THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Another day of consensus staring at a Greek tree – the forest of globally interconnected risk ticks on:

- CHINA – China just moved into the Top 3 Most Read on Bloomberg this morning for the first time in a while (Greece has dominated news-flow), and given China actually matters to Global Growth, this makes sense. In the last 48 hrs Chinese data did exactly what we said it was going to do: 1. Inflation accelerating sequentially to 4.5% from 4.1% y/y and 2. Growth Slowed, big time, w/ Exports down -0.5% y/y (1st y/y drop in over 2yrs).

- FRANCE – we’re short French Equities for the 1st time since late December for 3 reasons: 1. Growth data slowing as inflation data rising 2. CAC failed at its long-term TAIL of 3565 resistance and 3. EUR/USD is bumping up against a wall of resistance at 1.33 (highly correlated to the CAC). European stocks should stop trading on Greek “news” as the economic gravity of the French slowdown becomes more glaring.

- 10-year UST – markets tend to push the Pain Trade to its highest pressure points and then put the pain on those who chased. The 10-year yield ripped yesterday all the way up to my 2.03% (intermediate-term TREND line), and then reversed (2.00% this morning and falling). If I’m right and Global Growth slows sequentially as inflation rises here in FEB, I want to be long the long-bond.

SP500 continues to make lower long-term highs (below April 2011’s 1363).

SUBSECTOR PERFORMANCE

QUICK SERVICE

COSI: Cosi initiated a consulting agreement with industry veteran Brad Blum yesterday. Blum will provide consulting services related to branding, product development, merchandising and marketing in a collaborative effort to maximize long-term shareholder value, according to a company press release.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

DNKN: Dunkin’ Brands declined on accelerating volume after reporting a strong quarter, on the surface, but failing to inspire confidence on the earnings call. We remain skeptical about the long term growth prospects of the company.

CASUAL DINING

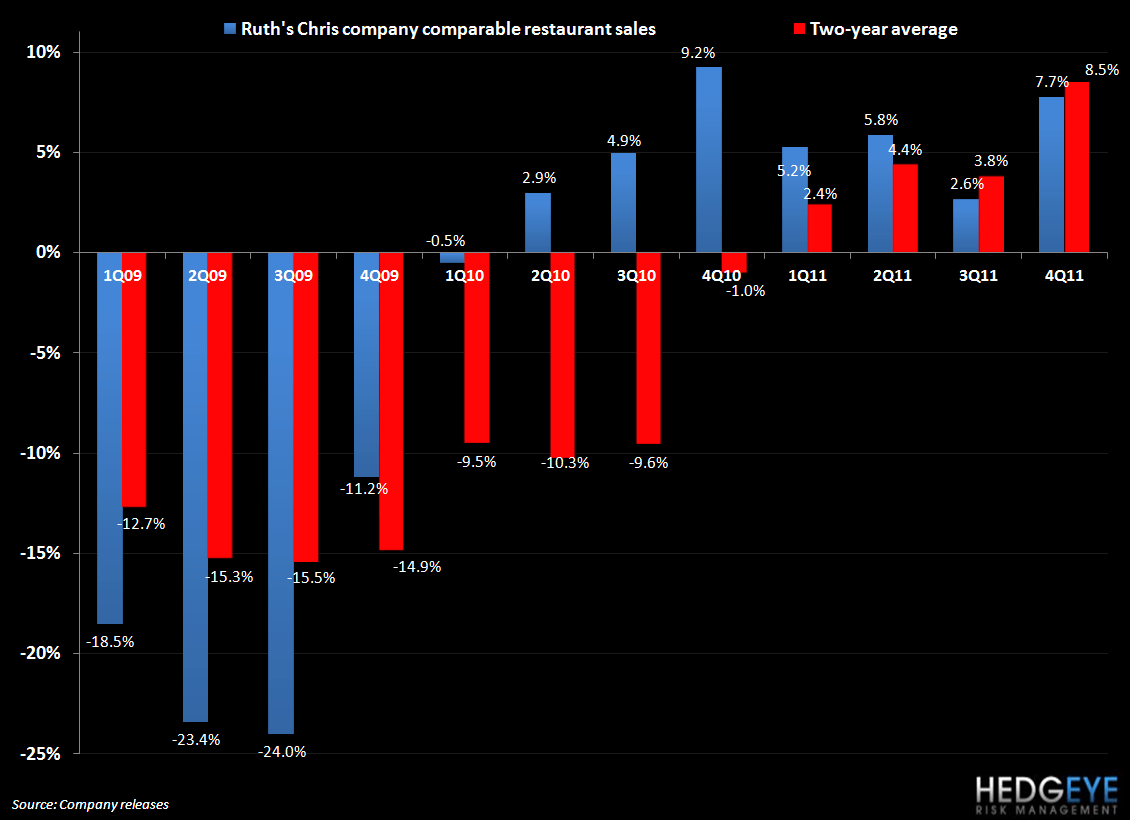

RUTH: Ruth’s Chris reported 4Q EPS of $0.11 versus consensus $0.09. Company-owned comparable restaurant sales for Ruth’s Chris increased to +7.7%.

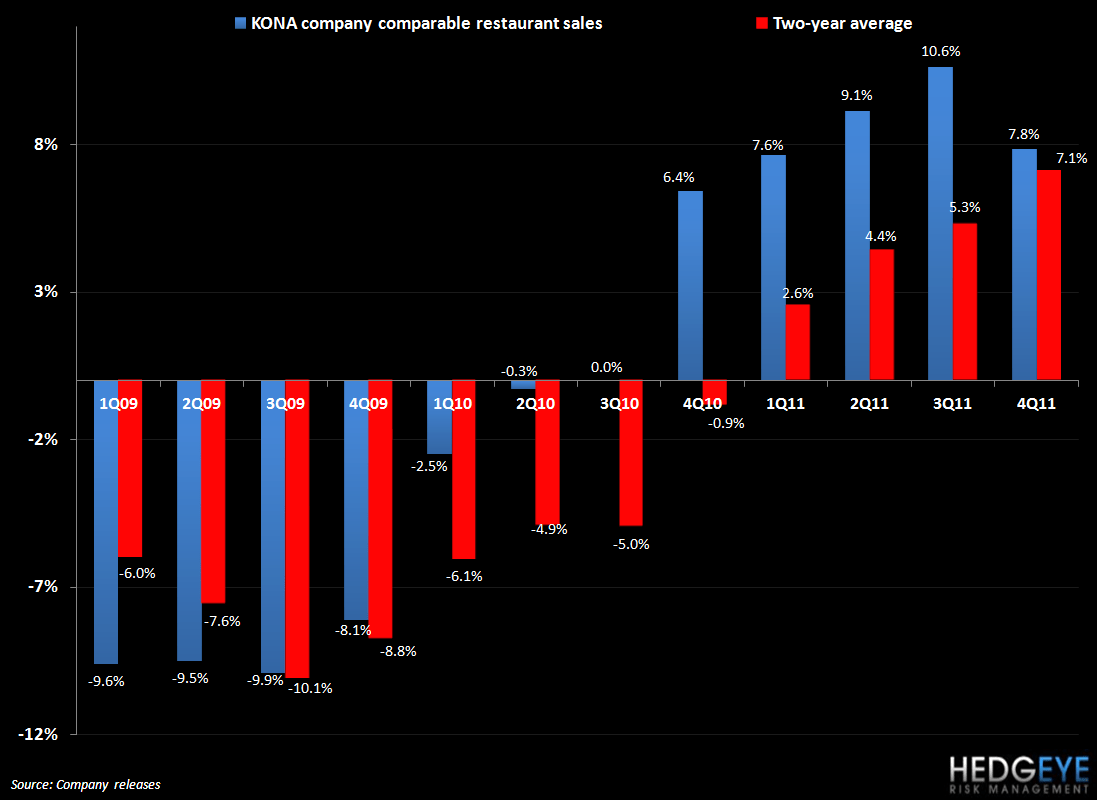

KONA: Kona Grill reported 4Q11 EPS of $0.12 (excluding severance charges of $0.04) versus $0.01 expectations. 4Q same-store sales gained 7.8%.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

BWLD: Buffalo Wild Wings continues to trade higher, gaining 3% on accelerating volume yesterday.

Howard Penney

Managing Director

Rory Green

Analyst