Claims Improvement Begets Further Claims Improvement ....

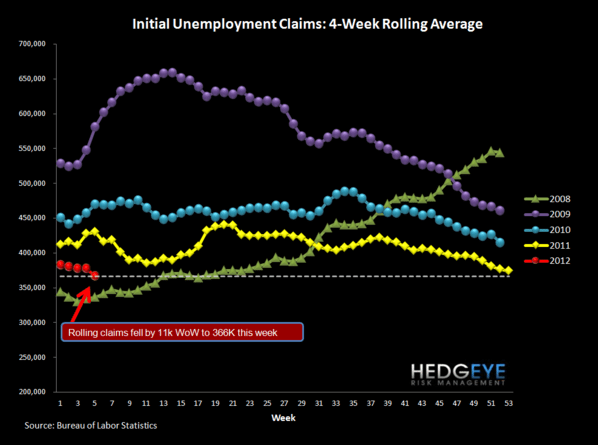

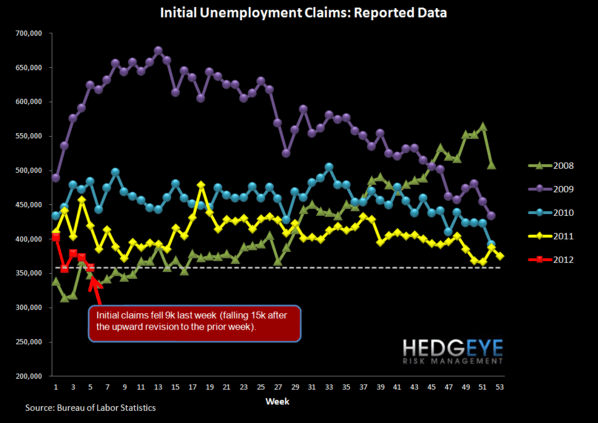

The headline initial claims number fell 9k last week to 358k (falling 15k after the upward revision to the prior week). Rolling claims fell by 11k WoW to 366k this week. On a non-seasonally-adjusted basis, reported claims fell 24k WoW to 398k.

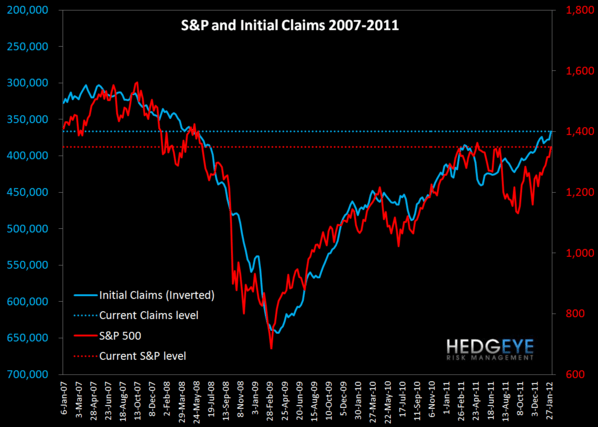

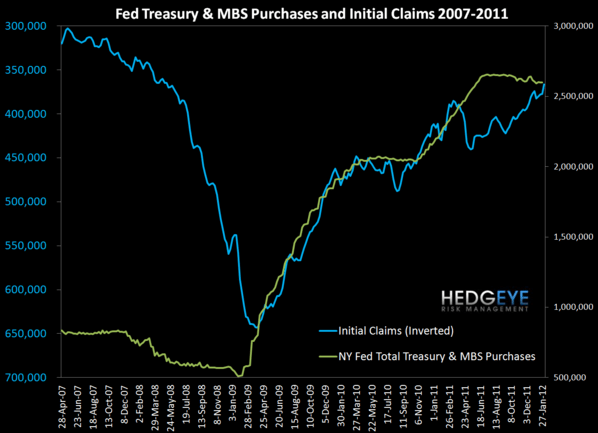

Claims remain on autopilot, for now. While some of the strength here is the byproduct of a seasonal distortion that will roll from tailwind to headwind around the end of February, the underlying trends are still very positive. Our hypothesis has been that falling claims become self-reinforcing once they break through the 375-400k level because that is the rate below which the unemployment rate can decline sustainably. This, in turn, fosters greater confidence among hiring managers and consumers, which begets further reductions in claims. The treadmill has become virtuous. This remains a key theme supporting our bullish stance on the large-cap financials. We expect this trend to continue over the intermediate term. To be clear, we're not suggesting that claims must fall week-in and week-out going forward. That would be ridiculous. Rather, we're suggesting that the general trend lower in the rolling claims series is likely to persist going forward.

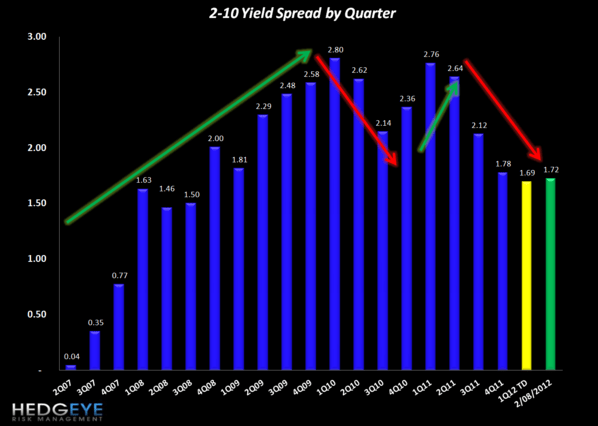

2-10 Spread

The 2-10 spread widened 12 bps versus last week to 172 bps as of yesterday. The ten-year bond yield increased 16 bps to 199 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky