TODAY’S S&P 500 SET-UP – February 7, 2012

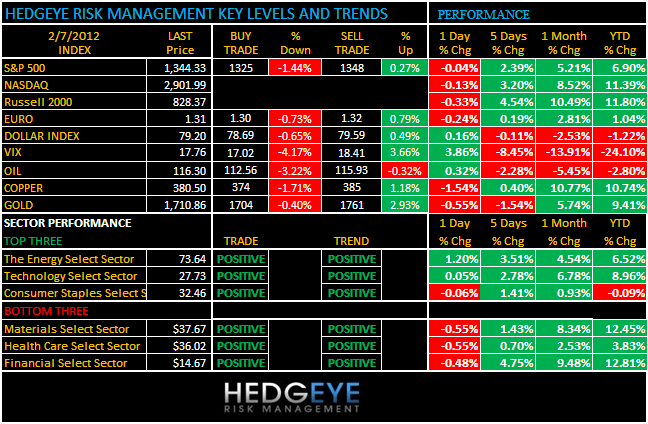

As we look at today’s set up for the S&P 500, the range is 23 points or -1.44% downside to 1325 and 0.27% upside to 1348.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -540 (-2253)

- VOLUME: NYSE 687.23 (-24.90%)

- VIX: 17.76 3.86% YTD PERFORMANCE: -24.10%

- SPX PUT/CALL RATIO: 1.78 from 1.29 (37.98%)

CREDIT/ECONOMIC MARKET LOOK:

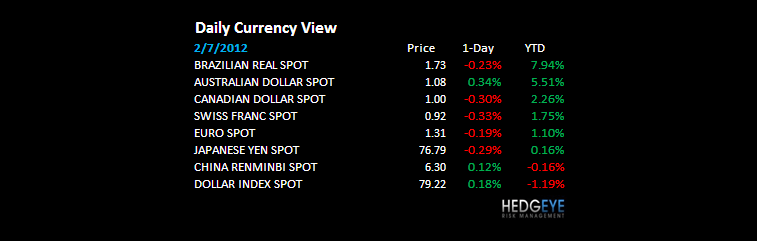

USD – attempted to have an up day yesterday, then got pounded into the close; the US Dollar Index really needs to hold its intermediate-term TREND line of 78.69 support or Gold, Oil, etc can go a lot higher.

- TED SPREAD: 45.71

- 3-MONTH T-BILL YIELD: 0.07%

- 10-Year: 1.91 from 1.91

- YIELD CURVE: 1.68 from 1.68

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: Weekly retail sales

- 10am: Fed’s Bernanke testifies to Senate Budget Committee

- 10am: JOLTs job openings

- 10am: IBD/TIPP economic optimism, est. 48.6 (prior 47.5)

- 11:30am: U.S. to sell 4-week bills, $26b 52-week bills

- 1:00pm: U.S. to sell $32b 3-yr notes

- 3:00pm: Consumer Credit, Dec., est. $7b (prior $20.374b)

GOVERNMENT

- Republican presidential caucuses in Minnesota, Colorado, non-binding primary in Missouri

- President Barack Obama speaks at White House Science Fair

- House, Senate in session:

- House Energy Committee marks up North American Energy Access Act, 9 a.m

- House Appropriations panel considers GAO, CBO budget, 9:30am

- House-Senate Conference meets on payroll tax-cut extension, 10am

- House Education and Workforce Committee holds hearing President Obama’s recess appointments to the NLRB, 10am

- Joint Economic Committee holds hearing on payroll tax- cut extension, unemployment benefits, 2:30pm

WHAT TO WATCH:

- Glencore agreed to buy Xstrata for $62b in the biggest mining takeover

- California, New York AGs still haven’t signed on to a proposed mortgage-foreclosure settlement

- Fed Chairman Bernanke testifies before Senate Budget Committee on outlook for U.S. economy, monetary policy, 10am

- Goldman Sachs said to be seeking outside investors for its REDI Technologies trading-software business

- Oracle seeks new trial in suit against SAP: court filing

- Toyota raised profit forecast for year on rebounding sales in the U.S.

- UBS 4Q profit trails est.; investment bank posts second straight loss

- SEC said to be near a proposal to shore up the $2.7t money- market fund industry, WSJ says

EARNINGS

- Becton Dickinson (BDX) 6 a.m., $1.17

- Emerson Electric (EMR) 6:45 a.m., $0.51

- Broadridge Financial Solutions (BR) 7 a.m., $0.13

- Church & Dwight (CHD) 7 a.m., $0.51

- Scotts Miracle-Gro (SMG) 7 a.m., $(1.21)

- TransDigm Group (TDG) 7 a.m., $1.25

- AGCO (AGCO) 7:30 a.m., $1.33

- Harman International Industries (HAR) 7:30 a.m., $0.74

- Coca-Cola (KO) 7:30 a.m., $0.77

- Perrigo Co (PRGO) 7:47 a.m., $1.15

- Louisiana-Pacific (LPX) 8 a.m., $(0.20)

- Magellan Midstream Partners (MMP) 8 a.m., $0.95

- Martin Marietta Materials (MLM) 8:12 a.m., $0.39

- Bell Aliant (BA CN) 8:19 a.m., C$0.38

- Saputo (SAP CN) 9:37 a.m., C$0.63

- Netgear (NTGR) 4 p.m., $0.64

- Panera Bread (PNRA) 4 p.m., $1.42

- Axis Capital Holdings (AXS) 4:01 p.m., $0.44

- Cerner (CERN) 4:01 p.m., $0.53

- Life Technologies (LIFE) 4:01 p.m., $1.04

- Western Union (WU) 4:01 p.m., $0.40

- Buffalo Wild Wings (BWLD) 4:01 p.m., $0.67

- Waste Connections (WCN) 4:04 p.m., $0.35

- CBRE Group (CBG) 4:05 p.m., $0.43

- ValueClick (VCLK) 4:05 p.m., $0.40

- Solera Holdings (SLH) 4:05 p.m., $0.68

- Lincoln National (LNC) 4:10 p.m., $1.00

- Two Harbors Investment (TWO) 4:10 p.m., $0.42

- Walt Disney (DIS) 4:15 p.m., $0.72

- Hartford Financial (HIG) 4:15 p.m., $0.60

- RenaissanceRe Holdings (RNR) 4:30 p.m., $1.04

- CYS Investments (CYS) 5:01 p.m., $0.51

- RAL Holdings (RAH) 5:04 p.m., $1.37

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

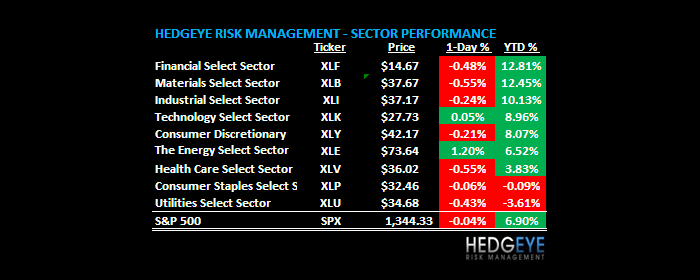

OIL – so the price of Brent Oil is at $115.95 this morning = up +6% since the #SOTU and #BernankTax on the week of Jan 23rd; since we know that inflation slows real-consumption growth, we think being long energy (XLE) and anything inflation really (as opposed to being long Consumer Discretionary (XLY) like we were before Jan 26th) is the right sector shift.

