THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer

Initial jobless claims came in at 358k versus expectations of 370k and 373k the week prior (revised from 367k).

SUBSECTOR PERFORMANCE

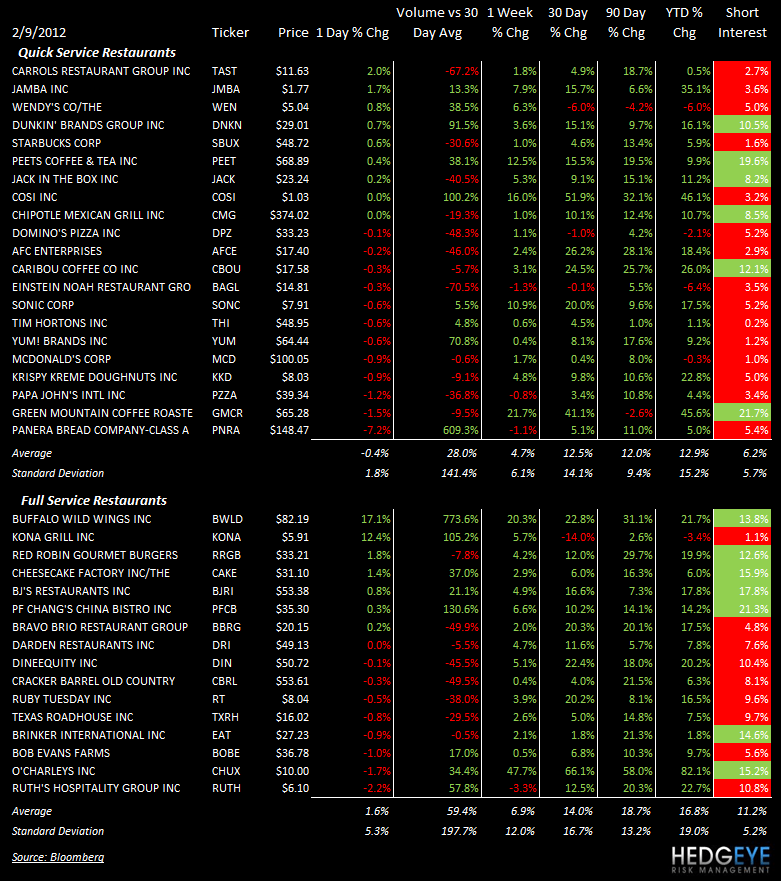

QUICK SERVICE

DNKN: Dunkin’ Brands U.S. comparable store sales were up 7.4% and Baskin-Robbins U.S. comparable sales were up 5.8% as the company reported 4Q EPS of $0.30 versus consensus $0.28.

YUM: Yum Brands was upgraded to Neutral from Sell at Goldman.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

PNRA: Panera Bread declined 7.2% on accelerating volume following disappointing earnings.

CASUAL DINING

BWLD: Buffalo Wild Wings was cut to Market Perform by Raymond James.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

BWLD: Buffalo Wild Wings led the space, gaining 17%, following much stronger than expected earnings.

Howard Penney

Managing Director

Rory Green

Analyst