues during the celebration. However, we still haven’t gotten the post-CNY slowdown. It is unclear, how much hold played a role in the recent strength but the historical post-CNY slowdown skipped at least this year.

Importantly for Macau, YoY growth has been surprisingly strong, with the exception of the actual CNY weeks. Growth during those two weeks was only 4% but 24-38% the other 4 weeks presented. We acknowledge that the comparisons are not perfect but the data is good enough to support our conclusions. We’d say the data leans bullish for Macau.