- Farmers Plan Biggest Crops Since 1984, Led by Corn: Commodities

- Corn Falls as U.S. May Plant Most Since 1944; Wheat Declines

- Glencore’s 2011 Trading Earnings Slide on Cotton Plunge, Metals

- Copper Falls for Second Day as Chinese Output Growth May Slow

- Sugar Falls as Brazil’s Production May Increase; Cocoa Drops

- Oil Trades Near Six-Week Low on Forecast of Rising U.S. Supplies

- Gold May Decline as Dollar Strengthens Amid Greece Bailout Talks

- Sugar May Fall 20% This Year Before Second Consecutive Surplus

- Russia May Not Need to Limit Grain Exports, Producers Union Says

- Billion-Ton Coal Market Looms as India Increases Sea Cargoes

- Glencore, Xstrata Deal to Squeeze Japan Coal After Fukushima

- Carbon Capture Projects Imperiled by Worst-Case Scenario: Energy

- Tanker Rates Seen at Four-Year High as Refineries Shut: Freight

- Copper Stockpile Drop May Herald China Revival: Chart of the Day

- Glencore Agrees to Buy Xstrata for $41 Billion in Shares

- Distressed Ship Owners to Rise as Rates Plunge, Fitch Says

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

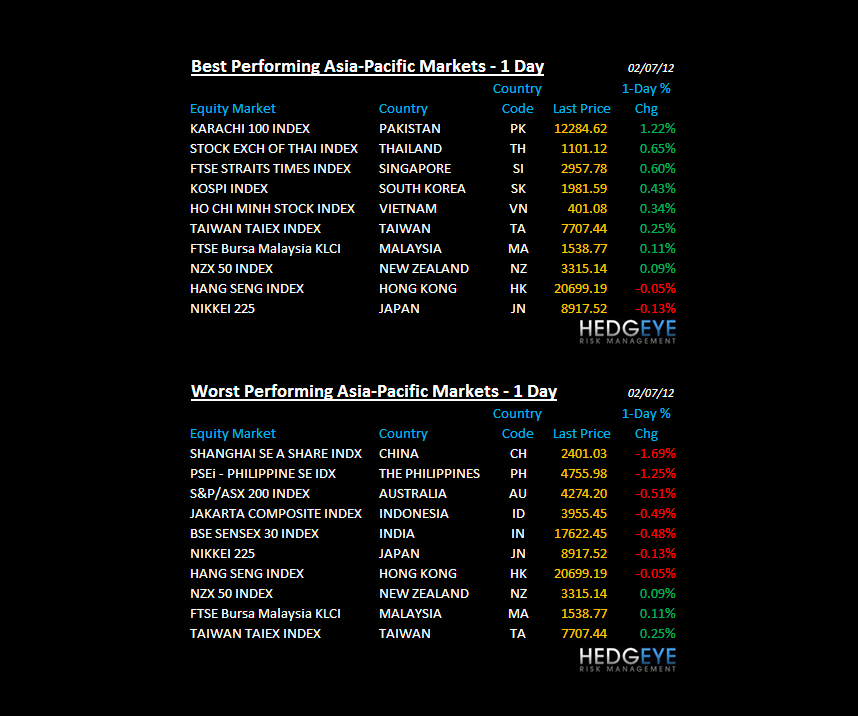

ASIA – follow the bouncing macro ball – China fails at TREND line resistance yesterday (down 1.7% overnight); Singapore’s PM warns of a Chinese “rough landing” ahead of this week’s China data; and Glenn Stevens at the RBA refused to cut Aussie interest rates last night = inflation expectations in Asia rising like the chart of Brent Oil.

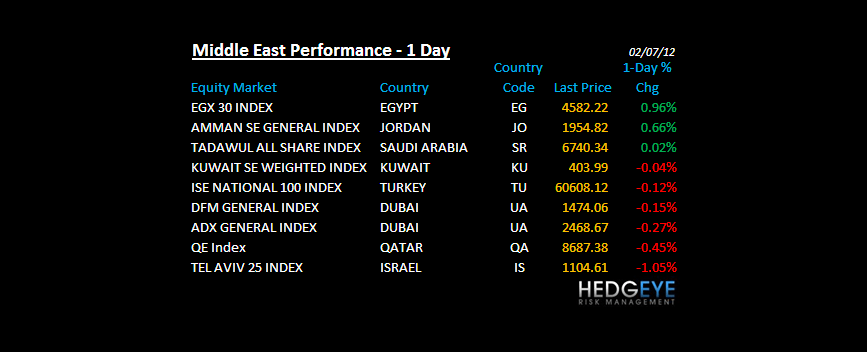

MIDDLE EAST

The Hedgeye Macro Team